Polymarket Fee Rollout

Revenue Impact and Market Implications

Executive Summary

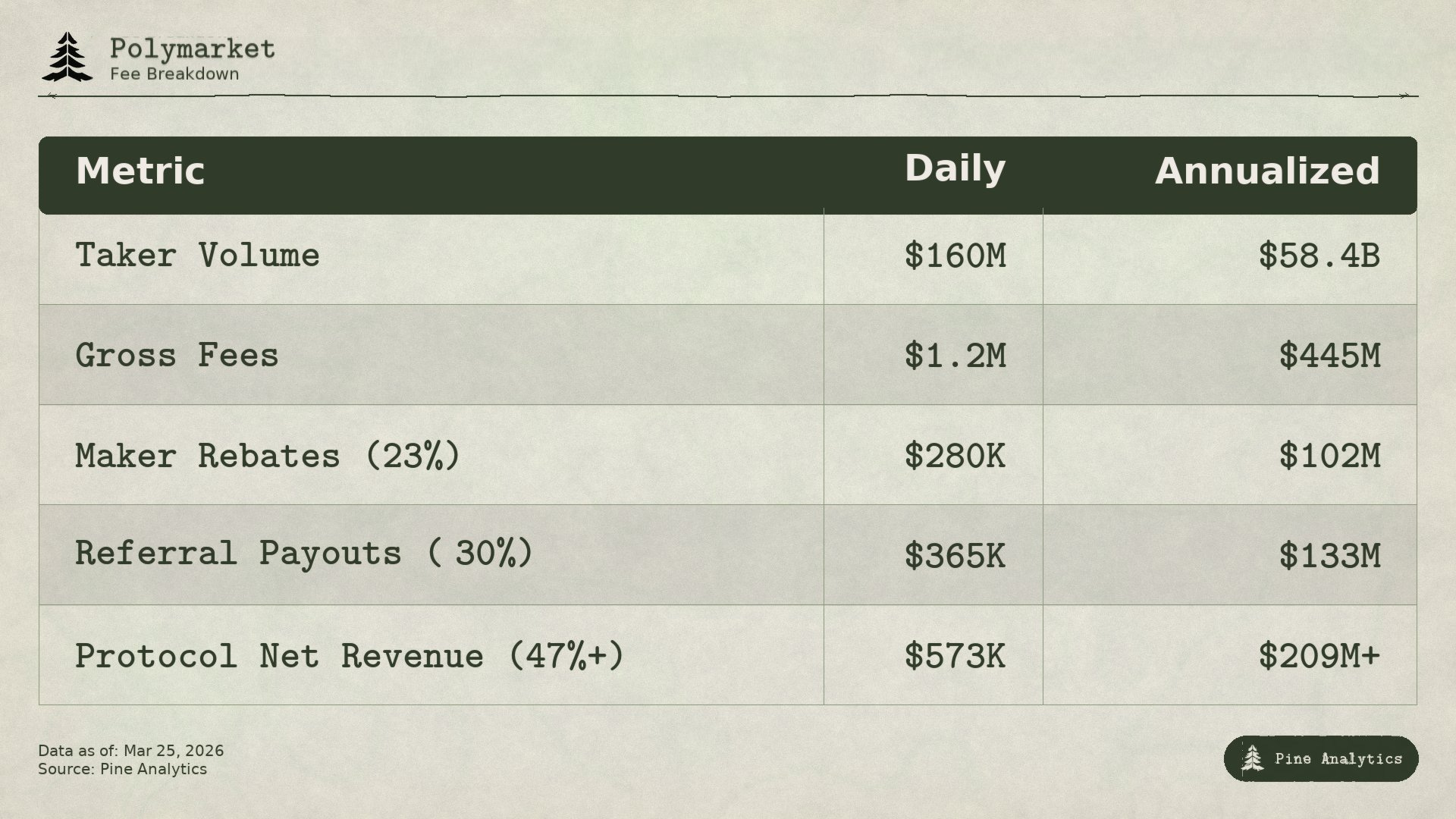

@Polymarket is rolling out taker fees across nearly all market categories on March 30, 2026, expanding a fee structure that currently only applies to Crypto and Sports markets. Using on-chain data from Dune Analytics and Polymarket’s published fee parameters, we estimate that the platform will generate approximately $1.2M in daily gross fee revenue at current volume levels (~$160M/day in taker volume). After accounting for maker rebates and referral payouts, protocol net revenue is estimated at $573K per day, or roughly $209M annualized. Early evidence from the Crypto and Sports fee rollouts suggests the impact on trading volume is modest, with Sports markets showing no volume decline and Crypto markets seeing only a slight pullback that falls within normal variance.

