The Bull Case for $META

A Personal Antidote

I woke up this morning to a sea of green and red across memecoins I’d never heard of. After some digging, here’s what’s happening: developers are using Claude Code to spin up apps and launching tokens on Bags. A fresh batch of “Claude coins” is running up—only to peak at mid-eight figures, crater 80%+ within 24 hours, and watch the next wave repeat the cycle, topping out around $8M before their inevitable march toward zero.

Being four days late to this meta it doesn’t seem worth playing. My timeline is flooded with people insisting that Claude Code founders are about to launch the next billion-dollar runner. All I see is an echo of an echo—a negative EV game of chicken that nobody without DEX Screener open 24/7 has touched since March 2024.

Here’s the uncomfortable truth: no slop Claude Code app from a mediocre developer is going to be the next billion-dollar runner. If it were actually a good app, nobody would refer to it as “a Claude Code app”—it would just be an app. And any developer whose coin runs to $100M has exactly one incentive: rug it, pocket a bag, and call it a day.

All of which is to say: the memecoin game, like the NFT game before it, is circling the drain. It’s not coming back—at least not in this form.

But here’s my tension: I still want to buy low-cap coins. I still want to play the game of finding the next runner. The problem is that the current mechanics simply aren’t compelling to anyone who isn’t either (a) a sophisticated on-chain warrior glued to their screen, or (b) an insider. With each iteration, the marginal user gets burned harder, and the pool of willing participants shrinks.

What MetaDAO Stands For (My Perception)

With each iteration, tweak, and new mechanism, Prophet and Kollan are honing in on a vision where founders who are serious about what they’re building—and want to put real skin in the game—are able to raise capital from the internet with low friction, work on their vision, and be held accountable to delivering what they promise to the people who helped them pursue it. In turn, investors get the peace of mind that founders’ incentives align with theirs, and if they believe the founders and their teams are unable or unwilling to execute on the vision they set out to complete, they can claw back what remains of their contribution. This version isn’t fully complete yet, but it’s within sight.

