$P2P: MetaDAO ICO Analysis

Executive Summary

P2P.me is a non-custodial USDC-to-fiat on/off ramp built on Base, using zk-KYC and on-chain settlement to let users buy, sell, and spend USDC through local payment rails like UPI, PIX, and QRIS. The protocol is live in India, Brazil, Argentina, and Indonesia with 23,000+ registered users and peaked at $1.97M in monthly volume in February 2026. It’s backed by Multicoin Capital, Coinbase Ventures, and Alliance DAO ($2.33M total raised), and is now launching a $P2P token via MetaDAO’s ICO framework targeting a $6M raise at ~$15.5M FDV.

The product is real, the traction is on-chain verifiable, and the privacy-first design addresses genuine pain points — particularly the bank-freeze problem in India, where 78% of users are concentrated. However, at a $15.5M FDV the valuation looks stretched relative to fundamentals. Annual gross profit — what the protocol actually captures after merchant commissions — is running at roughly $82K, implying a ~182x multiple. Active user growth has plateaued since mid-2025, and the planned expansion to 20+ countries risks diluting focus before the protocol has saturated the markets it’s already in. Strong product, real usage, but the price requires growth assumptions the data doesn’t yet support.

App Overview

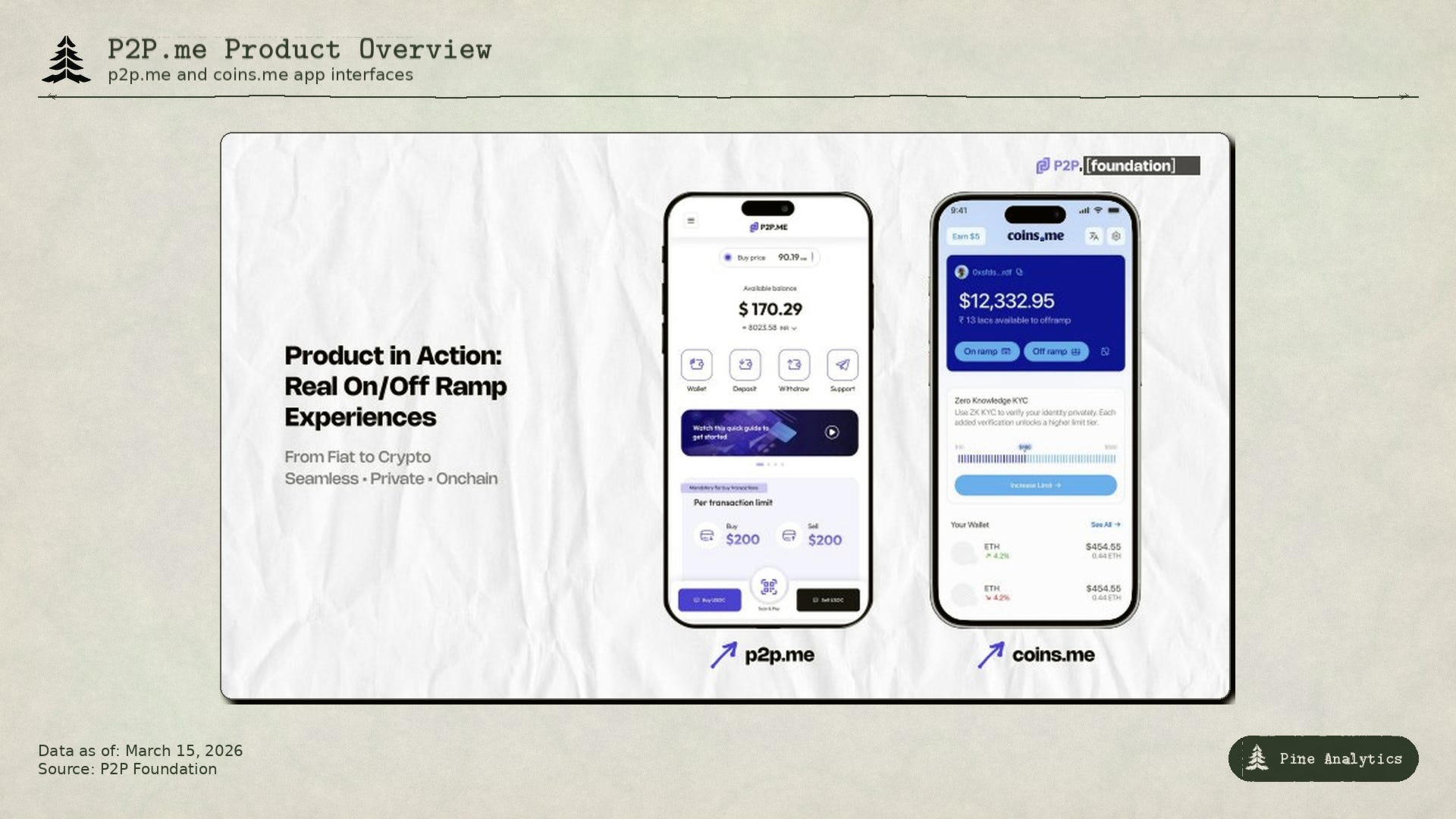

P2P.me is a decentralized, non-custodial USDC-to-fiat on/off ramp built on Base (Coinbase's L2). The core idea is simple: you can spend USDC at any store that accepts local payment methods (UPI in India, PIX in Brazil, QRIS in Indonesia, ARS in Argentina) by swapping crypto to fiat in near real-time through a peer-to-peer network of liquidity providers.

