The FairScale Saga: A Case Study in Early-Stage Futarchy

What is FairScale?

FairScale (@fairscalexyz) is reputation infrastructure built on Solana. It provides APIs that score users and wallets by analyzing on-chain activity, social behavior, and sybil patterns to generate a composable FairScore. Protocols, AI agents, and dApps can use these scores to gate access, filter participants, and assess trust.

What happened

The Launch

FairScale launched its $FAIR token and ran a fundraising round via @stardotfun (a Solana launch platform often used for fair/ICO-style raises) on January 23rd. The raise attracted approximately $355,600 from 219 participants. The team accepted $300,000 and refunded the excess. During the launch, the team opted their token into futarchy governance via @combinatortrade.

The Price Collapse

The $FAIR token went live at a 640K FDV and within three days crashed to roughly 220K FDV. Over the following three weeks, the token dropped to a low of 140K FDV. The decline coincided with SOL falling from $127 to $88, a dramatic market-wide drawdown that shook confidence across the ecosystem. But the sell-off was not purely macro-driven. Growing community concerns about the accuracy of the team’s revenue projections and partnership claims added selling pressure on top of the broader downturn. The combination of a bad market and perceived misrepresentation created a situation where contributors who had allocated more than they felt comfortable holding saw little reason to stay.

The Liquidation Proposal

After this prolonged downtrend, a large holder of the $FAIR token submitted a proposal to liquidate the project’s liquidity and execute token buybacks. This would be immediately profitable for token holders because the unlocked market cap had fallen dramatically below treasury value. The proposal was accompanied by a detailed document alleging team misconduct and revenue misrepresentation, which we examine in the following section. The proposal passed by very thin margins, authorizing the liquidation of 100% of the team’s treasury. The result was a roughly 300% price increase from the bottom to the price implied by the treasury value, delivering large immediate profits to the proposing holder.

The Fraud Allegations and the Team’s Response

The liquidation proposal was accompanied by a detailed document accusing the FairScale team of systematic misrepresentation of partnerships and revenue.

FairScale had publicly cited specific MRR figures tied to named partners: approximately 17K euros from TigerPay, $5K from Streamflow, and $500 each from PotBot and PNP. The Streamflow figure came with a granular breakdown including a $1,000 monthly baseline, $0.10 per wallet scoring, and a 40,000 wallet monthly volume estimate. The team projected $10K MRR by end of February and $20K MRR by end of March.

When community members contacted the partners directly, every single one described their arrangement as a mutual benefit integration with no payment structure. The Streamflow breakdown, which specified pricing for a partnership with no payment terms, was described by the team as an “internal error.” Additional concerns emerged around TigerPay, their claimed largest revenue driver, which showed no app updates since August 2024, minimal user activity, and overwhelmingly negative reviews. A pre-ICO announcement of a $1.5M preseed raise led by “BNG Capital” also drew scrutiny, as the entity appeared to have been created months prior with no verifiable presence. The team’s previous project, PRNT, surfaced similar community complaints of unfulfilled promises.

The FairScale team pushed back. They maintained that the only formal revenue target was $1.5M ARR by end of 2026, that they were three weeks into operations, and that first paid API revenue had been generated. Every named partner had publicly confirmed their relationship on X. The team framed the proposal as a single large holder using futarchy mechanics to exit at the highest possible price during a downturn, with FDV at $348K against a $215K liquid treasury. They pointed to their shipping pace as evidence of legitimacy: scoring engine rebuild, x402 micropayments, sybil detection, and 50+ developers on their APIs.

From our review, the partner confirmations verify that integrations exist but do not address the specific MRR figures cited before the ICO. The gap between “we have partnerships” and “we projected 17K euros monthly from TigerPay” remains unexplained. The team’s shipping velocity is real, but shipping product and overstating commercial traction are not mutually exclusive. The truth likely sits in an uncomfortable middle ground: a team that was genuinely building but significantly overstated how far along the business actually was.

