The Compression of L1 Value Capture

Thesis

L1 blockchains cannot sustainably capture fees at scale. Every major revenue source they have ever generated, from transaction fees to MEV, has been systematically arbitraged away by the participants they serve. This is not a failure of execution by any individual chain but a structural feature of open, permissionless networks: whenever L1 revenue grows large enough to matter, the other side of that transaction innovates to compress or eliminate it.

Bitcoin, Ethereum, and Solana are among the most successful networks in crypto. Yet despite processing billions in value, all three have followed the same arc: fee revenue spikes, attracts attention, and then gets competed away by L2s, private order flow, MEV-aware routing, or application-layer extraction. This pattern has repeated across every major fee regime, MEV dynamic, and scaling paradigm in crypto’s history, and there is no evidence it is slowing down.

The natural counterargument is that traditional financial exchanges sustain fees indefinitely. They do, but at levels that would destroy every L1 valuation model in crypto. CME charges less than 0.001 basis points on notional value. If crypto fee markets converge on TradFi economics, which they will as the same participants and competitive pressures arrive, the terminal fee rate for blockchains is orders of magnitude below what current token prices imply.

This paper argues that L1 fee compression is permanent and accelerating, examines the specific innovations that have crushed margins at each stage, and considers what this means for L1 token valuations that still price in sustainable fee capture.