How Polymarket’s Fee Structure Works

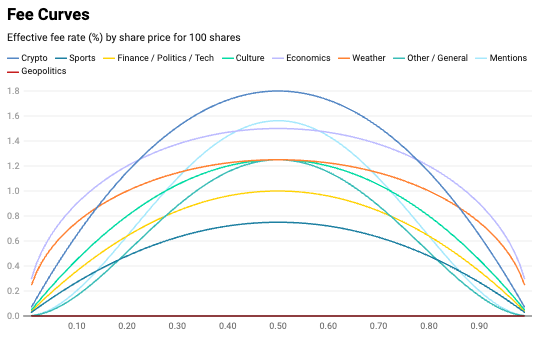

Polymarket uses a dynamic taker-only fee model. Makers (liquidity providers who place resting orders) pay nothing and instead receive rebates. Takers (traders who hit existing orders) pay a fee that varies based on the probability of the market they are trading. The fee is calculated using the formula: fee = C x p x feeRate x (p x (1 - p))^exponent, where C is the number of shares and p is the share price between 0 and 1.

This creates a bell-shaped fee curve that peaks at 50% probability, where uncertainty is highest, and drops toward zero at the extremes. A trade at 95 cents (95% implied probability) incurs a negligible fee, while a trade at 50 cents pays the maximum rate. Geopolitics and world events markets remain completely fee-free.

The peak effective fee rates by category after the March 30 rollout are as follows:

