$JUP Token Overview

Jupiter has established itself as one of the most recognizable projects on the Solana blockchain, rapidly expanding its product suite to capture significant market share across multiple verticals far beyond its origins as a DEX aggregator. Yet despite massive growth in usage and reach, the JUP token has been in a consistent grind downward over the past year, dropping 84% from this time last year. In this article we dive into Jupiter’s different product lines, their growth trajectories, how the team treats the token, and at what price JUP becomes a buy.

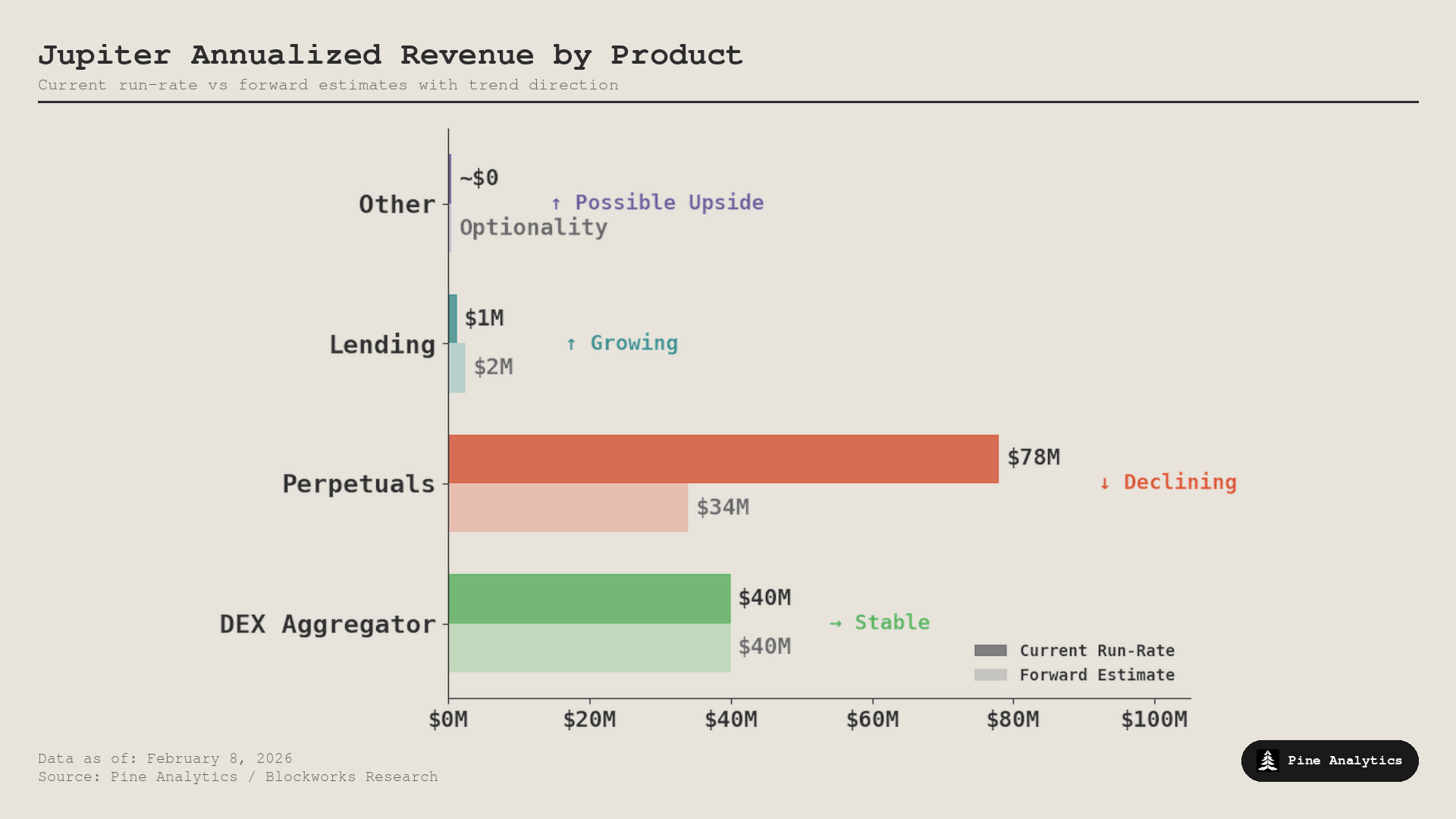

DEX Aggregator

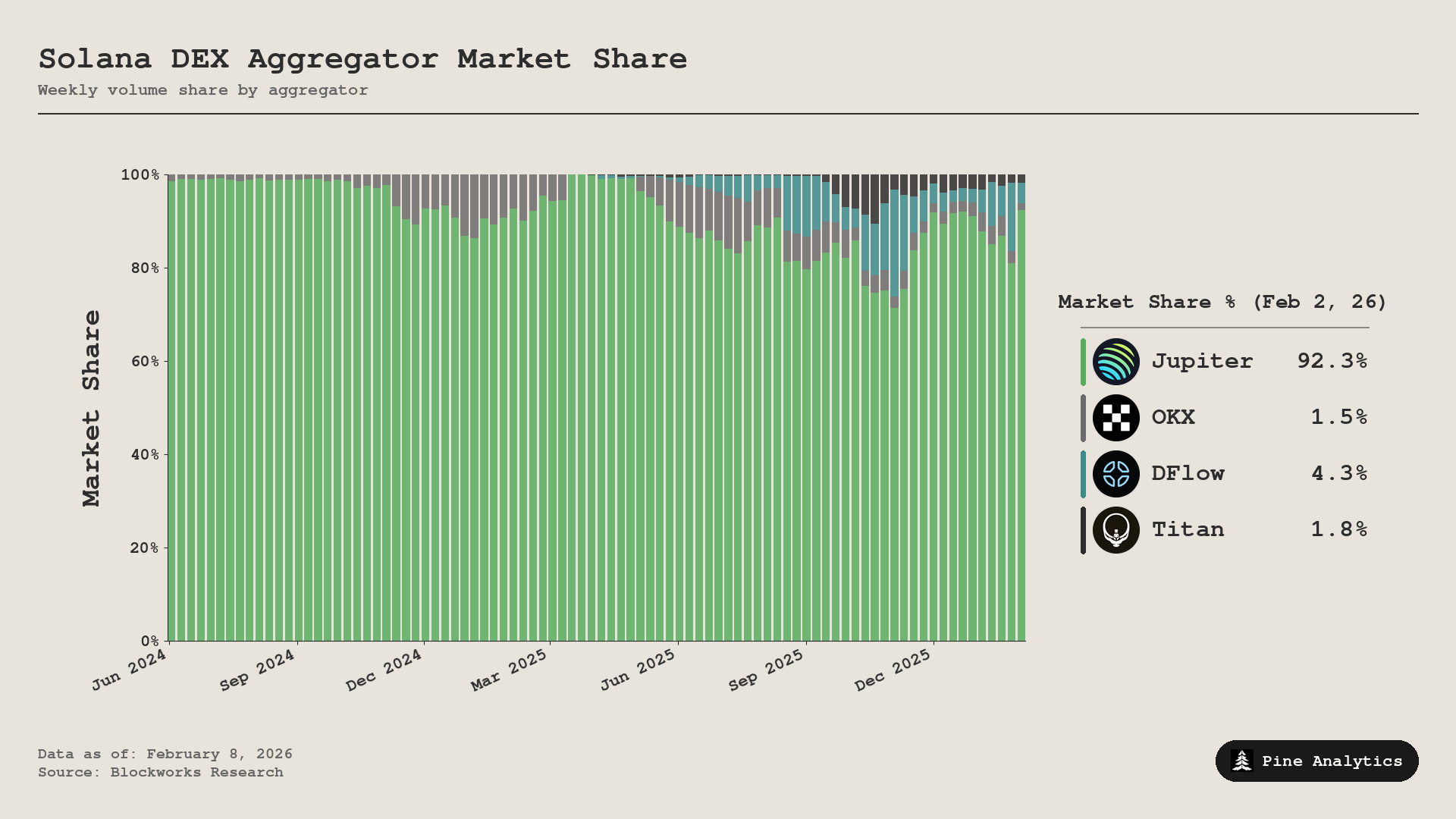

The first thing to examine is Jupiter’s market share and revenue as a DEX aggregator on Solana. Until the end of 2024, Jupiter was effectively the only relevant DEX aggregator on the chain. That changed when OKX started gaining traction, and by November 2025 Jupiter’s share of aggregator volume on Solana had fallen to 71%, with DFlow and Titan rounding out third and fourth. But that proved to be the trough. Since then Jupiter has climbed back to 92% market share, trending toward complete dominance. Currently the Jupiter aggregator generates between $500K and $1.2M per week in revenue, which annualizes to roughly $40M at current rates. This revenue stream is Jupiter’s most defensible and dominant.