Bitcoin

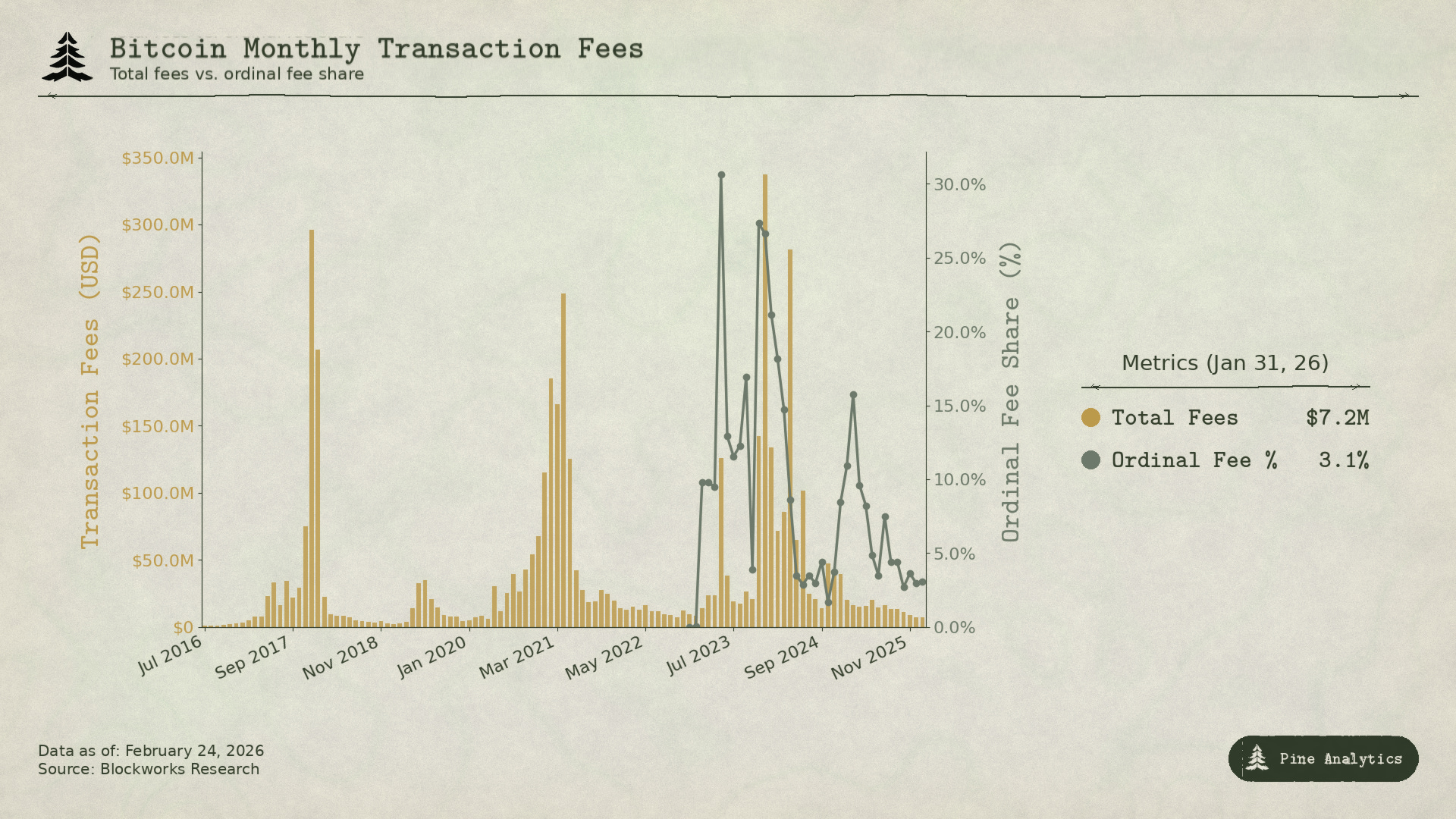

Bitcoin generates fee revenue almost exclusively through congestion driven by demand to send BTC on-chain. With no smart contracts, there is essentially no MEV. The problem: each time BTC price appreciation has driven a fee spike, the spike has been smaller relative to economic activity than the one before it.

In 2017, BTC surged from $4,000 to $20,000, a 5x move. Average fees went from under $0.40 to over $50. At the peak on December 22, fees accounted for 78% of total miner block rewards: roughly 7,268 BTC in fees, nearly four times the block subsidy. Fees collapsed 97% within three months.

The market responded. SegWit adoption rose from 9% of transactions in early 2018 to 36% by mid-year, and those SegWit transactions paid only 16% of total network fees despite representing over a third of volume. Exchanges adopted batching, consolidating hundreds of withdrawals into single transactions. The combined effect cut fees 98% within six months. Lightning Network launched in early 2018. Wrapped BTC on other chains gave users exposure without touching the base layer.

By the 2021 peak, monthly fees were lower than 2017 despite BTC reaching $64,000. Transaction count was lower. Volume transacted was 2.6x higher in USD terms. The network was moving more value but capturing the same or less in fees.

The current cycle made the trend undeniable. BTC appreciated from $25,000 to over $100,000, a 4x move. Fees for standard transfers never spiked like previous cycles. By late 2025, transaction fees had fallen to roughly $300,000 per day, less than 1% of miner income. Bitcoin earned $922 million in total fee revenue for 2024, but the majority came from Ordinals and Runes activity rather than traditional BTC transfers. The spot Bitcoin ETFs accumulated over 1.29 million BTC by mid-2025, roughly 6% of total supply, providing massive demand for BTC exposure that generates zero on-chain fees. The need to interact with Bitcoin’s chain to access the asset has been largely engineered away.

The Ordinals and Runes fee spikes briefly pushed fees to 50% of miner revenue in April 2024, but faded to below 1% by mid-2025 as tooling matured. These resembled MEV more than congestion, driven by immature infrastructure around novel assets rather than demand for BTC settlement.

The pattern: every time Bitcoin’s fee revenue grows large enough to matter, the ecosystem builds cheaper alternatives. The L1 gets one big fee spike from each demand source, then the margin gets innovated away.

