STRC Volatility Is the On/Off Switch for BTC's Largest Marginal Buyer

Executive Summary

Strategy’s STRC preferred stock is already one of Bitcoin’s largest marginal buyers, rivaling the entire U.S. spot ETF complex during peak weeks. Unlike ETFs, the flow is one-directional: every dollar of STRC issuance buys BTC, and no amount of STRC selling forces BTC liquidation. But the current scale is just the starting point.

The longer STRC maintains low volatility, the more this engine can grow. Low vol means tighter haircuts in margin frameworks, which means more leverage capacity, which means larger institutional allocations, which means more issuance, which means more BTC buying. Each month of stability extends the track record, opens new buyer pools, and compounds the flywheel. With $21 billion in fresh ATM authorization, the ceiling for this bid is far above where it sits today.

The risk is equally reflexive. STRC can only issue above its $100 par value. A major volatility event that breaks the peg kills the issuance engine, and with it, one of the largest systematic bids in the Bitcoin market. A routine ex-dividend dip in March paused issuance entirely and collapsed weekly BTC purchases from 17,994 to 1,031. A real credit event would do far worse.

STRC volatility is the variable that determines whether this demand source grows or disappears. It belongs on the BTC dashboard.

What STRC Actually Is

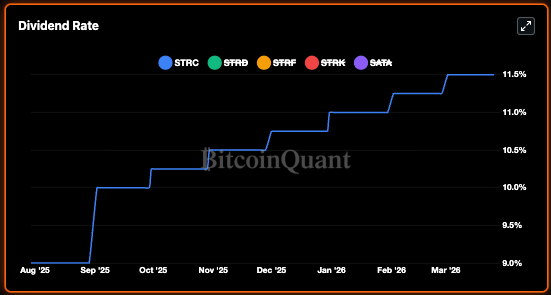

STRC, or “Stretch,” is a variable-rate perpetual preferred stock issued by Strategy (formerly MicroStrategy), the largest publicly traded holder of Bitcoin with 762,099 BTC on its balance sheet. The instrument pays a monthly cash dividend at an annualized rate of 11.5% and is designed to trade near its $100 par value. When the price dips below par, the board raises the dividend rate to attract buyers. When it trades above par, the rate can be lowered.

The critical mechanic: Strategy can only issue new STRC shares through its at-the-market (ATM) program when the stock trades at or above $100. Every dollar issued above par becomes capital used to buy Bitcoin. STRC does not exist to pay a dividend. It exists to buy Bitcoin. The dividend is the cost of keeping the machine running.

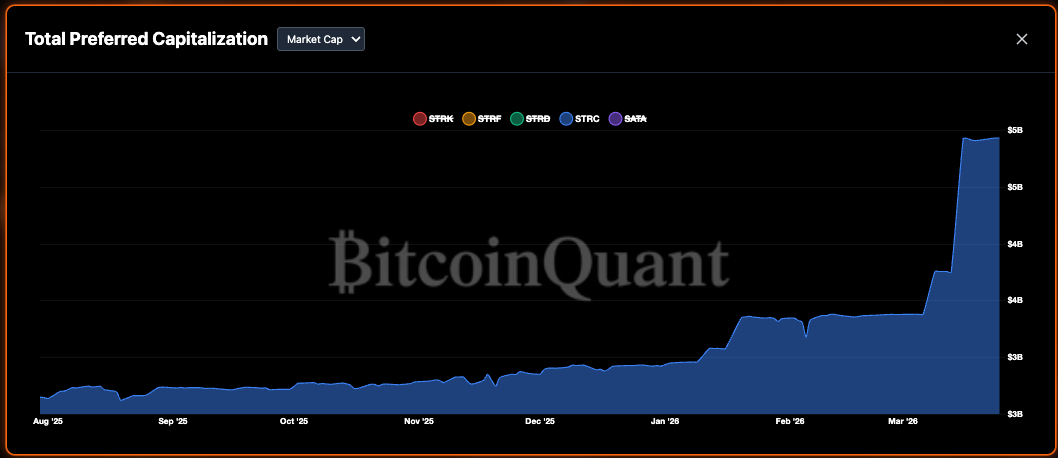

Since its July 2025 debut, Strategy has raised $5.02 billion through STRC and recently authorized an additional $21 billion in issuance capacity.

STRC Is Rivaling the Entire ETF Complex as a Marginal BTC Buyer

During the week of March 9-15, 2026, STRC ATM sales generated $1.18 billion in proceeds. Strategy used those proceeds (combined with MSTR common stock sales) to purchase 17,994 BTC at an average price of $70,946. Over that same period, the combined net inflows across all 12 U.S. spot Bitcoin ETFs totaled approximately $763 million.