MetaDAO Today

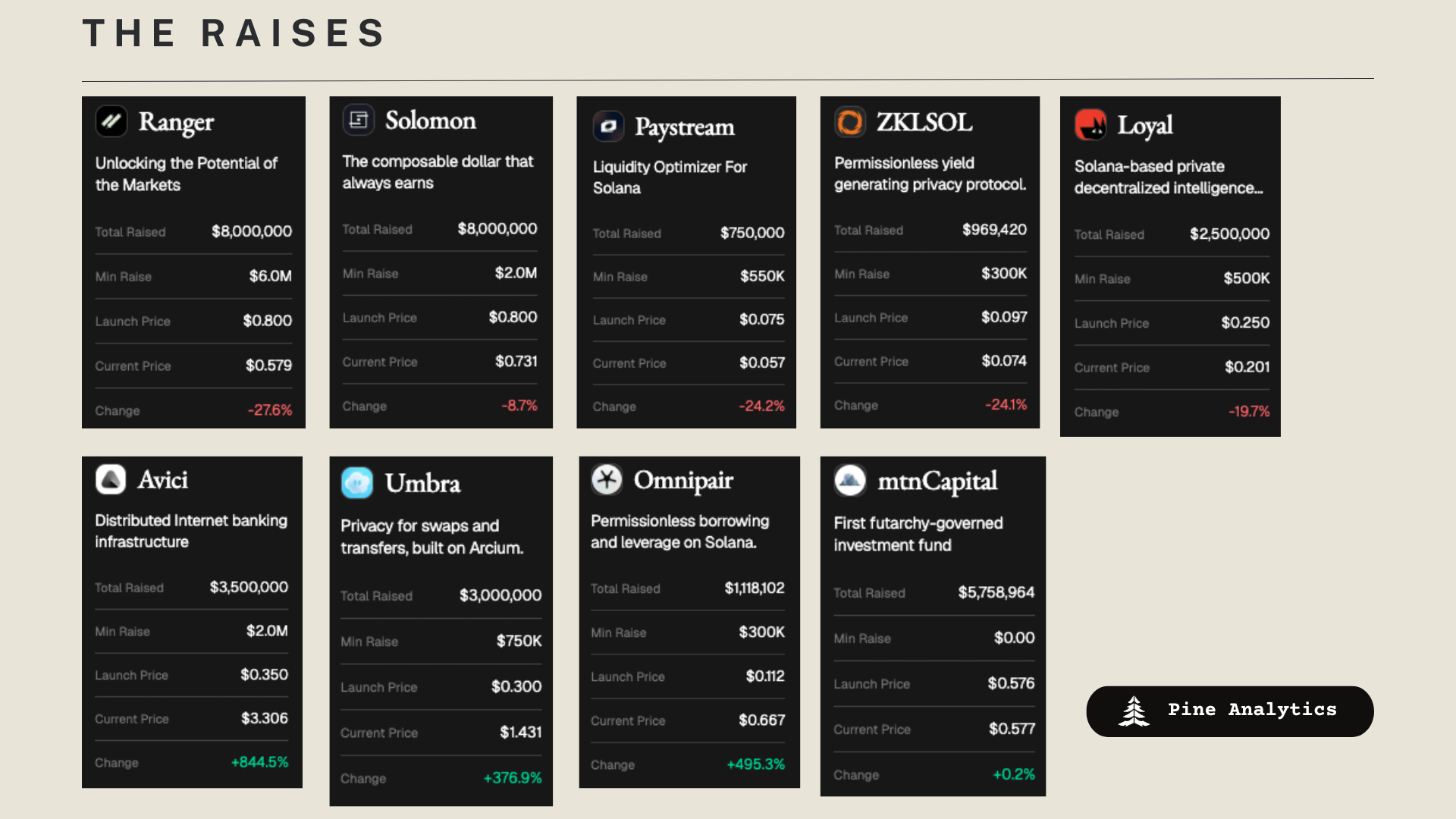

The Raises

So far there have been 9 tokens launched on the MetaDAO launchpad. Of these raises, 1 is essentially flat, 5 are down, and 3 are up from the ICO price. On average, if a participant invested equally into each MetaDAO ICO launch, their portfolio would be up 194% from the initial amount invested. This is staggeringly strong performance given that 8 of the 9 ICOs happened since October 2025.

The mechanism for participation in these raises allows as much money to be deposited as people want. If the total amount deposited exceeds the team’s minimum raise amount, the team can opt to take more than their minimum, and all deposits receive a share of the raise token proportional to their contribution relative to the total amount raised. In practice, these raises have been getting many multiples of the minimum raise deposited, and teams are opting to take slightly more than their minimum raise target.