Ethereum

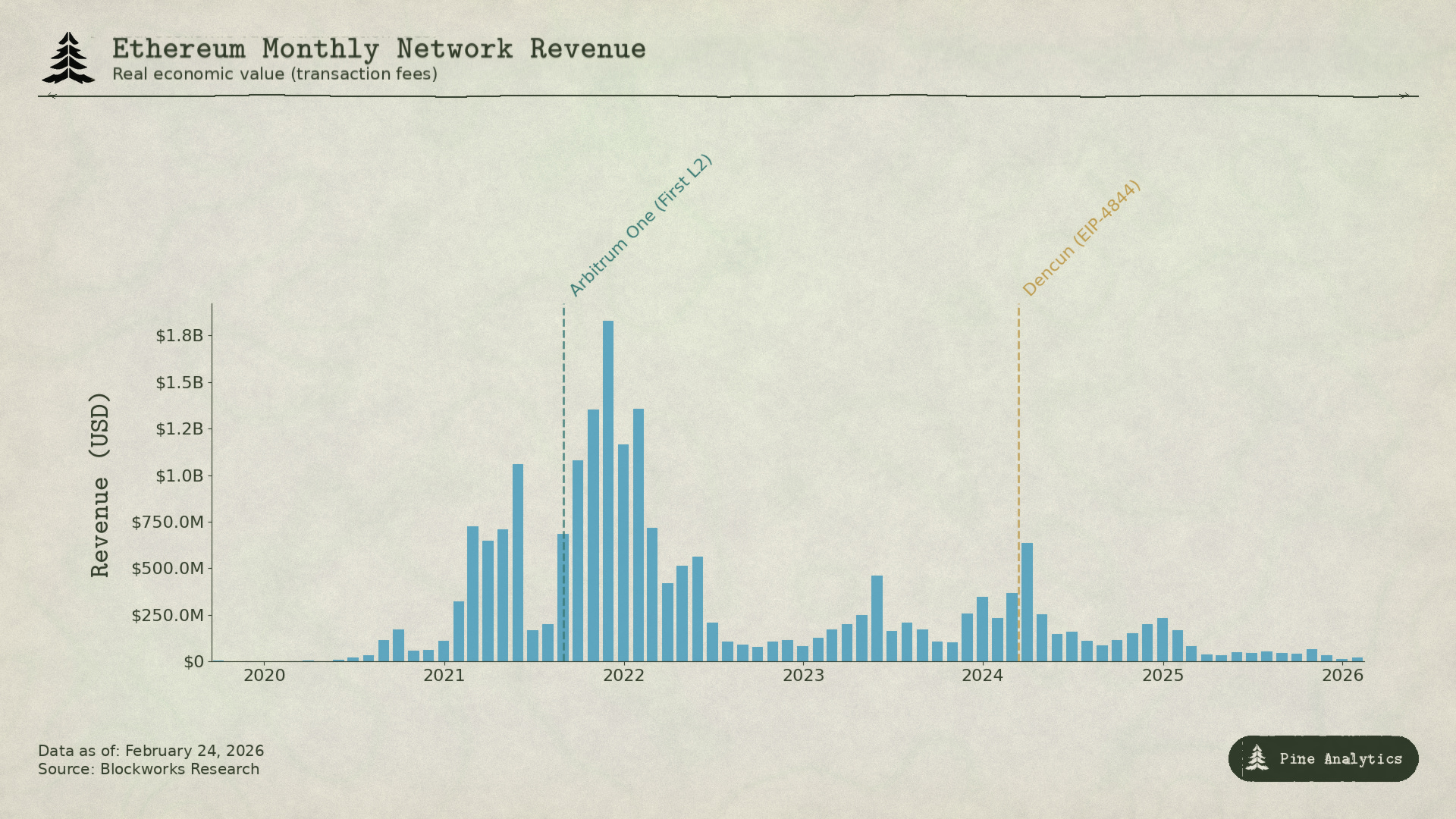

Ethereum’s fee story is more dramatic because the chain actually captured enormous value, then watched it get systematically dismantled.

DeFi Summer in mid-2020 made Ethereum the center of a new financial system. Uniswap’s monthly volume exploded from $169 million in April to $15 billion by September. TVL went from under $1 billion to $15 billion by year end. Ethereum miners earned a record $166 million in fees in September 2020, six times more than Bitcoin miners. For the first time, a smart contract platform was generating serious sustained revenue from genuine economic activity.

