PURR: The Hyperliquid Beta Play

Generally at Pine Analytics we like to keep our research right-curve: cashflows, adoption, competitive dynamics, and other fundamentals. This piece is a departure. We’re going to make a memecoin thesis. The token is PURR, the native community token on Hyperliquid, and we think the risk-reward here is asymmetric enough to warrant a closer look at what is, on the surface, a cat-themed meme token with no stated utility.

The HYPE Wealth Effect and PURR as the Beta Play

Hyperliquid is positioning itself as one of the fastest horses among L1s in this cycle. The protocol generates more revenue than most chains with a fraction of the token float, the buyback mechanics are aggressive (97% of trading fees flowing into HYPE buybacks), and the ecosystem is still in its early innings relative to where Solana or Avalanche were at comparable stages of development. If and when BTC makes a decisive move higher and capital rotates into alts, HYPE is sitting in a structurally favorable position to outperform: low circulating supply, strong revenue backing, no VC selling pressure, and a user base that has already demonstrated willingness to hold through volatility.

When that move happens, the downstream effect is predictable. A sharp repricing of HYPE creates a wealth effect among its holders, and that new liquidity needs somewhere to go. Historically in crypto, wealth effects within an ecosystem flow into the highest-conviction ecosystem-native assets first. Holders don’t rotate into random Ethereum DeFi tokens or Solana memecoins. They look for beta within the ecosystem they just got rich in.

PURR is the largest market cap and highest volume native Hyperliquid token other than HYPE itself. There is no other liquid, high-profile asset on the chain that can absorb a meaningful bid from HYPE holders looking for leveraged ecosystem exposure. It trades on the native spot orderbook, it has real depth from HIP-2 liquidity, and it has the brand recognition of being the first token ever deployed on the chain. For someone who wants to express a continued bullish thesis on Hyperliquid’s growth without simply buying more of the L1 token, PURR is effectively the only game in town at any meaningful size.

What is PURR

PURR came into existence via an airdrop to Hyperliquid points holders following the first stage of HIP-1, which enabled native tokens and spot trading. It was basically a technical proof of concept: Hyperliquid needed to demonstrate that HIP-1 (their native token standard) and HIP-2 (their permissionless liquidity mechanism) actually worked on mainnet. PURR was the guinea pig, a cat-themed meme token deployed to stress-test the infrastructure before other projects launched spot tokens on the chain. It went live on April 16th, 2024.

The max supply was 1 billion. 500 million were distributed proportionally to points holders based on a snapshot. 400 million initially deployed as HIP-2 liquidity were burned. The remaining ~100 million sits in the liquidity pool. Zero went to VCs, team, or any private sale. The token is deflationary, as trading fees paid in PURR are burned, bringing the current circulating supply to roughly 598 million.

The points that determined your allocation were mostly earned through Season 1 perps trading activity: volume, number of transactions, funding fees paid, and similar metrics. The Hyperliquid team deliberately kept the exact calculations opaque to prevent gaming and whale monopolization of the distribution.

Who Holds PURR Today

The original airdrop recipients were the same cohort that went on to receive the massive HYPE airdrop in November 2024. When HYPE launched at ~$2 and ran to double digits within a week, that user base was sitting on five- and six-figure HYPE allocations that dwarfed the value of their PURR. They had every incentive to sell: PURR was a test token with no stated utility, and they had just received a far more valuable allocation from the same platform.

A significant portion did sell. That means the current holder base skews toward two groups: conviction OGs who held through the entire cycle, and market buyers who actively accumulated PURR on the secondary market with real capital. Both represent stickier, more intentional ownership than the original distribution. Compare this to most memecoins, where the launch distribution is the holder base (insiders, snipers, and early LPs), or to protocol tokens with large VC and team allocations on vesting schedules. PURR has neither problem. There are no locked team tokens, no VC overhang, and the airdrop recipients who didn’t want to be there have already cycled out. What remains is fully circulating, deflationary supply held by users who chose to be there.

PURR/HYPE Ratio: The Rotation Is Over

The PURR/HYPE ratio tells the entire story in a single chart. The ratio peaked around 0.025-0.028 in late 2024, when PURR was the only liquid way to express a bullish Hyperliquid thesis. Once HYPE launched and you could own the L1 token directly, the proxy trade was no longer necessary. The ratio bled roughly 90% as holders rotated out of PURR and into HYPE.

