ENA Token Analysis

Introduction

The recent surge in the supply of the USDe token has prompted a closer look at the activity surrounding the Ethena protocol and how its token ENA compares to its peers. This article examines the Ethena protocol's performance, its underlying activities, and how its token's value relates to the broader ecosystem of similar protocols. By comparing ENA to its competitors, we aim to shed light on the factors driving its valuation and explore the dynamics between protocol activity and token valuation across the sector.

Project Overview

Ethena is a synthetic dollar protocol built on Ethereum that provides a crypto-native solution for money, not reliant on traditional banking infrastructure. Its synthetic dollar, USDe, maintains a stable value by using a strategy called delta-hedging with Ethereum (ETH) and Bitcoin (BTC) as collateral. In simpler terms, USDe holds its value because Ethena holds ETH and BTC and shorts their futures in equal amounts. This means that if the prices of ETH or BTC go up or down, the total value of the collateral remains stable in USD terms.

Besides functioning as a stablecoin, USDe can be staked to become sUSDe, a yield-bearing stablecoin. sUSDe generates yield from two sources: staking rewards from ETH (since all ETH used as collateral is staked) and the positive carry from shorting ETH/BTC futures. Currently, this token is yielding an annual percentage yield (APY) of 13.7%.

Ethena faces several risks, including funding rate fluctuations, potential liquidation scenarios, custodial dependencies, exchange failures, and collateral valuation differences. These risks are actively managed through various strategies designed to ensure the stability and reliability of USDe. For a detailed explanation of how these risks are addressed, please refer to: Ethena Risks

Project Metrics

Currently, $3.44 billion Ethena USDe has been minted, with about half of it staked as sUSDe. The growth of these tokens has been astonishing, rising from $139 million in supply at the start of February.

Holder Distribution

USDe: 14,588 wallets hold USDe on Ethereum. The top three wallets hold over 50% of the unstaked supply.

sUSDe: 7,282 wallets hold sUSDe, with about 50% of the tokens held in Pendle.

Token Use

Overall, on-chain activity for USDe and sUSDe is very active, with a large focus on DeFi. One of the largest protocols that use USDe/sUSDe tokens is Pendle, a platform that allows the trading of yield. Currently, there is $1.46 billion of Ethena’s tokens in Pendle, which makes up a little less than half of all the stablecoins.

ENA Token Metrics

Use of ENA Token

The ENA token’s roles within the Ethena ecosystem are primarily focused on governance and utility. Holders of the ENA token can participate in the decentralized governance of the Ethena protocol, influencing decisions about the platform's development and future direction. This includes voting on various proposals that affect the protocol's updates and strategic moves.

Token Price/Market Cap

The ENA token launched in April at around $0.65 and experienced a significant uptrend in the first two weeks it was live, followed by a downtrend that continues today. Currently, the price of ENA is $0.41, resulting in a market cap of $700 million and a fully diluted market cap of $6.1 billion, with only 11.4% of the tokens circulating.