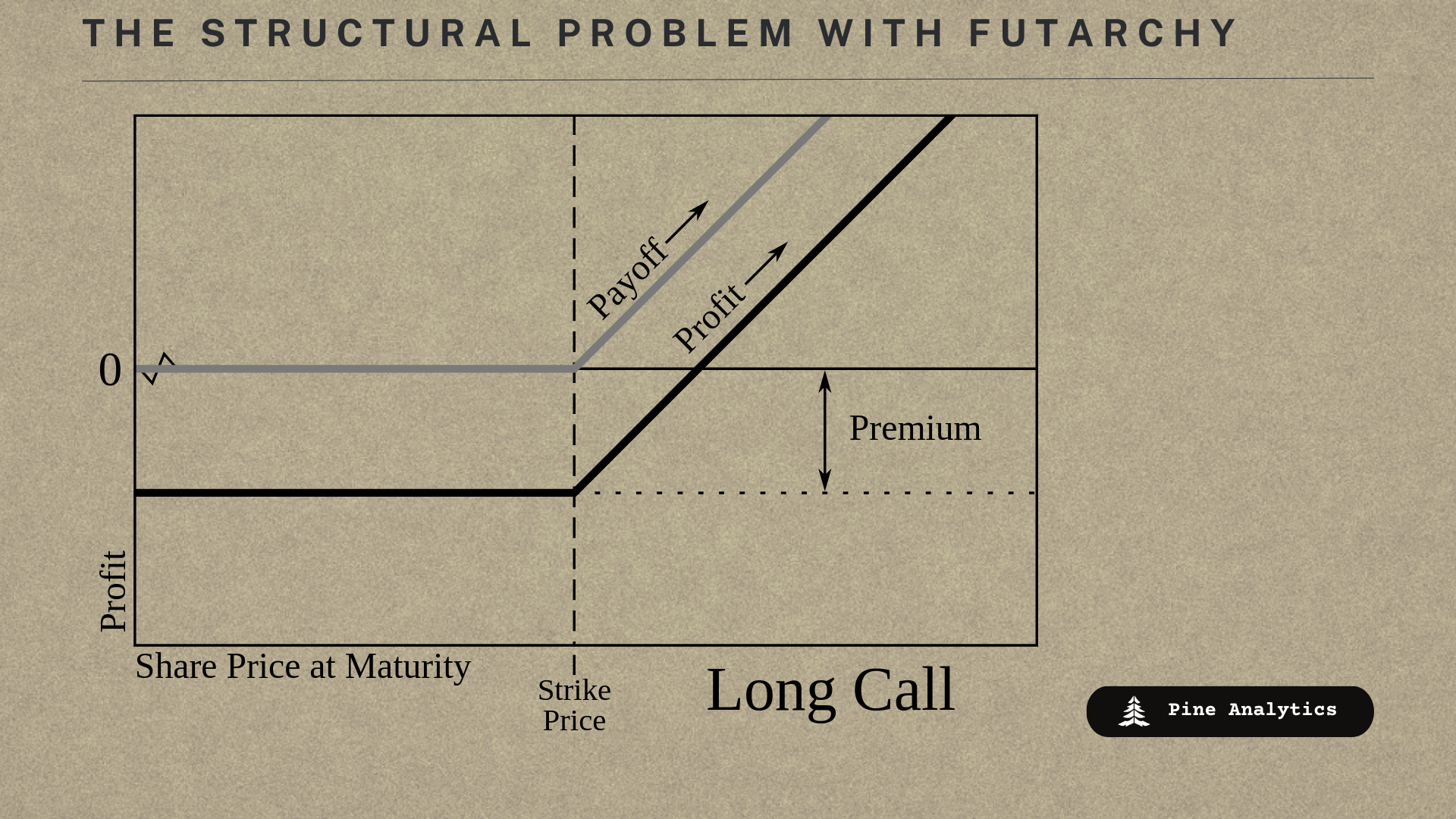

The Structural Problem with Futarchy

The FairScale case exposes a fundamental tension in futarchy’s design that simple mechanical fixes cannot resolve.