But the chart has entered a fundamentally different regime over the last three to four months. The ratio has flatlined at approximately 0.0024, and it has held that level while HYPE has been one of the strongest performing assets in all of crypto. A flat ratio during a period of significant HYPE outperformance means PURR has been matching HYPE’s dollar returns move for move, without any idiosyncratic catalyst of its own.

The structural selling pressure is exhausted. Every holder who wanted to swap PURR for HYPE has already done it. What remains is a holder base choosing to hold PURR despite months of opportunity to exit into a ripping L1 token. In market structure terms, the chart reads as a textbook transition from a prolonged markdown phase to an accumulation phase. Even a modest mean reversion in the ratio to the 0.005-0.008 range, still 70-80% below the prior highs, would represent a 2-3x outperformance versus HYPE from current levels. The ratio doesn’t need to reclaim anywhere near its peak for the trade to work.

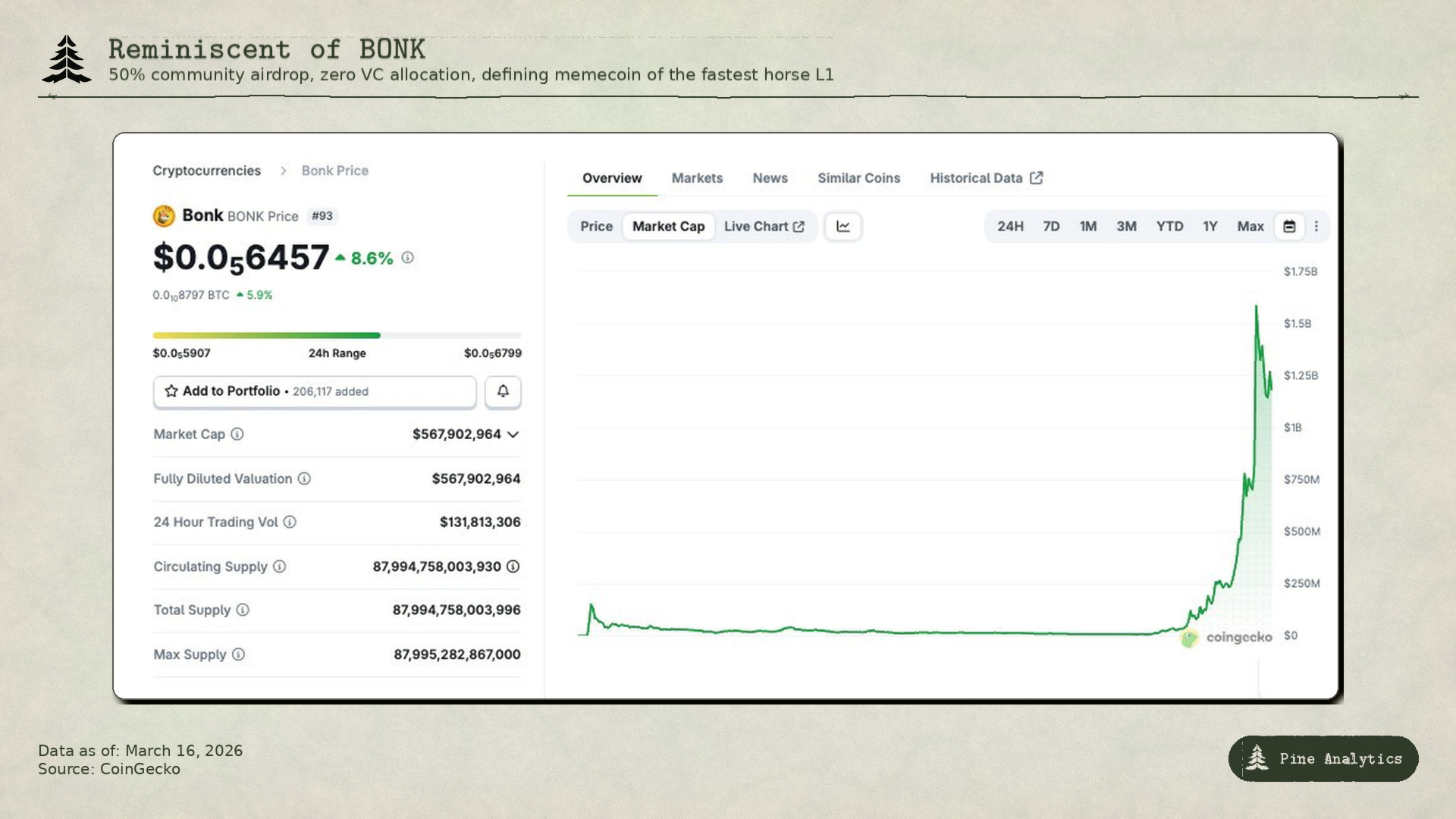

Reminiscent of BONK

The parallels between PURR and BONK are hard to ignore. Both launched via community airdrops with 50% of supply distributed freely and zero VC allocation. Both were deployed during pivotal moments for their respective L1s: BONK arrived on Christmas Day 2022 to revive Solana post-FTX, PURR launched in April 2024 as Hyperliquid’s first native spot token. Both experienced an initial spike followed by an extended bleed. And both emerged as the defining memecoin of the L1 that is arguably the fastest horse in its respective cycle.

BONK’s recovery is instructive. After bleeding 96% from its January 2023 peak, BonkBot launched in November 2023, and the combination of a product catalyst plus Solana’s macro recovery produced an 11,500% move in roughly two months. Over the following two years, BONK was integrated into over 100 Solana dApps and the team retroactively built a product suite (BonkBot, LetsBonk, Bonk Arena) to justify and sustain the market cap that community energy had already created.

PURR’s structure differs in ways that cut both directions. There is no PURR team, no DAO, no dedicated contributors. On the upside, this means no team tokens, no vesting schedules, and no treasury that could be sold into the market. BONK carried a 20% early contributor allocation vesting over three years. On the downside, PURR has no one actively building products or driving integrations. If Hyperliquid’s growth stalls, there is no team to adapt or create new reasons for the token to matter. PURR’s fate is entirely tethered to Hyperliquid’s trajectory in a way that BONK’s never was to Solana alone.