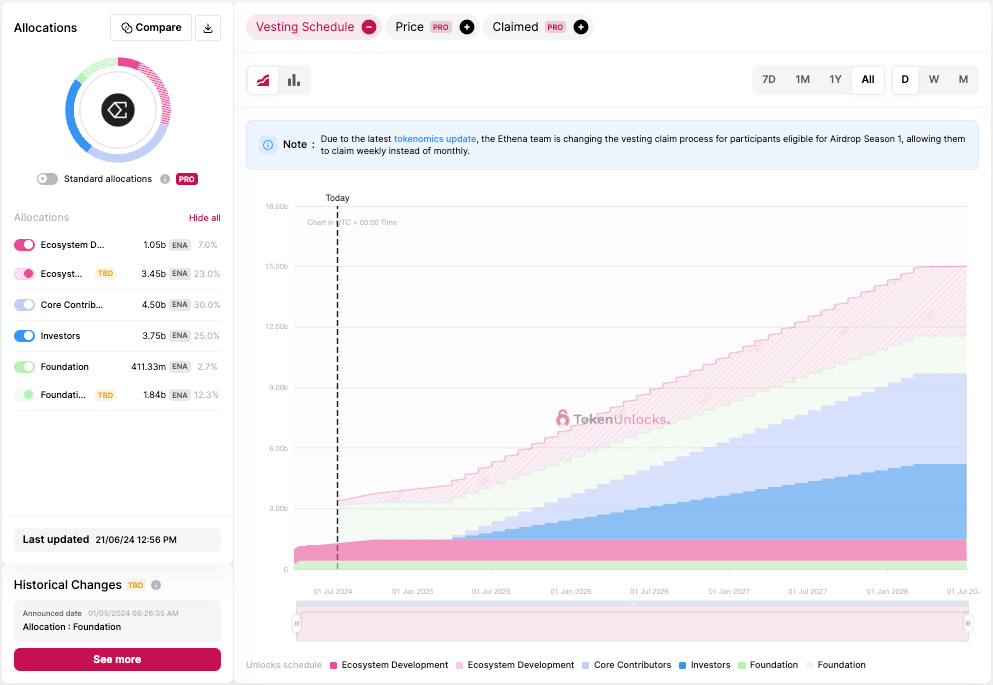

Token Unlock Schedule

Each week until the end of September, 14 million ENA tokens (approximately $6.13 million) will be unlocked for ecosystem development. There are about 5 billion tokens with discretionary release timing, comprising 1.8 billion for the foundation and 3.4 billion for the ecosystem. Investor and contributor allocations will start unlocking in April 2025 at a rate of 229 million tokens per month.

Market Cap Assessment and Comparisons

ENA is a stablecoin project currently valued at $6.1 billion with a TVL of $3.4 billion, generating 0.78% of its TVL in annual revenue. Comparatively, MakerDAO, a similar stablecoin business, has $5.3 billion in TVL and a market cap of $2.3 billion, while Frax has a market cap of $649 million for its stablecoin and $241 million for its governance token. Currently, ENA is generating annual revenue of $26.52 million (0.78% of $3.4 billion). With a P/E ratio of 234, the implied revenue to justify the current market cap is $244 million. This would require the TVL to grow to $31.28 billion to align with the current P/E ratio using the same revenue percentage. This suggests that the market is pricing in a substantial future growth expectation.

Given a more conservative and sustainable growth trajectory, transitioning from a hyper-growth phase to a stable phase, ENA would need to increase significantly over the next 3-5 years. To transition from a hyper-growth phase with a P/E ratio of 234 to a more sustainable P/E ratio of 25, ENA should follow these TVL growth milestones:

Year 1: TVL grows to $6.8 billion, with a P/E ratio of 115.

Year 2: TVL grows to $11.9 billion, with a P/E ratio of 66.

Year 3: TVL grows to $17.85 billion, with a P/E ratio of 44.

Year 4: TVL grows to $22.31 billion, with a P/E ratio of 35.

Year 5: TVL grows to $27.89 billion, with a P/E ratio of 28.

These milestones indicate the substantial but gradually slowing growth required for ENA to justify its current valuation. This path reflects a realistic transition from hyper-growth to more sustainable growth, aligning the P/E ratio with industry norms over time. Increasing the revenue-to-TVL ratio would also allow these TVL milestones to be less aggressive, easing the growth targets needed to justify the current valuation.

Given the aggressive growth expectations priced into ENA's current valuation, investors should closely monitor the stablecoin TVL milestones mentioned above. Achieving these targets is crucial for ENA to justify its high valuation and maintain investor confidence. While ENA appears overvalued compared to its peers based on current metrics, its rapid growth potential, if successfully realized, could validate the market's optimism.

Conclusion

Ethena showcases both impressive growth and aggressive valuation. While the current market cap of $6.1 billion appears high compared to similar protocols like MakerDAO and Frax, Ethena's unique approach and rapid growth offer substantial potential. To realize this potential, Ethena must focus on expanding its stablecoin supply and increasing its revenue-to-TVL ratio.

The aggressive growth expectations priced into ENA's current valuation suggest that the market is anticipating substantial future growth. Investors should closely monitor the stablecoin TVL milestones previously mentioned, as achieving these targets is crucial for ENA to justify its high valuation and maintain investor confidence. Alternatively, increasing the revenue-to-TVL ratio would allow these TVL milestones to be less aggressive, easing the growth targets needed to justify the valuation.

However, due to the delta hedging strategy that backs USDe, there may be a natural limit to the amount of stablecoins that can be profitably issued. This limit could be heavily influenced by market conditions, as the effectiveness and profitability of delta hedging are contingent upon the funding rates of Ethereum (ETH) and Bitcoin (BTC).

While ENA appears overvalued compared to its peers based on current metrics, its rapid growth potential, if successfully realized, could validate the market's optimism. By increasing its stablecoin supply, improving its revenue-to-TVL ratio, and maintaining robust growth, Ethena can solidify its position as a leader in the synthetic dollar and stablecoin space. Nonetheless, the reliance on delta hedging introduces a layer of complexity that investors should consider, as market conditions will play a significant role in determining the sustainable growth of the stablecoin supply.

Sources

https://token.unlocks.app/ethena

https://coinmetro.com/price/ena

https://defillama.com/

https://coinmarketcap.com/