The Bear Case for Bittensor (TAO)

Introduction

Bittensor’s native token TAO trades at approximately $275 with a $2.6 billion market cap and $5.8 billion FDV. The project has institutional backing from Grayscale (S-1 filed December 2025 for a NYSE-listed ETF), a public endorsement from NVIDIA CEO Jensen Huang, and a compelling supply narrative: a 21 million hard cap with a Bitcoin-style halving schedule. The first halving in December 2025 cut daily emissions from 7,200 to 3,600 TAO. Subnet count has grown from 32 to 128 in a year, and Templar’s Covenant-72B training run proved decentralized compute can produce benchmark-competitive language models.

This report does not dispute any of that. It examines whether the network’s economics can generate demand-side revenue at a scale that justifies current valuations, and how its competitive positioning holds up against centralized providers and self-hosted compute.

How Value Flows Through the Network

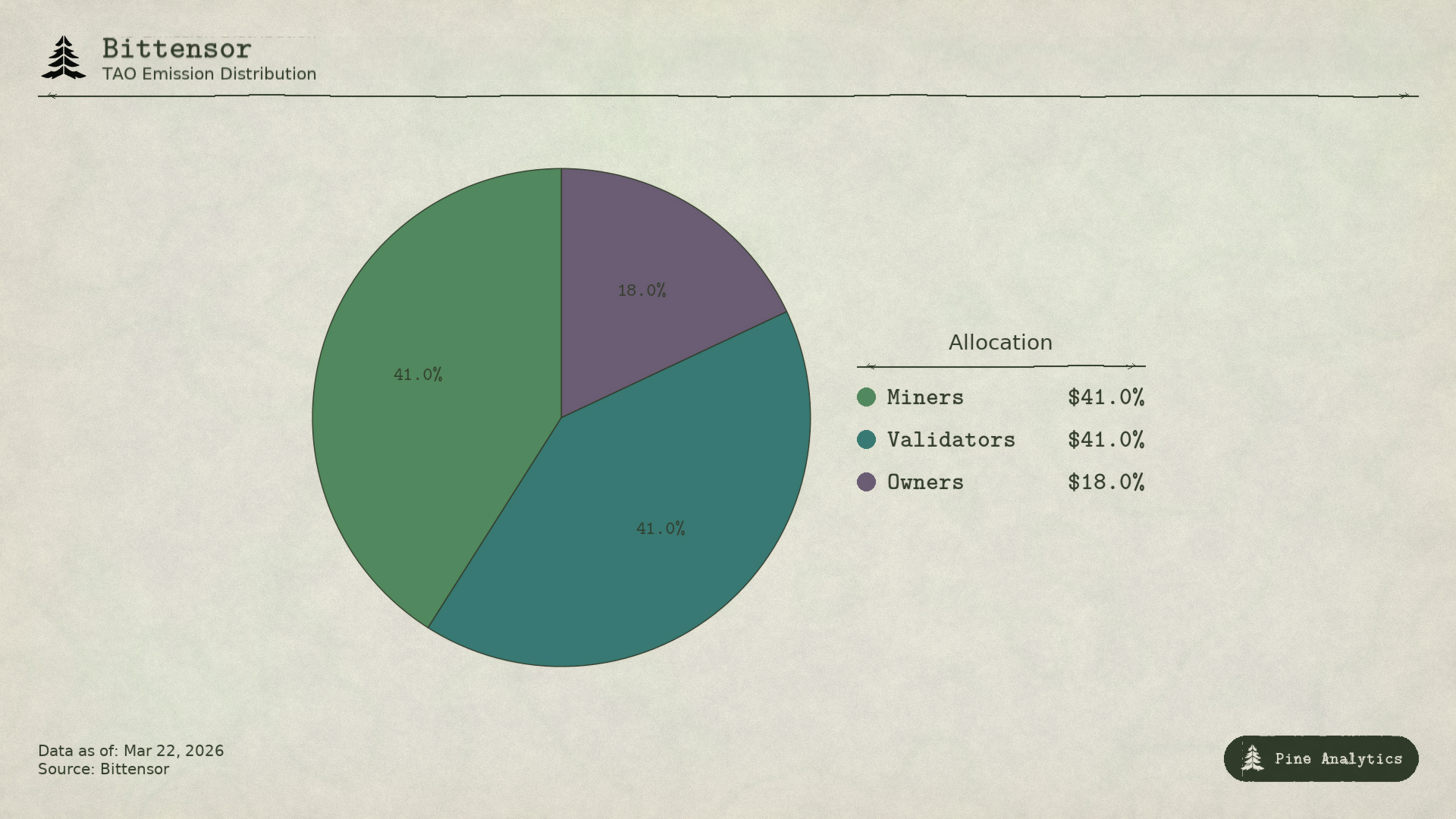

Bittensor has four participant classes. Subnet owners create specialized AI marketplaces and receive 18% of their subnet’s TAO emissions. Miners perform AI work (inference, training, data processing) and receive 41%, totaling approximately 1,476 TAO per day (~$406,000 or $148 million annualized). Validators score miner output and receive 41%. Stakers allocate TAO into subnet liquidity pools, receiving subnet-specific alpha tokens. Under the Taoflow model, a subnet’s emission share is determined by its net TAO staking inflows. Subnets with negative flows receive zero emissions.

TAO is the universal entry currency. Mining registration, validator staking, subnet token purchases, and service payments all require it. Subnet activity theoretically creates structural demand for the base token.

The Demand Side

Supply Transparency vs. Demand Opacity

Bittensor’s supply economics are transparent. Daily emissions of 3,600 TAO are split programmatically: 41% to miners, 41% to validators, 18% to subnet owners. The halving schedule is hard-coded. Staking ratios (~70% of supply), emission shares, and flow data are all on-chain. The top 10 subnets control roughly 56% of total emissions.

The demand side has no equivalent transparency. There is no aggregated dashboard tracking external revenue by subnet. AI service delivery (inference requests, compute jobs, training calls) happens off-chain and is not recorded on the blockchain. Investors infer demand from proxy metrics: staking flows, subnet token prices, and self-reported figures from individual teams. This opacity is structural, not temporary. The blockchain records token movements, not API calls.

What follows is the most complete demand-side picture available as of March 2026.