The first layer of the problem is straightforward. Contributors to futarchy raises implicitly view their participation as coming with free downside protection below NAV. If the token drops below treasury value, they can vote to liquidate and recover their capital. This makes contributing feel closer to a risk-free bet than a genuine investment, which means founders overraise from a contributor base that is short-term oriented and has no reason to hold through volatility. When a drawdown hits, they exercise their implicit put option and kill the business.

This dynamic is compounded by external capital. When a token trades at any significant discount to NAV, liquidation proposals create a risk-free arbitrage opportunity. There is effectively no limit to the capital that would find it profitable to bid for liquidation, meaning the people who want to keep the project alive cannot outbid the arb unless they push the token above NAV.

The obvious solutions, time locks before liquidation proposals, sustained trading below NAV requirements, all share the same logic: give founders breathing room to execute. But FairScale reveals why these are insufficient on their own.

Consider @ranger_finance, where a quarter of their treasury was used for buybacks just days after their @MetaDAOProject ICO. The token dropped below NAV not because of any issues with the team, but because fair-weather depositors (including ourselves) who had entered with implicit downside protection exited when the price failed to appreciate. A time-lock before liquidation would have protected them, and arguably should have. FairScale is a different case entirely. The liquidation was accompanied by documented evidence of revenue fabrication and partnership misrepresentation. A time-lock before liquidation would have shielded a team that appears to have materially misled its contributors. The mechanism that protects Ranger also protects FairScale, and those two outcomes point in opposite directions.

This is the core design tension: futarchy cannot easily distinguish between a token below NAV because the market dipped and a token below NAV because of problems with the business.