Through 2021, NFTs layered on top of DeFi. Average transaction fees hit $53 at peak. Quarterly fee revenue climbed from $231 million in Q4 2020 to $4.3 billion in Q4 2021, a 1,777% increase. EIP-1559 in August 2021 introduced a burned base fee, permanently removing revenue from supply. Ethereum looked like it had solved value capture.

But fees were congestion-based. Users paid $20-$50 not because that was the fair cost of execution, but because demand exceeded the chain’s roughly 15 TPS capacity. This created enormous incentive for cheaper alternatives.

Alt L1s like Solana, Avalanche, and BNB Chain offered execution for pennies. Ethereum L2 rollups like Arbitrum and Optimism absorbed activity, executing on their own chains and posting compressed batches back to Ethereum.

Then Ethereum delivered a self-inflicted wound. The Dencun upgrade on March 13, 2024 introduced blob transactions (EIP-4844), giving L2s a far cheaper way to post data. Before blobs, L2s used calldata at roughly $1,000 per megabyte. After: Arbitrum’s fees dropped from $0.37 to $0.012 per transaction. Optimism fell from $0.32 to $0.009. Median blob fees fell to effectively zero. Ethereum built a dedicated cheap lane for the users it was trying to retain, eliminating one of its last significant fee revenue streams.

The numbers: in 2024, L2s generated $277 million in revenue but paid only $113 million back to Ethereum. By 2025, L2 revenue dropped to $129 million, but the amount paid to Ethereum collapsed to roughly $10 million, less than 10% of L2 revenue, a 90%+ decline year-over-year. Monthly L1 fee revenue that once averaged over $100 million fell below $15 million by Q4 2025. The chain that generated $4.3 billion in a single quarter was on pace for revenues 95% lower just four years later.

Bitcoin’s compression came from users finding off-chain access to the asset. Ethereum’s came in two waves: alt layer siphoned users unwilling to pay congestion pricing, then Ethereum’s own scaling roadmap moved L2 data availability to near-zero pricing, gutting the L1’s ability to monetize the activity settling through it. In both cases, the L1 built or enabled the infrastructure that eroded its revenue.