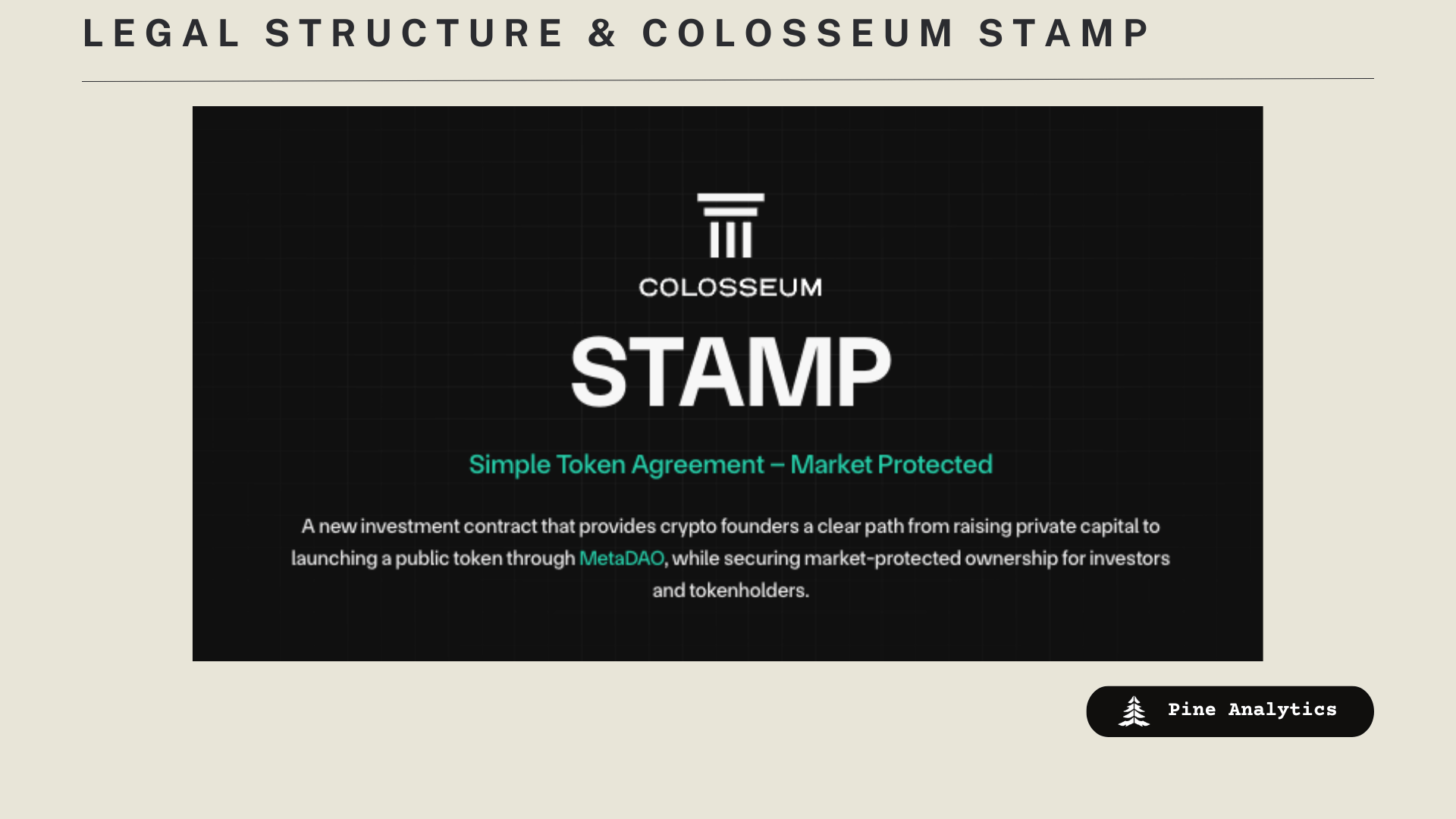

The DAO’s Legal Structure & Colosseum STAMP

MetaDAO’s DAO Legal Structure: Projects launched on MetaDAO form DAO LLCs, typically in the Marshall Islands via MIDAO. This hybrid wrapper integrates on-chain futarchy governance directly into the legal operating agreement. The LLC holds treasury, IP, contracts, and assets, providing tokenholders with enforceable control, liability protection, and “unruggable” features—preventing team misappropriation while allowing market-driven decisions on capital, minting, and exits.

Colosseum STAMP: Launched in December 2025 by Colosseum (a Solana accelerator) in partnership with MetaDAO and law firm Orrick, the STAMP (Simple Token Agreement, Market Protected) is an investment contract for crypto startups. It replaces complex dual equity/token structures (e.g., SAFEs/SAFTs) by making the token the sole economic unit. Founders raise private capital via STAMP, committing to a public token launch on MetaDAO’s futarchy-governed platform. This ensures aligned incentives, on-chain protections for treasuries and IP via decision markets, and fair public access—bridging private funding to protected, market-governed ownership.