How it works:

The protocol connects two sides. On one side, you have users who want to buy or sell USDC. On the other, you have “Liquidity Providers” (merchants) who hold USDC and process swaps through their own bank accounts. When a user wants to off-ramp, they send USDC into the protocol, a merchant receives the order, and the merchant sends fiat to the user’s local payment method. The reverse works for on-ramping. Merchants earn 2% on every swap they facilitate.

Key design choices:

The privacy angle is the most interesting part. They use “zk-KYC” (zero-knowledge identity verification) — so users can verify their identity to unlock higher limits without actually sharing personal data with the platform or counterparties. No traditional KYC is required to start using it, just ZK verification to prevent fraud. They claim a fraud rate of less than 1 in 25,000 transactions, which they say is 100x better than competing P2P services.

On the bank freeze issue (which is a massive pain point in India’s crypto P2P scene), they offer a 100% refund guarantee in USDC if a transaction on P2P.me (after September 1, 2025) leads to a bank freeze or lien, plus a community legal team to help resolve it. They also recommend users maintain a separate bank account specifically for P2P off-ramps.

Business details:

Total funding across all rounds is $2.33M from four investors: Reclaim Protocol ($80K angel, March 2023), Alliance DAO ($350K, March 2024), Multicoin Capital ($1.4M at $15M FDV, January 2025), and Coinbase Ventures ($500K at $19.5M FDV, February 2025). They have 1,000+ liquidity providers globally and currently serve India, Brazil, Indonesia, and Argentina, with Venezuela in alpha.