Solana

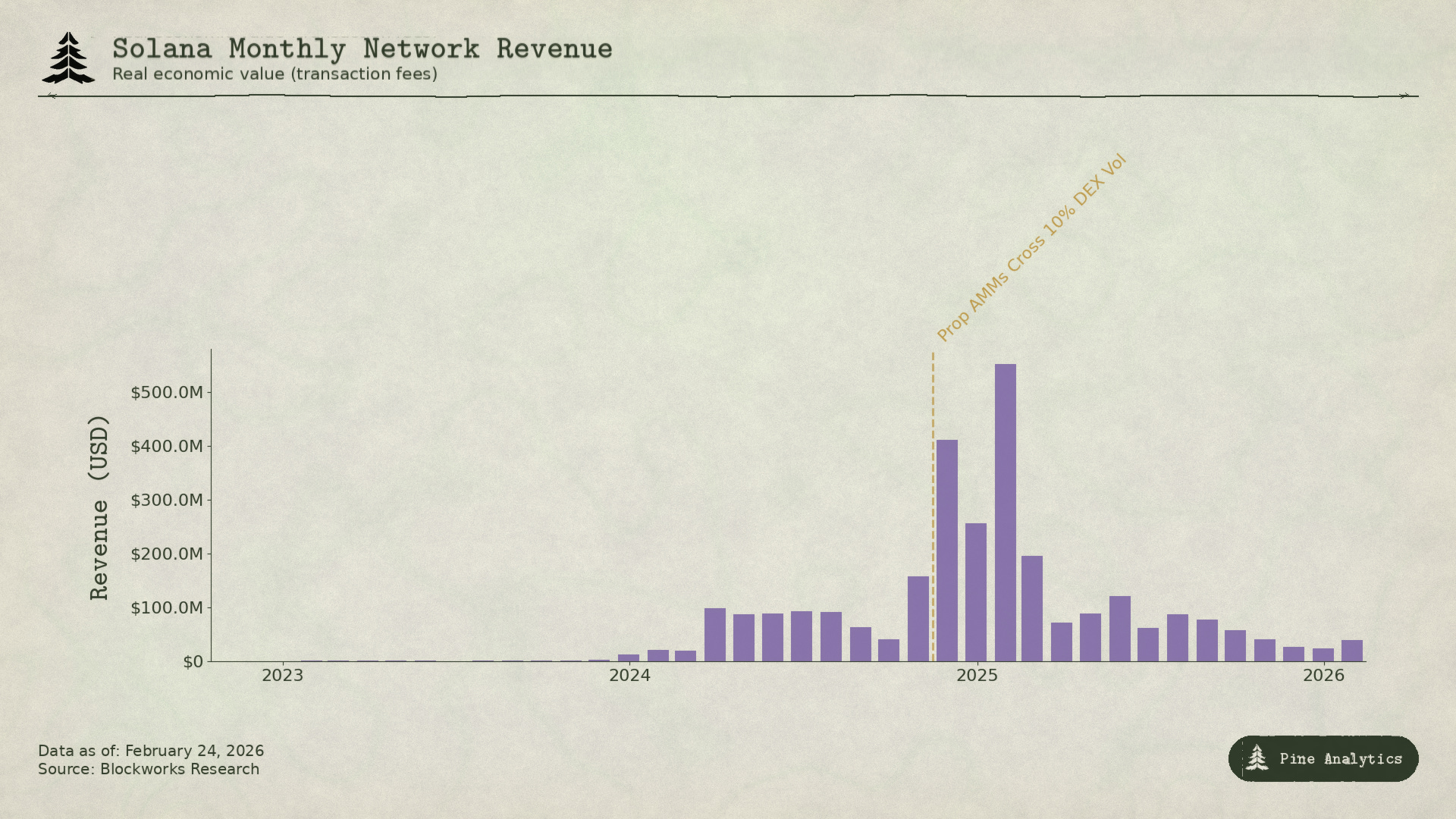

Solana’s value capture is fundamentally different because nearly none of it comes from congestion fees. The base fee is a fixed 0.000005 SOL per signature, essentially zero. Instead, roughly 95% of fee revenue comes from priority fees and MEV tips paid through Jito’s block engine. In Q1 2025, Solana’s Real Economic Value reached $816 million, with 55% from MEV tips. Validators were on pace to earn $1.2 billion in 2024 against only $70 million in costs.

The catalyst was memecoin trading. Pump.fun launched in January 2024, generated over $600 million in protocol revenue in under 18 months, and was responsible for up to 99% of memecoin launches at peak. DEX volumes hit $38 billion daily at peak. The TRUMP token launch in January 2025 pushed priority fees to 122,000 SOL in a single day and MEV tips to 98,120 SOL. The top 1% of memecoin traders generated $1.358 billion in fees in 2024, nearly 80% of total memecoin fees. Almost all MEV-driven.

Two innovations are now compressing this revenue.

First: proprietary AMMs. Protocols like HumidiFi, SolFi, Tessera, ZeroFi, and GoonFi use private vaults managed by professional market makers who quote prices internally and update them many times per second. Because liquidity is invisible to public pools, MEV bots cannot sandwich trades. Critically, prop AMMs select counterparties by accepting offers routed through aggregators like Jupiter rather than passively sitting in public pools where anyone can pick off stale quotes by paying MEV tips. By keeping pricing private and continuously refreshed, they eliminate the stale order problem that generates much of Solana’s MEV revenue. HumidiFi alone processed nearly $100 billion in cumulative volume in its first five months. Prop AMMs now account for over 50% of Solana’s DEX volume, even higher for liquid pairs like SOL/USDC.