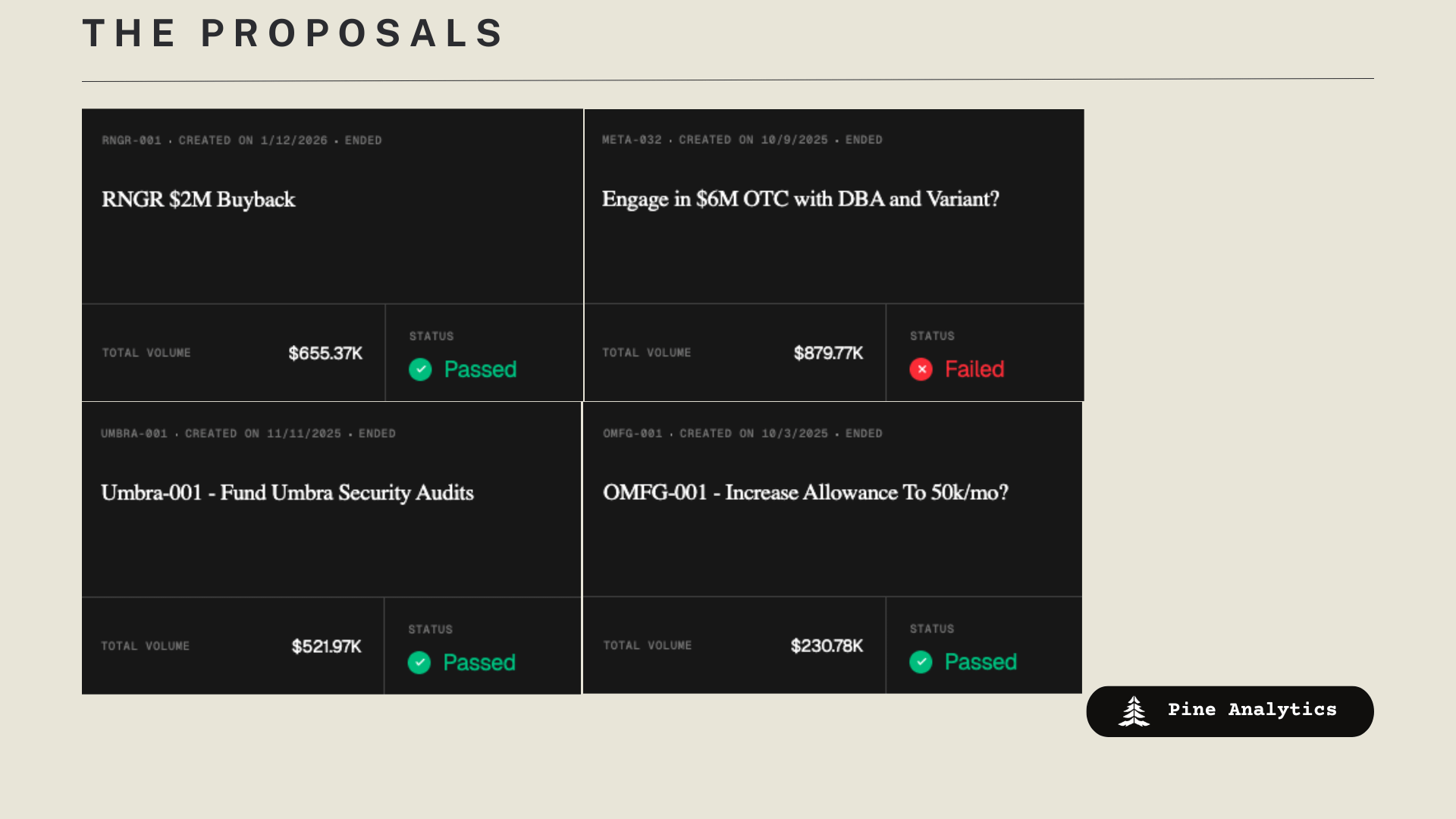

The Proposals

The DAOs that launch on MetaDAO adopt futarchy as their proposal process rather than traditional token voting. Breaking down futarchy is outside the scope of this article, but to give a brief synopsis: people vote with commitments to buy or sell tokens if proposals pass or fail. This allows people with measurable conviction to hold higher weight in the voting process.

Teams have a monthly spending allowance and cannot withdraw more money from the treasury than their allowance unless a proposal explicitly changes it or allows a one-time withdrawal. The proposals that have been submitted fall into four general categories:

First, proposals to use the treasury to buy back the token. These generally occur when tokens are trading below the project’s NAV and are nearly always accepted by people arbitraging the price.

Second, adjustments to the team’s spending allowance. These have passed pretty universally.

Third, one-time spend proposals for things like audits. These also pass without much friction.

Fourth, proposals to buy protocol tokens. These have usually failed if the proposer tries to buy below current market price.

The translation is this: if the token is trading below NAV, the market will be punitive and quickly try to arbitrage this with a buyback proposal. If the tokens are trading well above NAV, the market lets the team increase spending as they see fit with no major pushback. And the markets do not let people acquire the project’s tokens for cheap.