Chutes (SN64): The Subsidy Behind the Savings

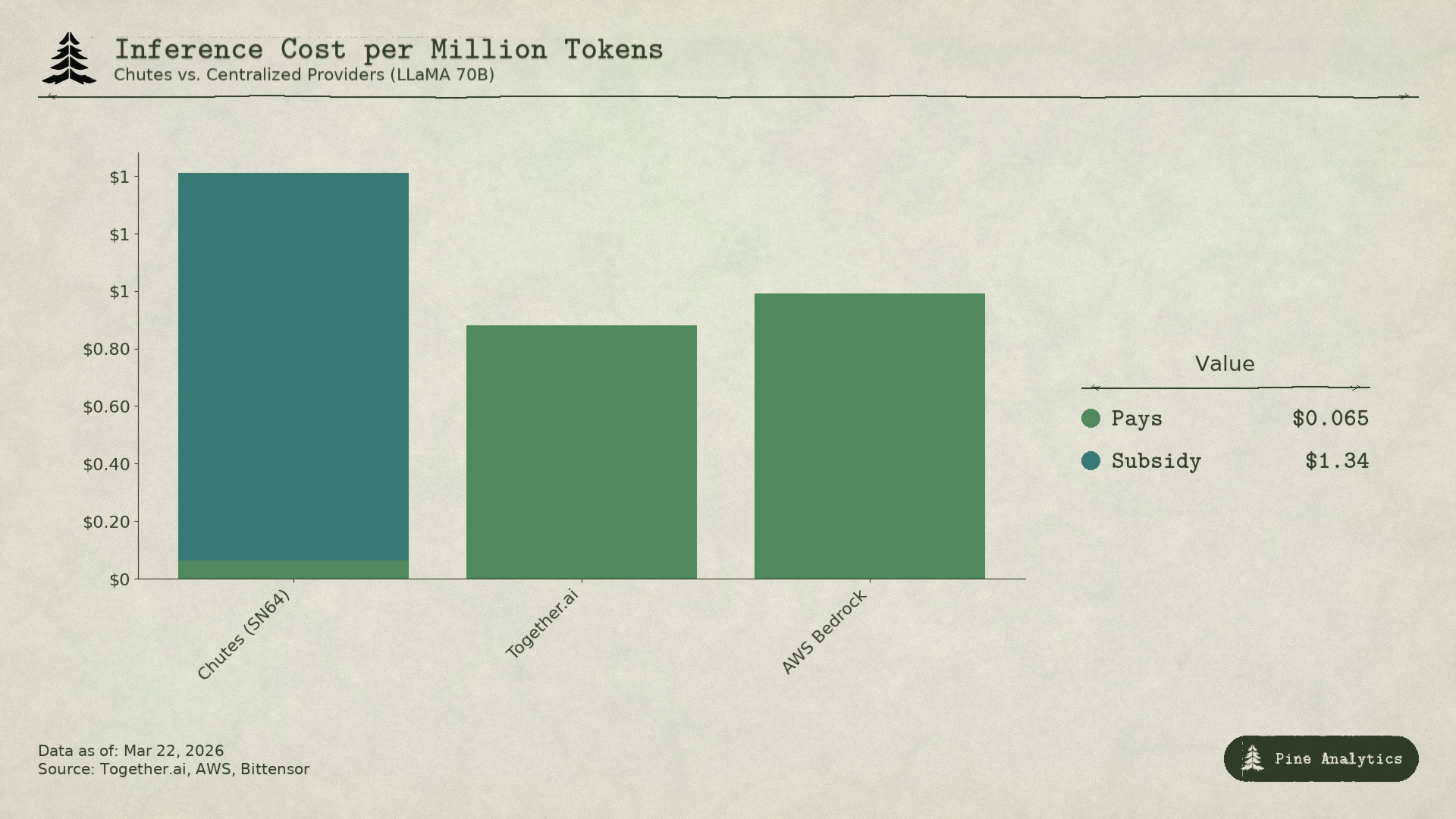

Chutes commands 14.4% of network emissions, the highest of any subnet. Developed by Rayon Labs, it offers serverless inference on open-source models (DeepSeek, Mistral, LLaMA) at prices reported to be 85% below AWS and 10-50% below Together AI. Usage metrics are the ecosystem’s strongest: 400,000+ users (100,000+ via API), 5M+ daily requests, 9.1 trillion tokens processed, and daily token generation that surged from 6.6 billion to 101 billion over three months. Chutes ranks as a top inference provider on OpenRouter, outperforming some centralized competitors on specific models.

The pricing, however, does not reflect operational efficiency. It reflects subsidy. At 14.4% of emissions, Chutes receives approximately 518 TAO per day, worth roughly $142,000 or ~$52 million annualized. This flows to the subnet's miners, validators, and owner. Against that, estimated external revenue is approximately $1.3-2.4 million per year (the higher figure self-reported by the Chutes team to DL News in October 2025; the lower from a March 2026 estimate, neither independently audited). The protocol subsidizes the subnet's operations at a ratio of roughly 22-40:1. For every dollar customers pay, the network contributes $22-40 in TAO emissions.