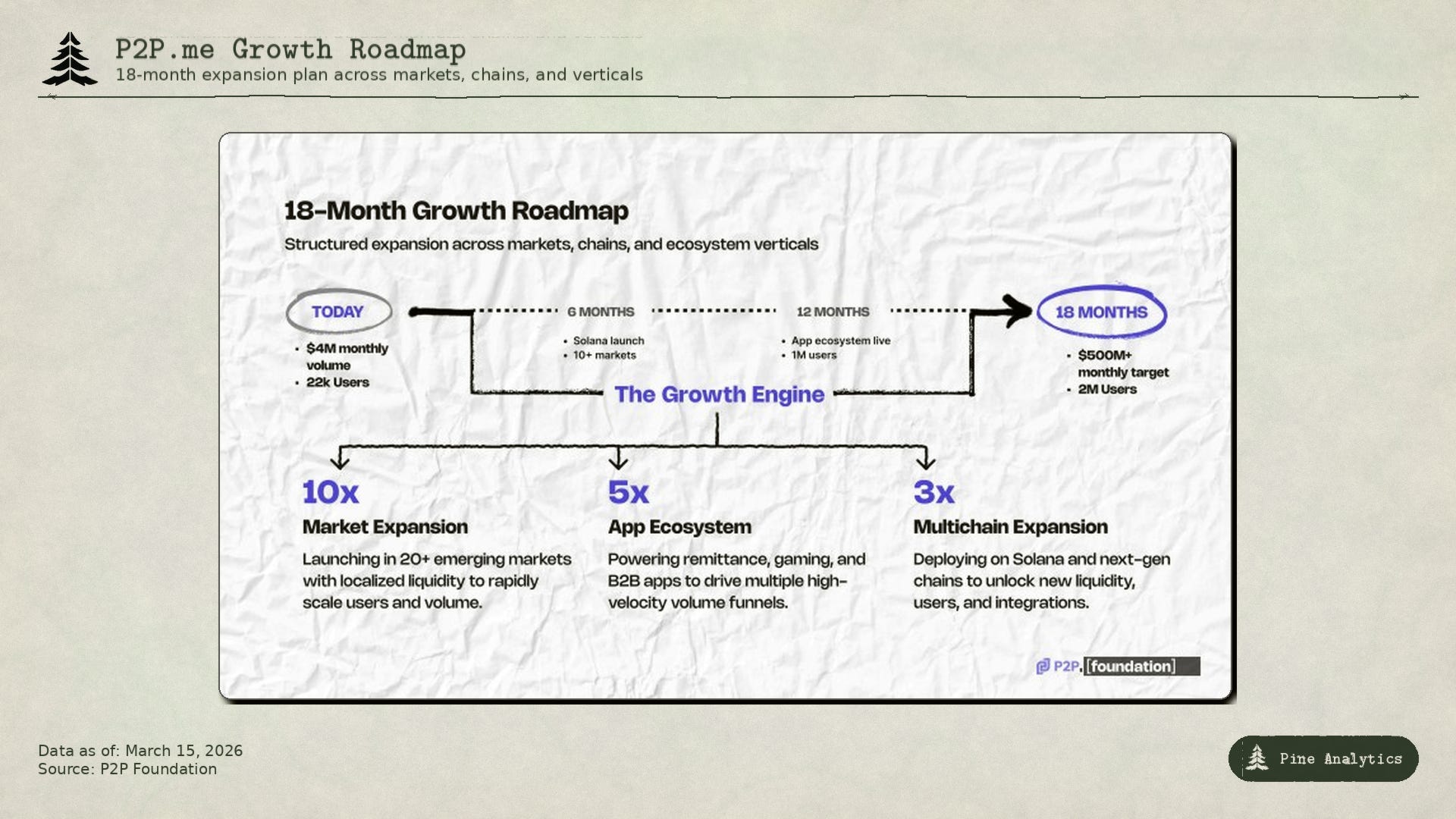

The TLDR pitch: It’s essentially a non-custodial P2P marketplace for converting USDC to local fiat rails (UPI, PIX, QRIS, ARS), similar to Binance P2P or LocalBitcoins, but with privacy-preserving identity verification, on-chain settlement and dispute resolution, and protections against bank-freeze risk. A Solana deployment is coming next.