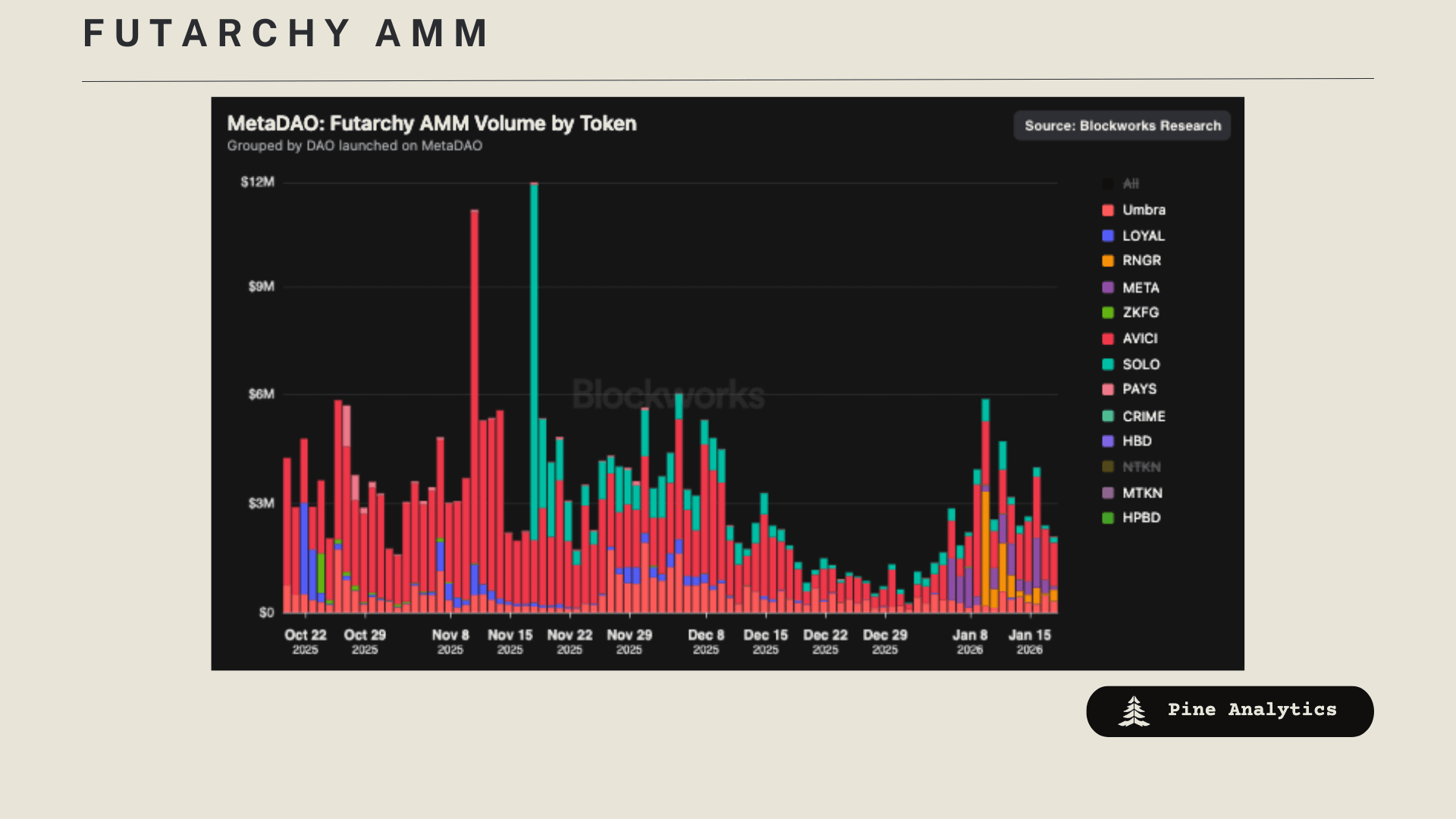

Futarchy AMM

The Futarchy AMM is MetaDAO’s decentralized exchange on Solana, purpose-built to support futarchy-based governance and trading for the ownership coins launched on the platform. At a surface level, it functions like a standard automated market maker, providing spot liquidity for project tokens (e.g., META/USDC). Under the hood, it is tightly integrated with conditional pass/fail prediction markets used for governance, where proposals are evaluated by markets and approved when the price of the pass outcome exceeds the fail outcome by a defined threshold.