The implications become clear when you model what pricing would look like without the subsidy. Chutes processes approximately 101 billion tokens per day. If miners had to cover their costs from customer revenue alone, they would need to recoup that ~$142,000 daily from token throughput. That implies an unsubsidized price of roughly $1.41 per million tokens.

Current market rates for the same open-source models: Together.ai prices LLaMA 3.3 70B Turbo at approximately $0.88 per million tokens. DeepSeek V3 runs at $0.40-0.80 across competitive providers. Smaller models go as low as $0.18 per million. At $1.41 per million, unsubsidized Chutes pricing would be 1.6-3.5x more expensive than centralized alternatives. The cost advantage does not narrow. It inverts entirely. The 85% savings that headline every Chutes discussion are funded by TAO holders through inflation, not by any structural efficiency of decentralization.

When emissions halve again (projected late 2026 or 2027), either pricing roughly doubles, miners leave the subnet, or the gap between subsidy and revenue widens further. The obvious rebuttal is that this resembles standard startup bootstrapping: subsidize early to build network density, then raise prices once users are locked in. Uber, DoorDash, and AWS all ran this playbook. The difference is that those companies built switching costs during the subsidy period (proprietary platforms, driver networks, enterprise integrations). Bittensor subnets build none. The models are open source, the APIs are standard, and users can migrate to any provider serving the same weights with zero friction. When the subsidy shrinks, there is no lock-in to prevent churn.