Second: Hyperliquid pulling the most valuable spot trading off Solana entirely. Through HyperCore, Hyperliquid built native bridge infrastructure allowing Solana-originated tokens to be deposited, withdrawn, and traded on its spot order book. When Pump.fun launched its PUMP token in July 2025, spot price discovery occurred on Hyperliquid rather than Solana DEXs, bridged through HyperCore. Hyperliquid had already demonstrated this with SOL itself and tokens like FARTCOIN. The initial price discovery phase, where spreads are widest, volatility highest, and MEV most extractable, is migrating off Solana.

These forces attack from opposite directions. Prop AMMs compress MEV on trades staying on Solana. Hyperliquid pulls the most MEV-rich spot activity off entirely. By Q2 2025, Solana’s REV had fallen 54% quarter-over-quarter to $272 million. Daily MEV tips declined over 90% from January’s peak to below 10,000 SOL per day.

Same pattern, different mechanism. Solana’s fee revenue was about MEV extracted during the chaotic early phase of a new trading meta. As prop AMMs clean up execution and Hyperliquid absorbs extractable order flow, the margin compresses. The L1 captured enormous value during the frenzy, but the market is already building tools to ensure it cannot sustain that extraction.

Implications for Token Prices

The pattern documented across all three chains is not merely descriptive. It is predictive. Every L1 fee regime follows the same arc: novel demand creates a spike, the spike attracts innovation that compresses it, and the compression is permanent. Applying this framework forward generates specific expectations for four tokens.

Ethereum: Continued Catabolic Fee Compression

Ethereum's fee trajectory has no obvious floor. L2s paid Ethereum $113 million in 2024, collapsing to roughly $10 million in 2025, a 90%+ decline. Every new L2 further fragments demand for Ethereum block space while the protocol's own roadmap continues cheapening data availability. EIP-4844 was not a one-time repricing but the beginning of a structural shift in which Ethereum deliberately subsidizes the infrastructure that routes activity away from its fee market. Monthly L1 fee revenue has fallen below $15 million, and the forces driving that decline are accelerating. Unless Ethereum discovers an entirely new source of L1 demand, the token price will reflect continued compression. ETH has already begun trading like a low-yield infrastructure token rather than a high-growth smart contract platform.

Solana: New ATH in Activity, Not in Price

Solana will almost certainly mark a new all-time high in on-chain activity next cycle. The ecosystem is deep, developer momentum is strong, and infrastructure is more robust than ever. But fees will not follow. The memecoin frenzy of late 2024 and early 2025 was Solana's SegWit moment: one big fee spike from a novel demand source, followed by rapid innovation that compresses the margin. Prop AMMs handle over 50% of DEX volume, eliminating most MEV. Hyperliquid's HyperCore is pulling the highest-margin price discovery off-chain. Even at 2-3x the activity of January 2025, fee infrastructure has matured past the point where that activity translates into comparable validator revenue. Daily MEV tips fell 90%+ from peak despite healthy activity. Without fee revenue to justify a higher valuation, it is unlikely SOL surpasses its all-time high price next cycle, even if usage does.

Hyperliquid: The Boom and the Compression

Hyperliquid is the most interesting case because it represents the next iteration of the same cycle, and the market has not yet priced in the back half.

Hyperliquid is already the dominant perpetuals DEX for TradFi assets. During the recent silver volatility spike, HIP-3 deployed markets captured approximately 2% of global silver trading volume, with tighter median spreads than COMEX for retail-sized trades. At points TradFi instruments accounted for roughly 30% of platform volume, with daily notional exceeding $5 billion. The platform generated approximately $600 million in revenue in 2025, with 97% flowing to HYPE buybacks and burns.