A key innovation of the system is liquidity bootstrapping for governance markets. Approximately 50% of the liquidity used in proposal prediction markets is borrowed directly from the project’s spot pool in the Futarchy AMM. This eliminates the need for proposers to fully seed thin decision markets, reduces spam, lowers participation costs, and ensures that governance markets have continuous, meaningful depth for accurate price discovery.

The AMM charges a 0.5% swap fee. Economically, it should not be viewed as a conventional DEX with many independent LPs. Instead, each project launch effectively creates a single, permanent liquidity position owned by MetaDAO. This position is the project’s payment to MetaDAO for providing token launch infrastructure, governance markets, and continuous liquidity. The DAO cannot withdraw the principal, but it earns a perpetual fee stream from trading activity, aligning MetaDAO’s incentives with the success of each token: the more a token trades, the more the DAO earns.

The data shows that the Futarchy AMM plays two distinct roles over a token’s lifecycle. At launch, it is the dominant source of liquidity and the primary venue for price discovery, leading to a sharp initial spike in trading volume. If a token fails to attract sustained interest, both price action and volume quickly decay and activity on the Futarchy AMM dries up.

For successful tokens, however, liquidity migrates to lower-fee DEXs. In this phase, the Futarchy AMM transitions from a primary trading venue into a high-fee, price-anchored reference market. Most volume routed through it is no longer organic flow but arbitrage that occurs when its price diverges from external venues enough to overcome fees and slippage. Consequently, Futarchy AMM volume for mature, successful tokens is driven primarily by price movements and volatility, not by overall spot trading demand. The more violently a token’s price moves across the broader market, the more arbitrage volume is pulled through the Futarchy pool, and the more fee revenue accrues to MetaDAO’s permanent liquidity position.

Observations and Analysis

When looking at these primary components of the MetaDAO ecosystem, there are a few things we note.

First, the ICOs continually have demand and have been oversubscribed each time, showing continued appetite for participation—though this could simply be a result of token performance so far.

On the legal structure side, tokenholders have much stronger rights over the work of the team than nearly all other token setups, where tokenholders typically receive value from the ecosystem at the discretion of the team. However, we note that in our view, the fiduciary duty a team has to tokenholders is generally weaker than it would be for a company set up in their native country and depends on the team’s country’s relationship with the Marshall Islands.

The proposal process seems to be rather seamless, with teams and the market most often agreeing, with the exception of liquidation proposals. It is our view that if the market does not value a company above NAV, then the company being wound down is inherently capital efficient. However, there may need to be more and larger market participants before we can actually deem the market wise in valuing projects below NAV.

MetaDAO’s Financials

Assets

Currently MetaDAO has roughly $17.1M in assets, consisting mostly of stablecoins along with a long tail of LP positions and project tokens on the Solana network.

Cash Flows

MetaDAO has two significant cash flow sources: fees from their Meteora LP positions and fees from the Futarchy AMM.

The Futarchy AMM has generated $16.4K in daily fees on average since launch, which annualizes to approximately $6M per year. The second notable cash flow comes from MetaDAO’s Meteora LP positions, which are deployed alongside the Futarchy AMM positions upon each token launch. These positions have generated the DAO $12.1K per day in fees on average, annualizing to about $4.4M. The third cash flow worth noting is the buywall, which launched with the RNGR token but has only generated the DAO $4K in revenue to date.

Overall, the two major cash flows are generating approximately $10.4M per year at their current rate. These cash flows spike during token launches and during large price appreciations of tokens launched on the platform. For fees to grow, there needs to be either increased trading volume or an increase in the market cap of tokens launched on the platform.

Expenses

The current spending limit for MetaDAO is $240K per month, totaling an annual spending limit of $2.88M. This is not what is actually spent each month, but the maximum the DAO is permitted to spend by tokenholders.

The $META Thesis

Valuation Context

Currently the fully diluted market cap of the META token is $124M. Subtracting MetaDAO’s treasury value of $17M, you get a free cash flow multiple of 10.2x, or 11.9x without subtracting the treasury.

To put this in context, Jupiter’s FDV is trading at about 12.6x its annualized free cash flow, Pump.fun’s FDV is trading at 8.3x its annualized free cash flow, Jito’s FDV is trading at 55.9x its revenue, and Meteora is trading at about 11.7x free cash flow.