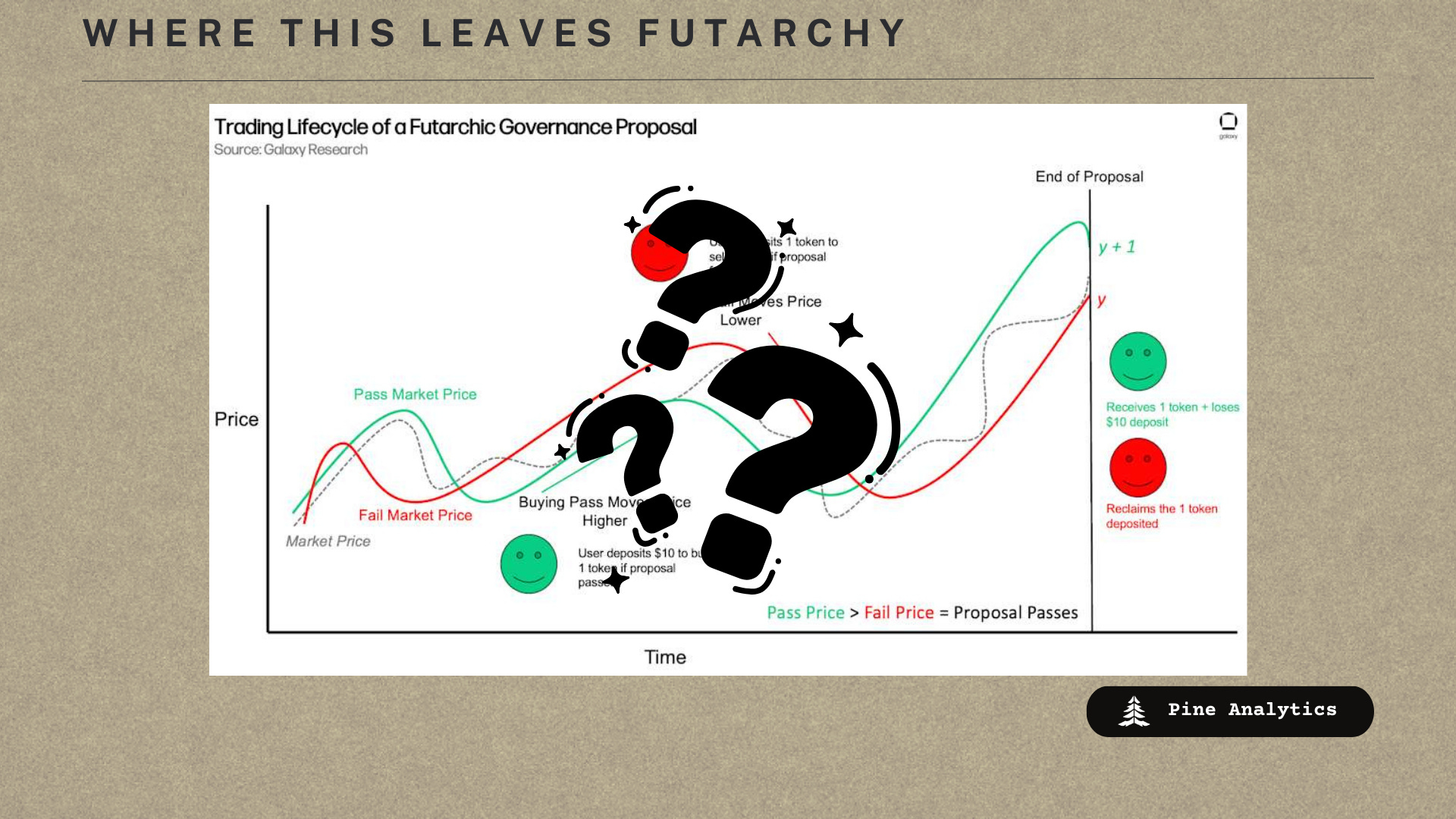

Where This Leaves Futarchy

The FairScale saga suggests that futarchy’s next evolution needs more than mechanical parameter tweaks. It needs layers that can differentiate between market-driven drawdowns and business-driven drawdowns. A few directions worth exploring:

Conditional protections tied to verifiable milestones could offer founders breathing room that is earned rather than automatic. If a team can demonstrate on-chain delivery against stated goals, they receive extended protection from liquidation. If they cannot, the protection does not apply.

Community-driven dispute resolution, where liquidation proposals that include fraud allegations trigger a structured review period before a vote, could provide space for evidence to be evaluated rather than having everything collapse into a binary price signal.

Neither of these are complete solutions, and both introduce their own tradeoffs. Critically, both require offchain mechanisms to function. Milestone verification needs someone to judge whether a milestone was met. Dispute resolution needs someone to evaluate evidence of fraud. These are inherently subjective, human processes that introduce trust assumptions into a system whose appeal was supposed to be trustlessness. Taken far enough, this logic converges on something resembling the existing legal system: judges, evidence standards, dispute timelines, enforcement.

There is a counterargument that even simple concrete limitations on liquidation, such as time locks, could have a positive second-order effect regardless of their direct mechanical impact. If contributors know they cannot simply liquidate at NAV the moment a token dips, they are forced to do more due diligence before investing. The implicit put option disappearing means capital has real downside, which naturally dissuades fair-weather investors and reduces inflows into less credible projects. The filtering happens before the raise rather than after, which is where it should happen.

Perhaps the most elegant expression of this logic comes from @barrett_io, who suggested whitelisted ICOs. Rather than changing the futarchy mechanism itself, this approach shifts the problem upstream to contributor selection. If a team can fill their raise with whitelisted participants who believe in the product and have long time horizons, then liquidation during a bad market becomes far less likely because the stakeholder base is built to weather volatility. If the team cannot fill the raise with whitelisted participants, they still get whatever capital they can attract, but they do so with eyes open about the type of stakeholder base they are working with. This is compelling because it requires no mechanical changes to futarchy. It simply proposes that teams get the quality of investor they can attract, and lets that quality determine how resilient the project is to drawdowns.

Futarchy in its current form works well as a price discovery mechanism but poorly as a governance mechanism for early-stage businesses. The implicit put option below NAV distorts contributor incentives, attracts the wrong capital, and creates a playbook for extraction. Whether through mechanism changes, contributor filtering, or simply removing the implicit safety net and forcing real due diligence, the path forward involves making futarchy raises feel less like risk-free bets and more like genuine investments.