App Use & Revenue

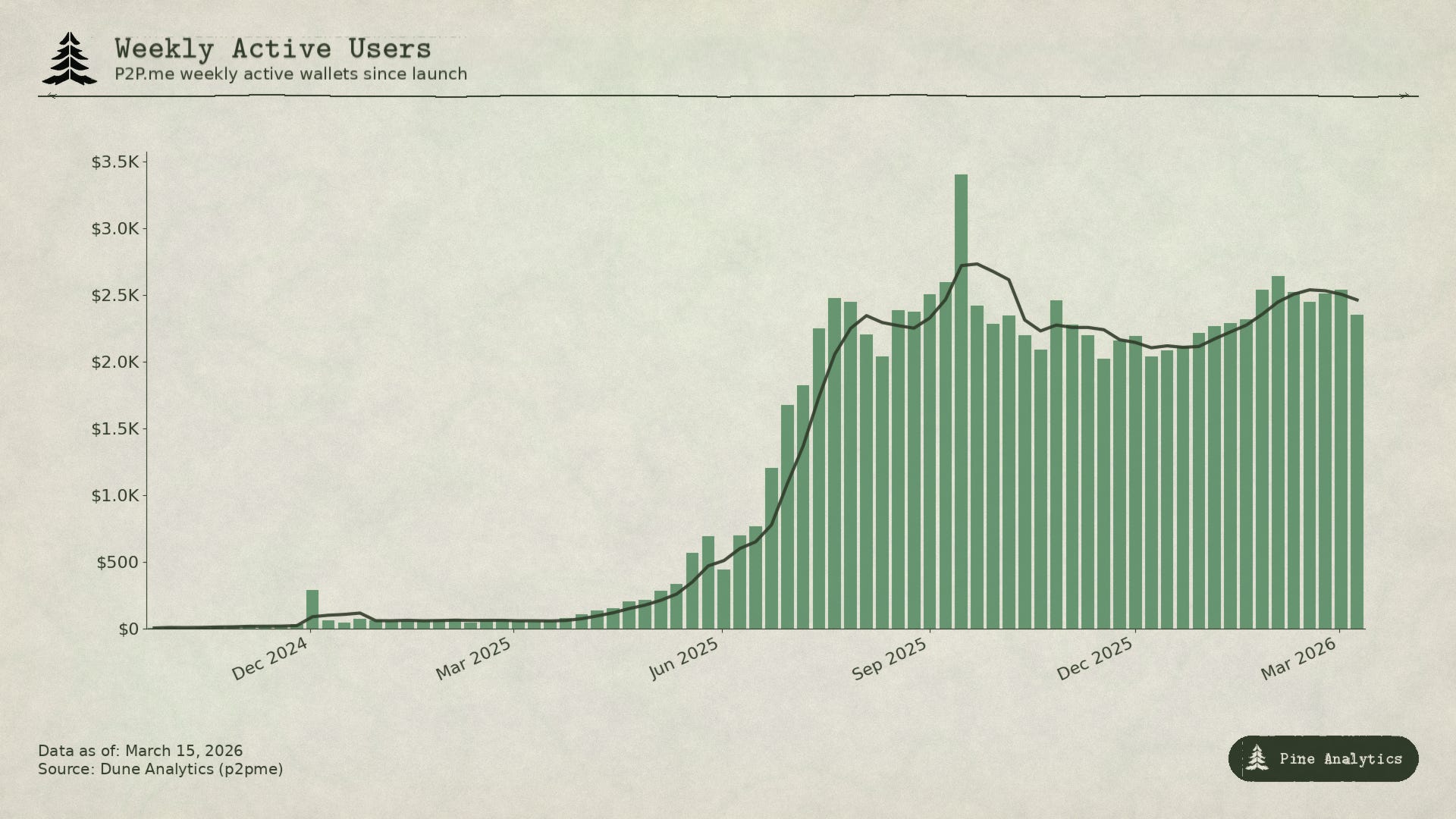

P2P.me has been live since mid-2023, processing $25K-$48K in monthly volume with a handful of users in its earliest months. Growth was modest through 2024, crossing $100K monthly volume and 100 users by December. The inflection came in early 2025 — volume jumped from $152K in January to $1M by June after the Pay feature launched, while weekly user signups surged from double digits to hundreds. Since then, both metrics have scaled sharply: monthly volume peaked at $3.95M in February 2026, total registered users crossed 23,000, and weekly actives have stabilized around 2,000-2,500 (~10-11% of the base).

Buy orders (fiat → USDC) consistently represent roughly half of volume, with the other half flowing out as Sell and Pay orders combined — Pay being functionally a Sell where fiat goes directly to a vendor via QR rather than back to the user’s bank. This balance between inflows and outflows suggests a healthy two-sided marketplace. The Pay feature has grown from zero to $1.3M monthly in under a year, signaling strong product-market fit for the “spend USDC at any QR” use case.

The user base is 78% India (18,071 users), 15% Brazil (3,382), 3% Argentina (656), and 1.4% Indonesia (332). India’s dominance tracks with UPI’s ubiquity and the bank-freeze problem P2P.me’s refund guarantee directly addresses.