Perpetuals

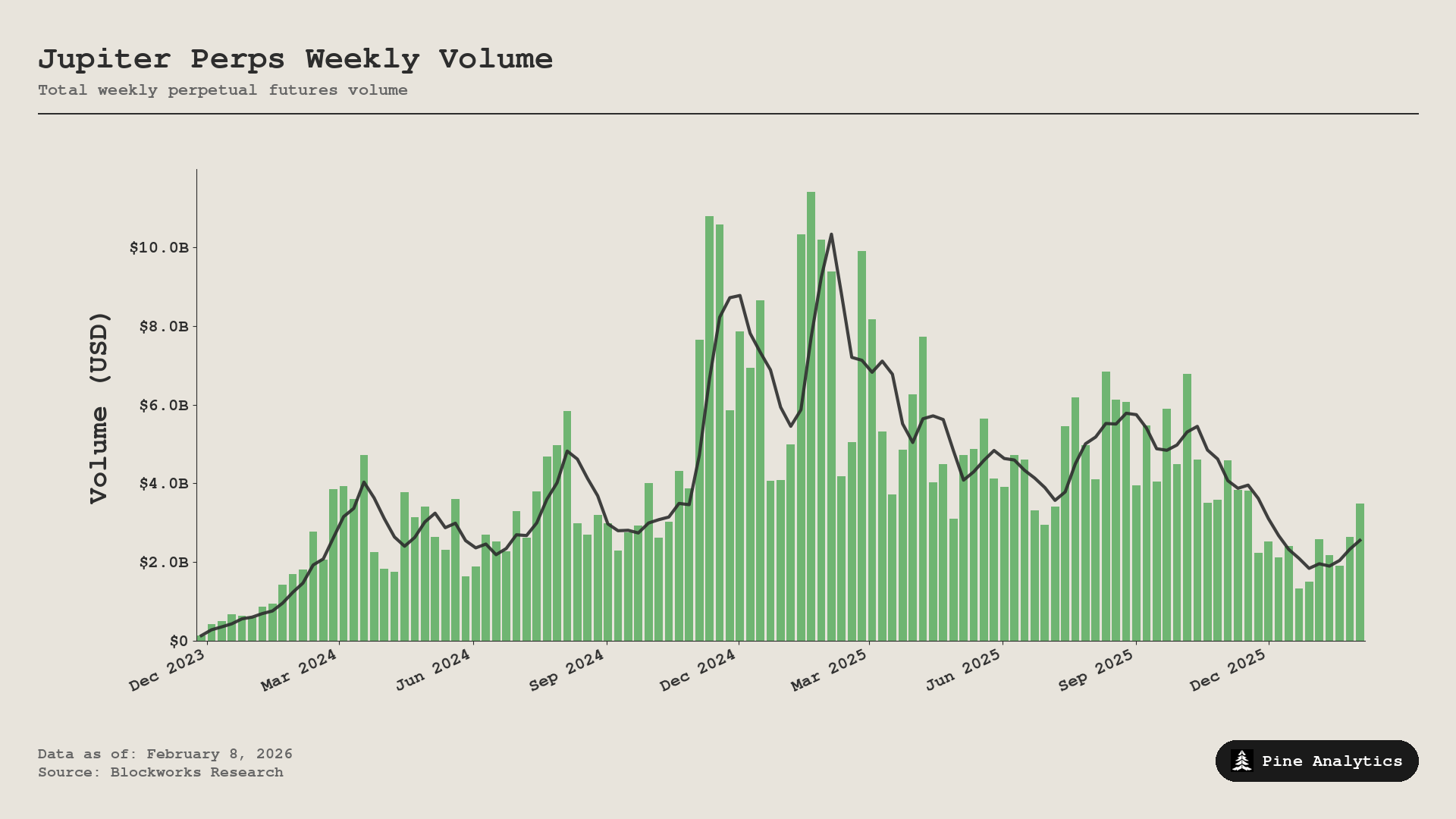

Jupiter’s second most important and highest revenue-generating product line is Jupiter Perps. Currently Jupiter Perps allows users to go long or short on SOL, ETH, and BTC, making it the second-highest volume perps DEX on Solana. However, its volume has been on a downtrend since the start of 2024. When comparing Solana perps to the broader perpetuals DEX market, they represent only a small portion of overall volume and are shrinking in market share. This product is on a downtrend with no clear catalyst for a reversal. Over the past month, average revenue generated by Jupiter Perps has been about $1.5M per week, which would annualize to roughly $78M. But factoring in the ongoing decline in activity, a more realistic annualized figure is probably half that rate, around $34M in fees.