Compared to top Solana protocols, META doesn’t stand out as a deep value play—but it is competitively priced relative to the cash flow the protocol generates. To be bullish here, the thesis needs to be a growth thesis rather than a value thesis.

The Growth Case

1. Futarchy is becoming Lindy

With each proposal that passes, this form of governance becomes more normalized and accepted as viable. As the track record lengthens, more teams will consider futarchy as a legitimate governance option.

2. Structural advantages create a token premium

The legal protections afforded to tokenholders through MetaDAO’s structure, combined with the price performance of tokens launched on the platform, make MetaDAO tokens increasingly attractive compared to competitors without equivalent legal structure and treasury protections. This should lead to a growing premium on MetaDAO tokens.

3. Quality founders follow quality structures

As a result of points 1 and 2, serious founders launching tokens will increasingly opt for MetaDAO over other platforms.

4. Timing aligns with market rotation

The memecoin/valueless token meta is circling the drain, but speculative energy in crypto still needs a home—energy that will only intensify if BTC sees another leg up. MetaDAO offers a destination for speculation with actual substance.

5. What’s missing for explosive revenue growth

Two things: more founders launching on the platform, and a speculative environment where people are actively bidding on tokens. We believe founder interest is growing daily, and the launch of permissionless DAOs could be the spark that ignites this.

The Permissionless Unlock

Permissionless DAOs have been hinted at by the team and appear to be on the roadmap. We believe this could be a pivotal catalyst for MetaDAO’s growth.

The problem with permissioned launches is that they’re too telegraphed—there’s no “rough” to find diamonds in, which kills the speculative energy that comes from discovery. Permissionless DAOs reintroduce that treasure-hunting dynamic: people sifting through launches looking for undervalued gems, which is what ignites bidding frenzies.

Beyond the speculative dynamics, permissionless launches massively expand the volume of founders who can access MetaDAO's infrastructure. The current permissioned process inevitably filters out teams—some of whom could have multi-billion dollar outcomes. History shows that the most transformative projects often come from unexpected places, and gatekeeping inherently limits optionality. Permissionless launches remove this bottleneck, allowing any founder with conviction to raise capital and build, while letting the market sort winners from losers rather than relying on upfront curation.

But here’s where MetaDAO’s structure creates a meaningful advantage over something like pump.fun: the conditional treasury mechanism acts as a capital preservation layer.

If investors in a permissionless ICO decide the team can’t deliver on their vision, they can liquidate the treasury and recover capital. This means:

Less capital gets permanently extracted by bad actors or failed projects

That capital recycles back into the ecosystem to fund more DAOs

Investors can speculate more aggressively knowing there’s a floor

The result is speculative energy without pure extraction dynamics. The frenzy feeds on itself—bidding activity attracts attention, attention attracts founders who want access to that capital, more founders means more opportunities for discovery, which sustains the bidding energy.

In essence, permissionless DAOs could unlock the speculative flywheel that MetaDAO needs to achieve escape velocity.

What Valuation Is Reasonable?

If MetaDAO’s permissionless launches can offer founders the ability to run ICOs aligned with tokenholders—with the protection that projects can be liquidated if teams fail to deliver—then the total addressable market expands dramatically beyond what pump.fun currently serves.

Pump.fun’s TAM is memecoin speculation: tokens with no treasury, no accountability, and no expectation of value creation. MetaDAO’s TAM includes any founder who wants to raise capital, build a real project, and offer investors meaningful protections. The pool of founders who would prefer aligned, protected token launches over pure memecoin dynamics is substantially larger.

MetaDAO likely captures less value per dollar of token volume than pump.fun does. But if the TAM is large enough, the smaller capture rate becomes irrelevant. META wouldn’t need to match pump.fun’s economics per token—it would just need to prove that the volume of serious launches can exceed the volume of memecoins. In a scenario where permissionless DAOs gain traction and MetaDAO becomes the default platform for aligned token launches on Solana, META flipping PUMP on a fully diluted basis is not only plausible but arguably the base case if the thesis plays out.

Given META’s current valuation in line with established DeFi tokens, the downside appears limited before the token reaches value territory. If the team continues executing and permissionless launches deliver on their potential, the upside is substantial. At $6, the current risk/reward is very compelling.