On revenue: the protocol generated just ~$5K cumulatively in its first year, with several early months running negative. Revenue inflected alongside volume in mid-2025, jumping from $3.3K in May to $27.4K in August, and has since stabilized in the $34K-$47K monthly range. Cumulative protocol revenue reached $327.4K through mid-March 2026. Gross profit — protocol revenue minus merchant commissions — turned positive around August 2025 at $2.6K (9.6% margin), and has since ranged between $4.5K (mid-March 2026, 18% margin) and $13.3K (October 2025, 33% margin), with February 2026 at $7.1K (15.3% margin). The MetaDAO listing targets 20% gross margin contribution to the treasury from June 2026 — the numbers suggest they’re close but not consistently there yet.

Launch Info

P2P Protocol is launching the $P2P token via MetaDAO’s framework with a $6M target raise. Under this model, raised funds and minting authority go into a market-governed treasury controlled by token holders through futarchy-based governance — not the team.

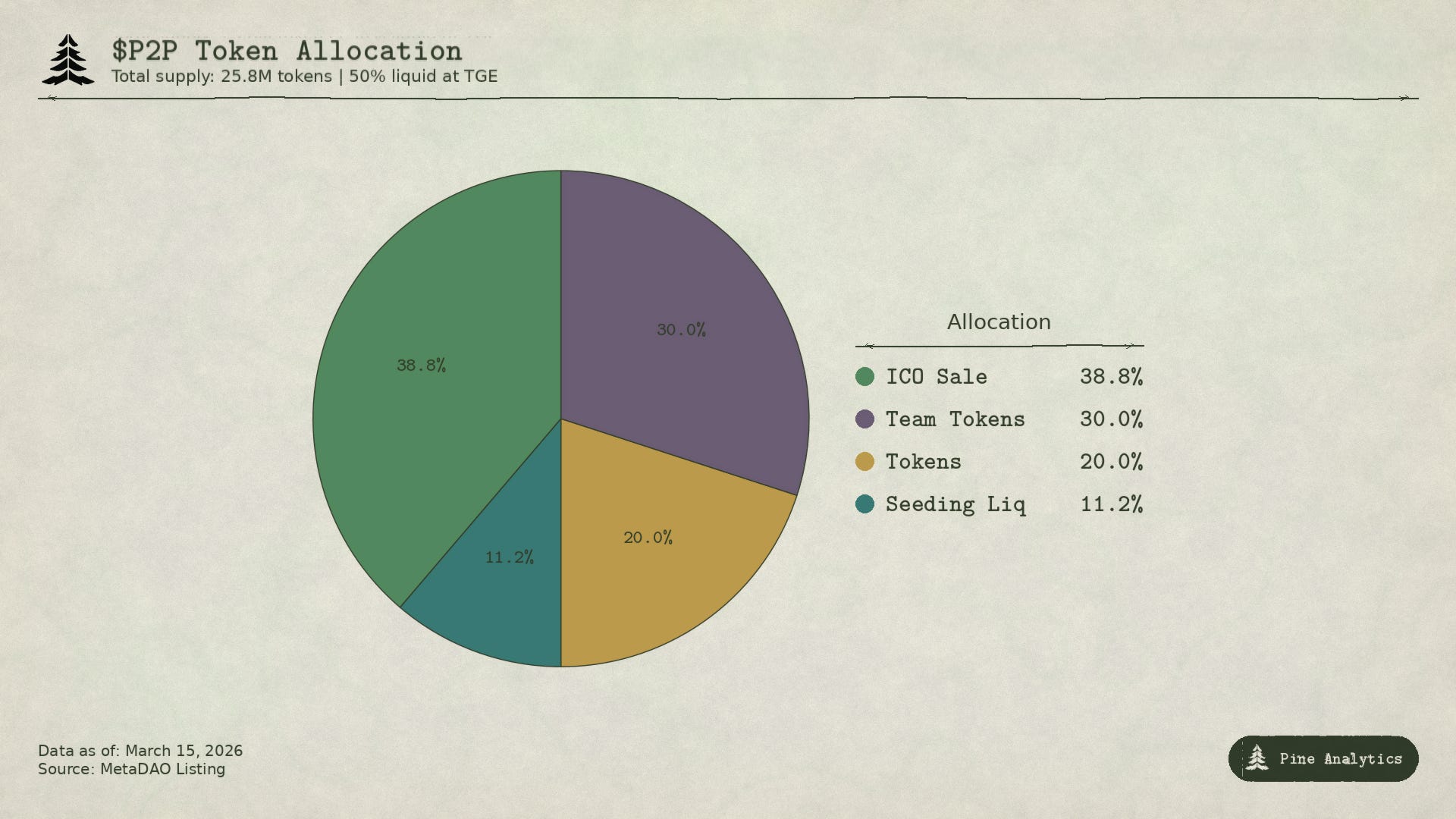

The total supply is 25.8M $P2P tokens. At TGE, 50% of supply will be liquid (10M from the ICO sale + 2.9M seeding liquidity), which is a notably high float for a token launch. No insider tokens unlock at TGE. At a $6M raise on 10M tokens, the implied ICO price is $0.60 per token, putting the fully diluted valuation at ~$15.5M.

Investor tokens (20% / 5.16M) are fully locked for 12 months, then unlock in five equal 20% tranches at months 12, 15, 18, 21, and 24. Locked tokens cannot be staked.

Team tokens (30% / 7.74M) are performance-based only with a 12-month cliff. Five equal tranches unlock at 2x, 4x, 8x, 16x, and 32x of the ICO price, measured via 3-month TWAP. The team only benefits if the protocol grows.

The protocol is requesting a $175K monthly allowance from the treasury, broken down as: $75K for team salaries (25 staff), $50K for growth and marketing, $35K for legal and operations, and $15K for infrastructure. At that burn rate, a $6M treasury gives roughly 34 months of runway. The MetaDAO listing targets 20% of protocol revenue flowing back to the treasury from June 2026 — at current rates that’s roughly $9.4K/month, extending runway to about 36 months but barely offsetting the burn. The protocol would need to scale monthly revenue to ~$875K before the treasury contribution alone covers operating costs, meaning the $6M raise is effectively the runway clock.

Our Concerns

Given the protocol is looking to raise at a $15M valuation, we have a handful of concerns around whether the protocol justifies this price.