Lending

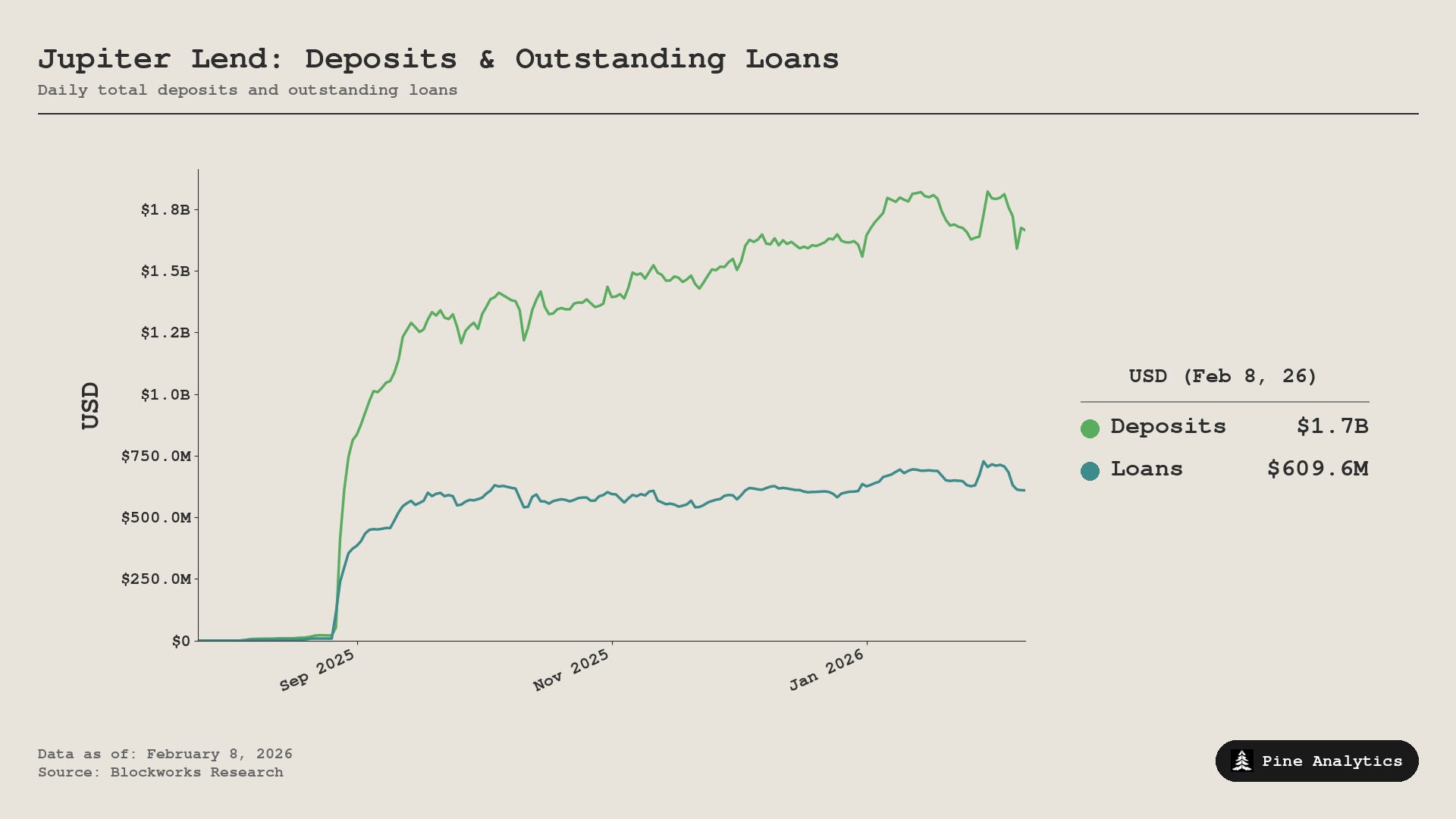

The third most important protocol in Jupiter’s product suite is Jup Lend. Currently the lending market holds $1.6B in deposits, mostly composed of USDC, SOL, and JLP. Compared to Kamino, the top lending protocol on Solana with about $3B in deposits, Jup Lend is smaller but its deposits are slowly grinding higher while Kamino’s have been declining since mid-December. Currently Jup Lend produces about $20K to $30K per week very consistently, annualizing to roughly $1M to $1.5M per year.

Other Products

In addition to these three major product lines, Jupiter has launched a stablecoin with a market cap of $34M, deployed a prediction market aggregator doing about $400K in weekly volume, launched a wallet, and shipped various other long-tail products.