The bet is that PURR doesn’t need a team because Hyperliquid’s own growth functions as the product. Some new Hyperliquid-native projects have chosen to airdrop to PURR holders (HFun allocated 30% of its supply to them, for example), and HIP-1’s technical design makes it easy for deployers to do so, but this is at each project’s discretion rather than a protocol guarantee. Trading fees burn supply passively, and the token’s position on the strict list gives it native legitimacy that ecosystem projects have so far chosen to build around. Whether that convention holds is the open question. BONK needed two years and 22 contributors to build its ecosystem moat. PURR is betting that being the first and largest native token on a fast-growing L1 can do the same work without anyone at the wheel.

Risks

PURR’s liquidity is thin. The token trades under $1M in daily volume, which is fine for small positions but would struggle to absorb a serious bid without significant slippage. If the wealth effect thesis plays out, the liquidity constraints could work in PURR’s favor on the way up, but they work against you just as hard on the way out.

The entire thesis is contingent on HYPE continuing to outperform. If Hyperliquid loses momentum, whether through a competitor shipping faster, a security incident, or simply failing to maintain its revenue trajectory, PURR doesn’t have an independent value proposition to fall back on. It’s levered beta on HYPE, and levered beta cuts both ways.

There is nothing stopping the Hyperliquid team or ecosystem from rallying around a different token. PURR’s position as the de facto community asset is a convention, not a protocol-level guarantee. A new token with an active team, a treasury, and a real product could emerge on Hyperliquid and absorb the attention and capital that currently defaults to PURR. The strict list offers some protection here, but it’s not a permanent moat.

Finally, this is a memecoin. There is no revenue, no product, and no team. The thesis rests on structural positioning, supply dynamics, and reflexivity, which are real factors, but they don’t generate cashflows and they don’t compound. If the macro move doesn’t come or the wealth effect rotation skips PURR entirely, this token can sit at these levels or bleed lower for a long time with nothing to backstop it.

"The Hyperliquid team deliberately kept the exact calculations opaque to prevent gaming and whale monopolization of the distribution."

Great article, very interesting. I asked Claude to give me more details on Hyperliquid's plan/thinking/initial structuring and it just linked to back to your post four times. Do you have any suggestions of where to look for case study like info on crypto reward structuring?