We expect Hyperliquid to continue dominating perps DEX volume for TradFi assets. The product-market fit is clear: 24/7 trading on commodities and equities unavailable outside business hours on traditional venues, permissionless market deployment through HIP-3, and leverage up to 20x on assets where CME requires 18% initial margin. Going into the next bull cycle, continued growth in activity and fees could drive a repricing of HYPE at the scale of Solana's repricing from its bear market lows. If TradFi asset volume continues to grow, a similar trajectory for HYPE is likely. Investors will likely extrapolate a single quarter of massive TradFi perps revenue into a forward valuation.

But Hyperliquid’s fee model contains the seeds of its own compression. The platform charges base taker fees of 4.5 basis points on notional value, with volume and staking discounts up to 40%. This is fundamentally different from TradFi derivatives pricing. On the CME, exchange fees for an E-mini S&P 500 contract are roughly $1.33 per side regardless of the contract’s $275,000+ notional value, less than 0.001 basis points. For a $10 million notional position: roughly $2.50 on CME versus $4,500 on Hyperliquid. The gap is approximately 1,800x.

This gap survives because Hyperliquid’s user base is predominantly retail and crypto-native. But TradFi perps bring TradFi expectations. As volume grows and institutional participants arrive, pressure to match CME-style economics will intensify. Hyperliquid’s own fee schedule reveals the trajectory: HIP-3 growth mode slashes taker fees by over 90% for new markets, to as low as 0.0045%. Top-tier traders can get below 0.0015%. The protocol is already racing its own fee compression. Competing perps DEXs and eventual traditional venues offering on-chain products will accelerate this. The endgame: Hyperliquid either loses volume to cheaper competitors or reprices fees toward fixed-fee models. Either outcome means the revenue base investors extrapolated will not materialize at scale, and the token will reprice downward rapidly.

Bitcoin: Price Must Lead Fees

Bitcoin occupies a unique position among these four because the relationship between fees and token price runs in the opposite direction. For Ethereum, Solana, and Hyperliquid, the logic is: fees generate revenue, revenue justifies token valuation, fee compression therefore compresses token price. For Bitcoin, the logic is inverted. Miners need the token price to appreciate at a strong enough rate to keep mining profitable through successive halvings, because fee revenue has proven unable to fill the gap left by declining block subsidies.

The 2024 halving reduced block rewards from 6.25 BTC to 3.125 BTC, cutting daily issuance from 900 BTC to 450 BTC. By late 2025, transaction fees had fallen to roughly $300,000 per day, less than 1% of total miner income. Despite Bitcoin earning $922 million in total fee revenue in 2024, the majority of that came from the Ordinals and Runes spike, not from sustainable organic fee demand. With fees contributing almost nothing, miners are almost entirely dependent on the block subsidy, which halves every four years, denominated in BTC. The only way miners stay profitable through each halving is if Bitcoin’s dollar price roughly doubles on the same timeframe, offsetting the 50% reduction in BTC-denominated revenue. Historically this has happened. But it is a precarious foundation. The chain’s security budget is not funded by usage. It is funded by continuous price appreciation of the asset itself. If Bitcoin’s price ever stagnates through a halving cycle, mining becomes unprofitable, hash rate drops, and the network’s security degrades, creating a potential negative feedback loop.

This makes Bitcoin’s sustainability story fundamentally more fragile than it appears. Price can lead fees in a way that no other chain can replicate, because Bitcoin functions primarily as a monetary asset rather than a smart contract platform. People buy BTC for the asset, not for the blockspace. This gives Bitcoin a mechanism the other three chains lack: price appreciation driven by monetary demand can fund chain security even when fee revenue is negligible. But it also means Bitcoin’s long-term security is entirely contingent on an assumption, continued price appreciation, that cannot be guaranteed. The chain’s viability as a secure settlement layer depends not on building useful applications that generate fees, but on maintaining a narrative and market structure that drives perpetual demand growth for the asset. It has worked so far. Whether it works through the next three or four halvings, as block subsidies shrink from 3.125 to 1.5625 to 0.78125 BTC, is the most important open question in crypto.

Fantastic breakdown and analysis, also appreciated how articulate and easy to follow this was!