Crypto — 1.80%

Sports — 0.75%

Finance — 1.00%

Politics — 1.00%

Economics — 1.50%

Culture — 1.25%

Weather — 1.25%

Tech — 1.00%

Other/Mentions — 1.25–1.56%

Geopolitics — 0%

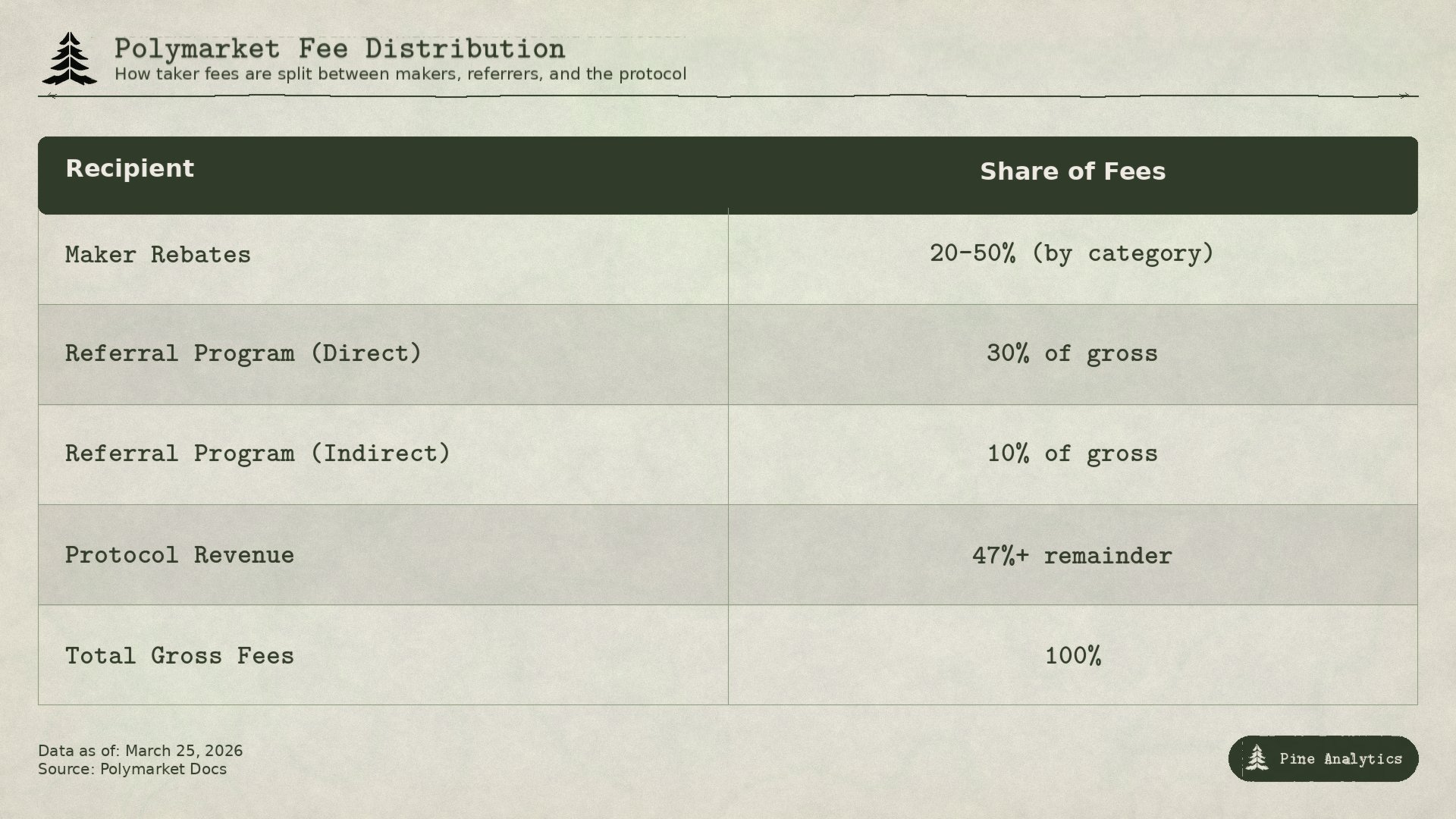

Fee Distribution

Collected taker fees are split three ways. First, a category-specific portion (20% for Crypto, 25% for most categories, 50% for Finance) is allocated to the Maker Rebates Program, paid daily to liquidity providers in proportion to their filled maker volume. Second, Polymarket runs a referral program that pays referrers 30% of gross taker fees generated by direct referrals and 10% from indirect referrals. The remaining balance is retained by the protocol. In practice, since not every trade is referred, the protocol’s actual share is likely higher than the base 47% implied by the math.

Early Evidence: Volume Impact of Fees

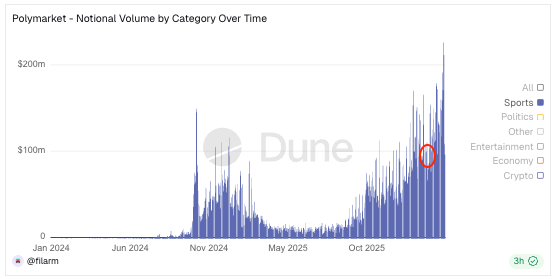

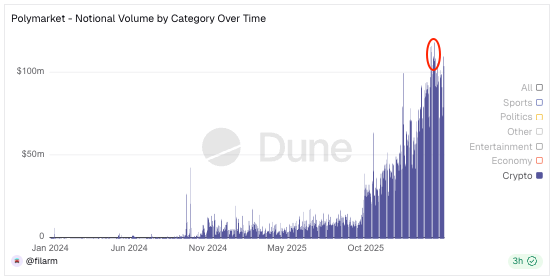

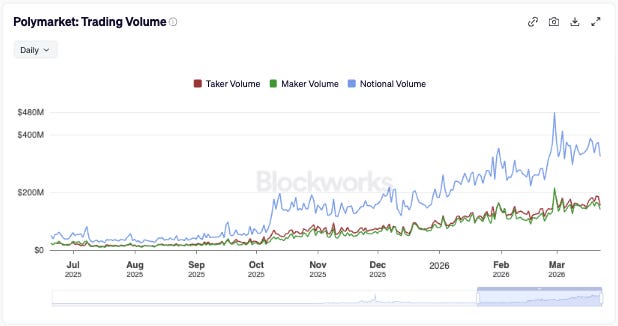

Fees first went live on Crypto markets on January 5, 2026, initially limited to 15-minute contracts and later expanded to all crypto timeframes by March 6. Sports market fees launched on February 18. This gives us roughly two months of data on Crypto and one month on Sports to assess the volume impact.