Rayon Labs also operates SN56 (Gradients) and SN19 (Nineteen), together commanding ~23.7% of total emissions. Neither has disclosed external revenue figures. A single team controls nearly a quarter of the network’s incentive distribution.

Targon, Templar, and the Rest

Targon (SN4) is the highest-revenue subnet. Operated by Manifold Labs ($10.5M Series A), it provides confidential GPU compute to enterprise customers. Estimated annualized revenue is ~$10.4 million against a ~$48 million valuation, implying a 4.6x revenue multiple. This is the most grounded valuation in the ecosystem. However, the $10.4 million is a projection cited across multiple analyst reports, not an audited number. Multiple researchers have flagged the absence of a live revenue dashboard excluding emissions as a transparency concern.

Templar (SN3) completed Covenant-72B (72B parameters, 1.1T tokens, 67.1 MMLU) and carries a $98 million market cap. It generates zero external revenue. Training APIs and enterprise sales are described as “in motion” but no paid product has launched.

The remaining 120+ subnets either have no reported external revenue, are pre-product, or operate primarily on emission capture. Celium (SN59) claims revenue but has published no figures. Nineteen AI (SN19) has disclosed no data.

The Aggregate Picture

Total identifiable demand-side revenue across the entire network is approximately $3-15 million annually, with the range reflecting the difference between verified revenue (Chutes’ ~$2.4M) and unaudited projections (Targon’s ~$10.4M). A single subnet’s emission subsidy (~$52M for Chutes alone) exceeds the upper bound of what the entire network generates in external revenue.

Against a $2.6 billion market cap, this implies a ~175-200x revenue multiple. Against FDV of $5.8 billion, ~400x. Centralized AI infrastructure companies (CoreWeave, Lambda) were valued at 15-25x forward revenue in recent rounds. High-growth SaaS rarely sustains above 50x. Bittensor’s implied multiple is 4-10x higher than the most aggressively valued comparable in either crypto or traditional infrastructure.

The gap between valuation and demand-side economics reflects a market pricing TAO almost entirely on supply-side scarcity (halving, staking lock-up), institutional catalysts (Grayscale ETF, exchange listings), and AI sector sentiment rather than demonstrated economic productivity. These are real price drivers. But they are distinct from a thesis that Bittensor is generating sustainable value as an AI services network.

The Pricing Vise

Subnets face margin compression from two directions simultaneously.

Self-hosting caps pricing from above. Every model on Bittensor is open source. Weights are on Hugging Face. A single H100 serves a 70B model at ~$40-50/day all-in. Tools like vLLM and Ollama have made local deployment trivial. NVIDIA’s roadmap (Blackwell, Rubin) is designed to reduce inference cost per token by orders of magnitude. Self-hosting offers unlimited inference with no token friction, no counterparty risk, and no network dependency. Any organization with sufficient volume is already cheaper running locally.