Token Alignment

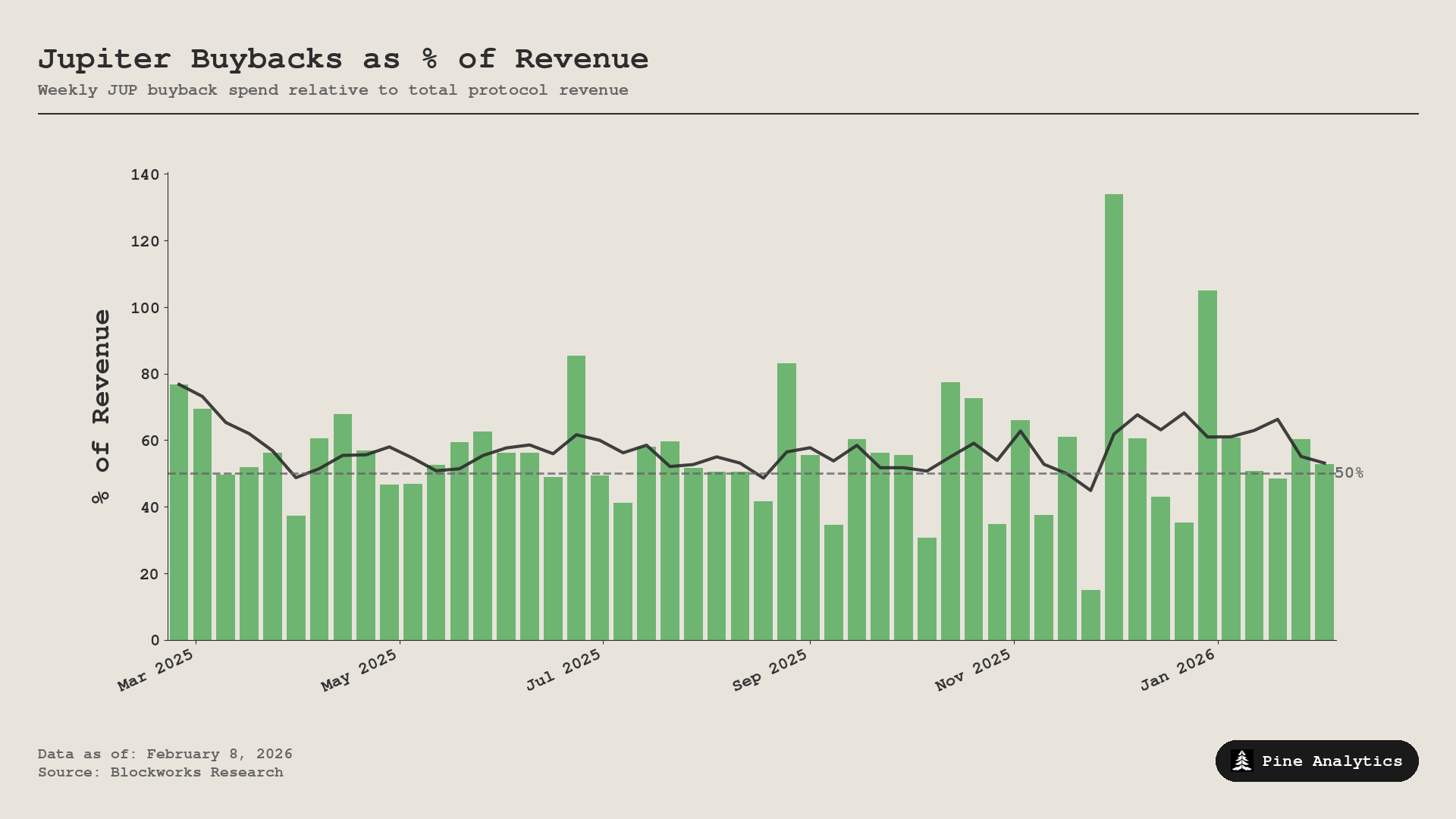

When evaluating Jupiter’s alignment toward the token, we look at the historical percentage of revenue directed toward buybacks. Since May 2025, just over 50% to 60% of revenue has consistently been used for JUP token buybacks, demonstrating strong and sustained alignment between the protocol’s revenue and token value.

Valuation

Pulling the revenue estimates together, Jupiter’s annualized revenue across its core products comes to roughly $75M to $80M: $40M from the aggregator, $34M from perps on a declining trajectory, and $1M to $1.5M from lending. The long-tail products (stablecoin, prediction markets, wallet) contribute marginal revenue today but represent optionality.

At the current JUP price of $0.15 and an FDV of $1B, Jupiter trades at a fully diluted price-to-revenue multiple of roughly 13x on current earnings. For a protocol with a dominant aggregator position and proven buyback commitment, that is a reasonable multiple, but not yet a compelling entry point.

The aggregator alone generates ~$40M per year and is trending toward complete dominance at 92% market share. This is Jupiter’s floor value. The perps line adds $34M in annualized revenue but is in structural decline, so discounting that by half to ~$17M is prudent for forward modeling. Lending and the long-tail products round out the picture with another $2M to $3M today, with optionality for more.

Using a conservative base case of $60M in forward annualized revenue (aggregator holds, perps decline further, lending grows modestly) and applying a 10x multiple gives a floor FDV of $600M, which implies a JUP price of roughly $0.09. At that level you are paying a single-digit multiple on proven revenue streams and getting all of Jupiter’s product expansion for free. That is where JUP becomes a compelling buy with meaningful margin of safety.