STRC alone was a larger marginal buyer of Bitcoin than BlackRock’s IBIT, Fidelity’s FBTC, and every other spot ETF combined.

The comparison undersells the point, because ETF flows are bidirectional. On January 29, the entire ETF complex posted negative $817.8 million. When ETF investors sell, authorized participants redeem shares and sell Bitcoin into the market. STRC does not have this mechanic. When STRC holders sell their shares, they sell into the equity market. Strategy does not sell Bitcoin to meet redemptions because there are no redemptions. The BTC goes in and does not come out.

This is a structurally one-directional flow. Every dollar of STRC issuance creates a Bitcoin bid. No amount of STRC selling creates a Bitcoin ask.

Volatility Is the Circuit Breaker

STRC’s rolling volatility is the single best real-time indicator of whether this bid is active. The connection runs deeper than ATM mechanics.

In collateral and leverage markets, the lower an asset’s observed volatility, the more leverage it can support. Prime brokers, clearinghouses, and repo desks set haircuts based on historical volatility using VaR models calibrated to rolling lookback windows. An asset with 2% rolling vol gets a smaller haircut than one with 18% vol. Smaller haircut means more borrowing capacity per dollar of collateral. More borrowing capacity means more capital deployed against the position.

As STRC’s 30-day rolling vol has compressed from 18% to 2%, every institution holding it gets progressively more room to size up. Funds running leveraged carry trades can take larger positions. Treasuries can justify larger allocations because risk models show less potential drawdown.

But the more important mechanism is temporal. Each additional month that STRC holds near par at low vol extends the track record that margin models use. Compliance teams get more comfortable. New buyer pools open up that were waiting for exactly this kind of demonstrated stability before entering. The instrument graduates from “novel crypto-adjacent product” to “yield instrument with a proven volatility profile,” and each graduation unlocks a new tier of capital.

Each new tier of capital creates more ATM issuance, more BTC buying, a stronger balance sheet, better credit quality, and more STRC stability. The reflexive loop feeds on its own history. The longer it runs, the stronger it gets.

This is why STRC vol is the master variable. It governs ATM issuance pace directly, leverage and sizing capacity indirectly, and the rate of new capital formation over time.

What to Watch

STRC vol belongs on the BTC dashboard alongside ETF flows and exchange balances.

30D rolling volatility is the primary signal. Any sustained move above 5% would indicate the rate adjustment mechanism is losing its grip and issuance capacity is being impaired.

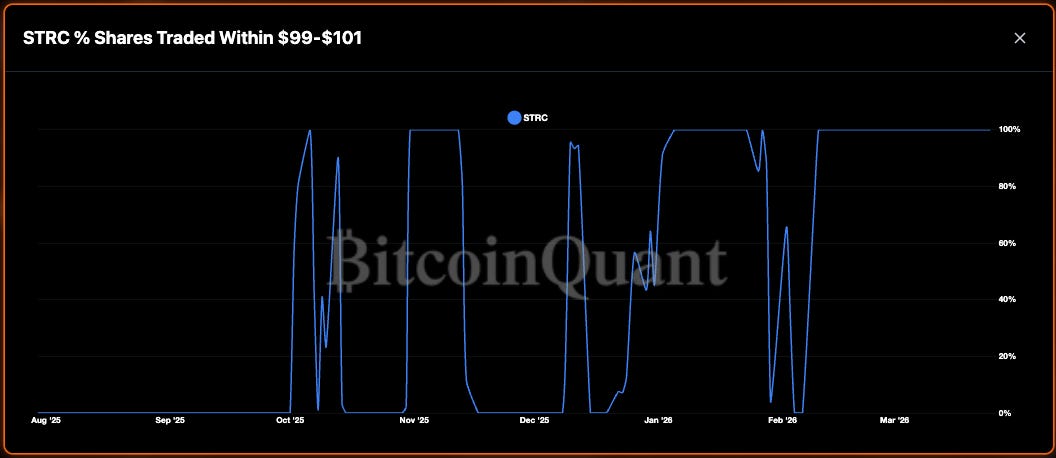

The $99-$101 trading band is the early warning. BitcoinQuant tracks the percentage of shares trading within this range, which has been near 100% recently. A breakdown in this band precedes an issuance pause.

Daily volume vs. 30D average signals demand intensity. The current 30D average is $221 million. Sessions well above average suggest accelerating institutional demand. Sessions well below suggest the bid is thinning.

Ex-dividend recovery time is the recurring stress test. Each monthly ex-dividend date pushes STRC below par temporarily. The speed of recovery (currently 9-10 trading days) measures underlying demand strength. If recovery starts taking 15 or 20 days, the issuance window shrinks and the BTC bid weakens proportionally.