First, although the protocol is doing around $500K in annual revenue at the current rate, most of this is eaten up by merchant fees, so the yearly gross profit at current rates is closer to $82K. This number matters more because it’s what the business itself actually captures — and at the valuation they’re planning to raise at, that’s roughly 182x their gross profit. They need to be growing at a rapid clip to justify that multiple.

Second is growth. Since the initial run-up in active users in mid-2025, the platform has seen no meaningful growth in daily active wallets for over six months. On top of this stagnant user growth, they plan to expand to 20+ countries with the money raised from MetaDAO. The data suggests that India makes up about 80% of their users and Brazil plus India account for the vast majority of their volume. In terms of numbers, they are nowhere near capturing all the possible customers in the jurisdictions they’re already in — and the additional jurisdictions seem to only be contributing marginally to usage. The concern is that if the focus is to spread across many countries, they’ll spread themselves thin and fail to build the network effects in any one jurisdiction that could really propel them into a fast growth rate.

Looking at the business overall, it’s hard to see why it’s a compelling buy at a $15M valuation where it’s trading at a large premium to its current cash flow and has a diffuse growth plan.

The Bull Case

In fairness, there are real arguments for why the current numbers understate the opportunity. The protocol has maintained 27% average month-on-month volume growth over 16 months — if that rate holds, the valuation math changes quickly. At 30% monthly growth (the rate used in their own projections), monthly volume hits $333M by mid-2027, and even a modest take rate on that volume would dwarf the current $82K gross profit. The B2B SDK launching in June 2026 is a potential step-change: if wallets and fintechs embed P2P.me’s rails, volume could scale without the protocol needing to acquire users directly. The Circles of Trust model — where local operators stake $P2P to onboard merchants in new countries — could also make geographic expansion cheaper and more organic than a traditional go-to-market push. The team token structure genuinely aligns incentives (no unlock below 2x ICO price, 12-month cliff), and the MetaDAO framework means the treasury can’t be rugged. And the TAM is undeniably massive — billions of people in emerging markets need a path between fiat and stablecoins, and centralized alternatives like Binance P2P carry real custodial and censorship risk. If P2P.me captures even a fraction of that market, $15M looks cheap in hindsight.

The question is whether you’re buying the current business or the optionality — and at what price that optionality is worth paying for.