Crypto markets saw a brief volume spike around the fee expansion in early March, reaching $100-120M in daily volume, before settling back to a range of $73-100M. While this represents a modest pullback, it falls within the normal variance of Crypto market volumes and is difficult to attribute definitively to fees after only 18 days of data. Sports markets, on the other hand, have been completely unfazed. Volume has actually increased from the $100-150M range to $150-250M per day since the fee introduction.

One likely explanation for the divergence is the fee differential: Crypto’s peak rate (1.56%, rising to 1.80%) is roughly 3.5x higher than Sports (0.44%, rising to 0.75%). The remaining categories being added on March 30 have peak rates that fall between these two, suggesting any volume impact is likely to be minor. Additionally, the maker rebate program creates a structural incentive to backfill any liquidity gaps, since market makers are now being paid to provide liquidity rather than doing so for free.

Revenue Estimates

Methodology

To estimate fee revenue, we first needed to understand where on the probability curve trades are actually occurring. We queried the last 7 days of on-chain trade data from Polymarket’s CTF Exchange contract on Polygon using Dune Analytics, calculating the volume-weighted average position on the fee curve relative to the theoretical maximum at 50% probability. Because the fee formula uses different exponents by category, which changes the shape of the curve, we calculated this separately for each exponent value. For exponent 1 categories (Crypto, Sports, Politics, Finance, Culture, Tech), the average trade captures 70.1% of the peak fee. For exponent 2 categories (Other/General, Mentions), it drops to 59.7% since the steeper curve penalizes off-center trades less. For exponent 0.5 categories (Economics, Weather), it rises to 80.2% since the flatter curve means traders pay closer to the max rate even at skewed probabilities.

We then applied the appropriate factor to each category’s peak fee rate and multiplied by recent daily taker volume. Taker volume (~$160M/day) represents the actual USDC changing hands per trade, roughly half of the ~$350M notional volume figure that Polymarket reports, which counts the full $1 face value of each share traded.

Results

Across all categories, the blended effective fee rate comes to approximately 0.76% of taker volume. At current levels, this produces the following estimated daily and annualized figures:

One important caveat: the referral figure represents the maximum payout assuming every trade comes through a referral link. In practice, the protocol’s net take is likely meaningfully higher than $209M annualized, with the true figure falling somewhere in the $209-342M range depending on referral program adoption.

Competitive Context

The implementation of fees on existing markets has had a slightly negative to negligible effect on the growth trajectory, and the maker rebate structure creates built-in incentives to compensate for any minor shortfall in liquidity. For context, @Pumpfun currently generates roughly $1M per day in net protocol revenue and @HyperliquidX sits around $2M per day. Post-transition, Polymarket’s estimated net protocol revenue of ~$580K per day (after maker rebates and referral payouts) puts it at roughly 60% of pumpfun and 30% of Hyperliquid on a like-for-like basis. Notably, the referral payout assumption is a ceiling since not every trade is referred, so the real protocol take likely sits closer to $580K-$950K per day depending on referral adoption. At the upper end of that range, Polymarket is already approaching pumpfun’s net revenue. If Polymarket continues even half of its recent growth trajectory, which has seen roughly 200% volume growth over the past six months, it could match pumpfun on a net basis and close the gap with Hyperliquid by September.

Among large cash-producing applications in crypto, Polymarket’s growth profile currently looks among the strongest. The combination of expanding product categories, mainstream media integrations (including the X/Twitter partnership), regulatory normalization through the ICE investment, and a fee structure designed to minimize friction while maximizing maker incentives positions the platform well for sustained revenue generation.