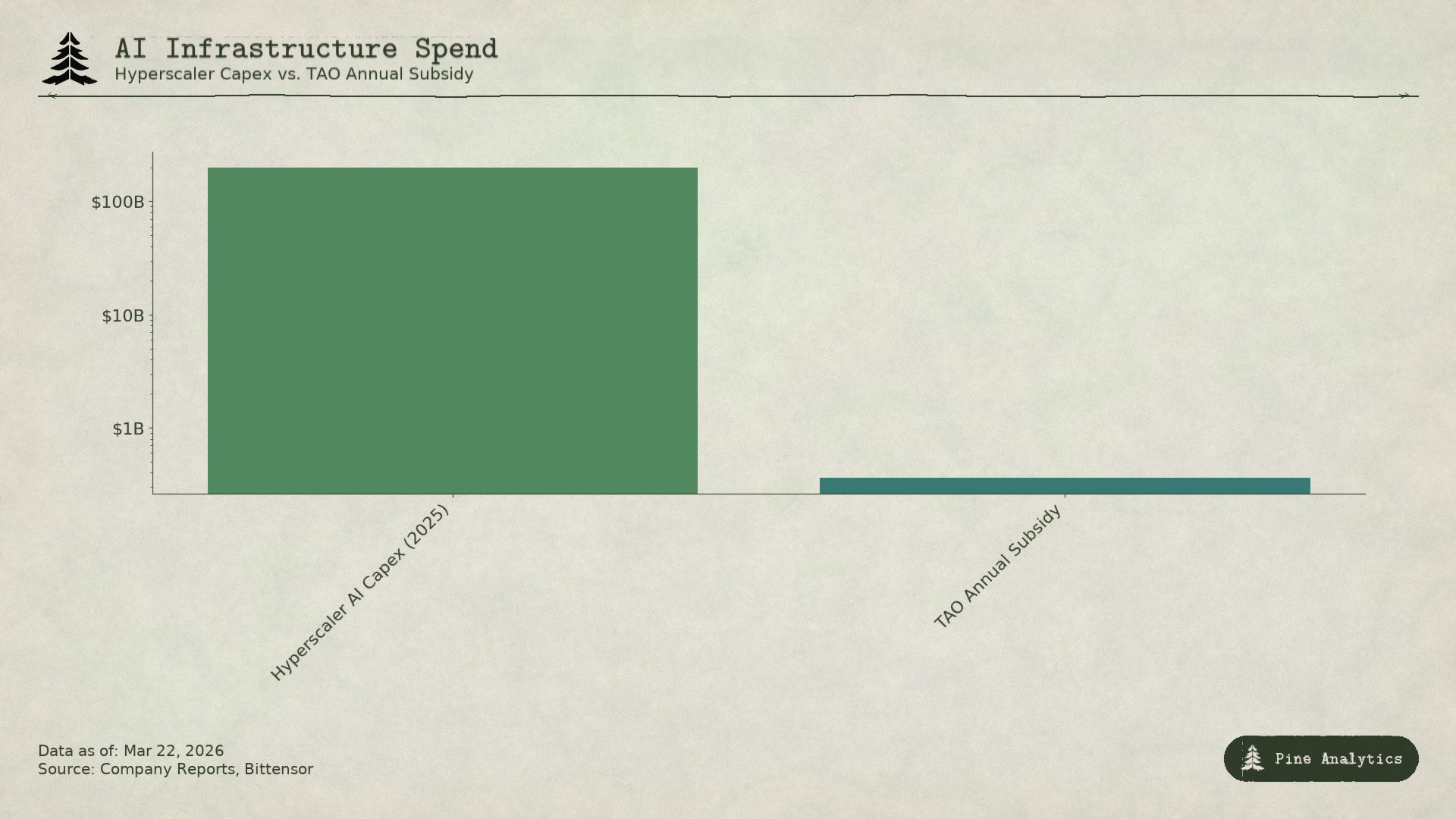

Hyperscalers compress from below. Microsoft, Google, Amazon, and Meta collectively invested over $200 billion in AI capex in 2025. They have first-priority hardware allocation, purpose-built data centers, existing enterprise relationships, and the ability to subsidize AI from adjacent cash flows. Bittensor’s entire annual incentive budget (~$360 million) is less than what Microsoft spends on AI infrastructure in a week. Specialized providers (Together.ai, Fireworks, Groq) compete on the same open-source models with VC-subsidized pricing.

Subnets must price between these two boundaries while absorbing costs unique to decentralization: token friction, validator overhead, subnet owner fees, and network latency.

The Moat Problem

If a subnet develops a valuable service, the underlying model and methodology are publicly available by design. Covenant-72B is Apache-licensed. SparseLoCo is on arXiv. Any competitor can replicate the approach without participating in the TAO economy.

Traditional moats (proprietary technology, network effects, switching costs, brand) do not apply. The technology is open. Network effects accrue to TAO, not individual subnets. Switching costs are zero when every provider serves the same weights. The community argues the incentive mechanism is the moat, but that requires the emission budget to remain large enough to attract compute, and it shrinks with every halving.

What TAO Is Pricing

At $2.6 billion, TAO is not priced on demand-side fundamentals. $3-15 million in annual revenue does not support it under any conventional framework. The market is pricing Bitcoin-like scarcity, the Grayscale ETF catalyst, AI sector rotation, and long-term optionality on decentralized AI. These are legitimate speculative factors. They are also entirely supply-side and sentiment-driven.

A TAO position based on scarcity and narrative may perform well regardless of demand economics. A position based on Bittensor becoming a meaningful AI services network requires evidence that does not yet exist and faces structural headwinds that may prevent it from materializing. Investors should be clear about which thesis they hold.