Tokenized Equities on Solana

Structures, Holder Rights, and On‑Chain Pricing

Executive Summary

Solana has effectively won the market for tokenized equities, capturing roughly 97% of all tokenized‑equity spot trading volume in May 2026 (~$869M on Solana vs. ~$24M across every other chain combined). But the four issuers that define the landscape — Backpack Securities (SPCX), Ondo Global Markets, xStocks (Backed Finance), and PreStocks — are not the same product wearing different logos. They look identical on a price chart and are radically different legal instruments underneath, sitting on a spectrum from redeemable into the real security to purely synthetic private‑market exposure. The distinction is invisible until something breaks — and in May 2026, with PreStocks, something did.

What a holder actually owns, ranked best to weakest:

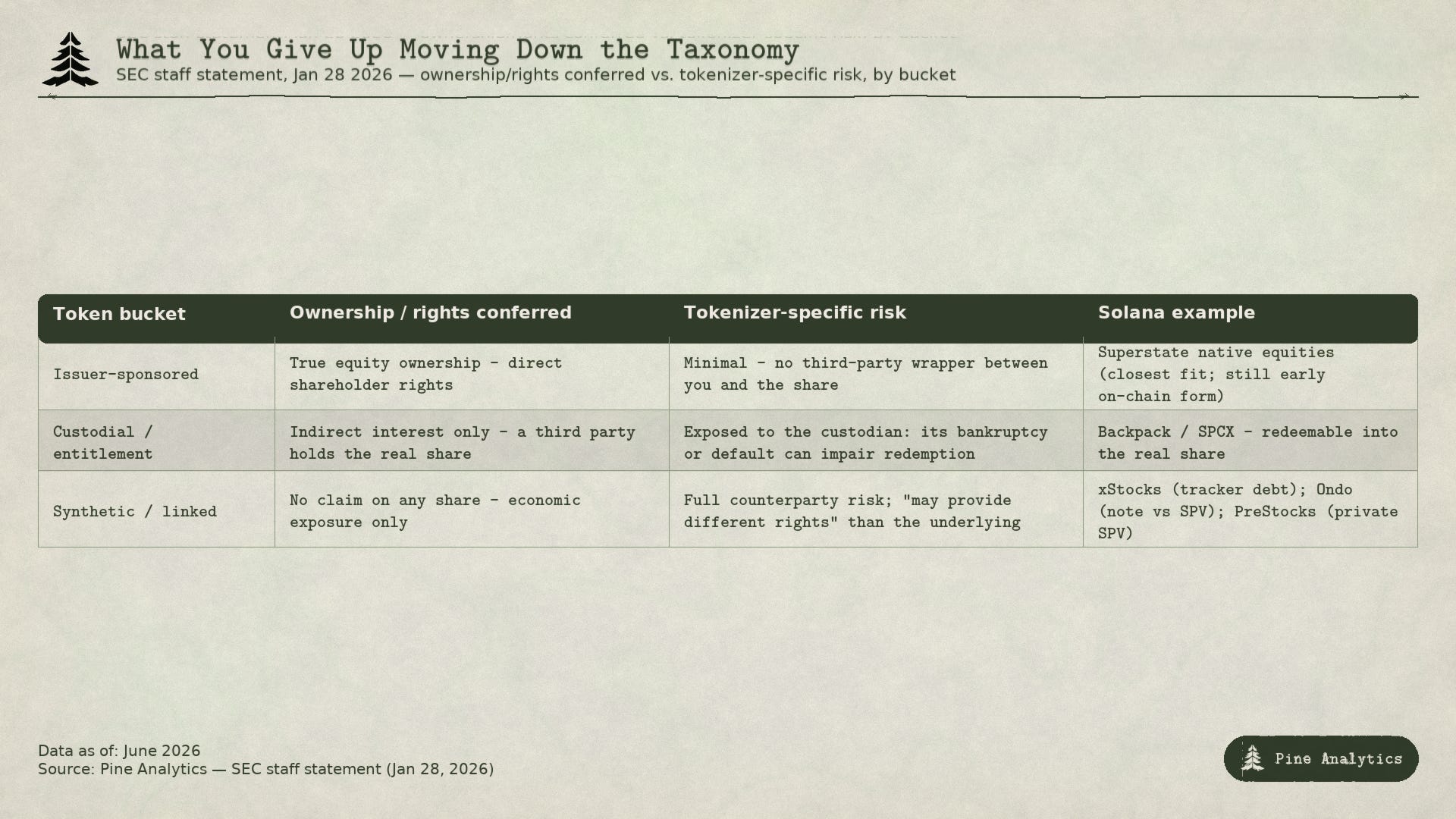

Backpack / SPCX — closest to owning the real thing. The token is redeemable back into the underlying share via ACATS/DTCC rails for eligible holders, landing on a UCC Article 8 security entitlement with genuine ownership rights. The catch: redemption is gated to onboarded holders; the raw on‑chain token is still an SPV claim.

Ondo Global Markets — the best‑protected non‑redeemable model. A structured note against a bankruptcy‑remote SPV, 1:1 + buffer collateral, a third‑party security agent with a first‑priority interest, and daily verification — but explicitly no shareholder rights.

xStocks — the most DeFi‑native option (Raydium, Jupiter, Kamino), but a bearer‑debt tracker certificate with no shareholder rights, and — contrary to common marketing — collateral that “may not always consist of the underlying shares.” Holders carry Backed’s credit risk.

PreStocks — the weakest posture: synthetic exposure to pre‑IPO SPVs with no rights and disputed backing. In May 2026, Anthropic and OpenAI called the underlying share transfers void/invalid and the tokens fell 34–40%; PreStocks showed an implied ~$1.3T Anthropic valuation against only ~$23M in actual assets, and the attestation reports promised at launch were never published.

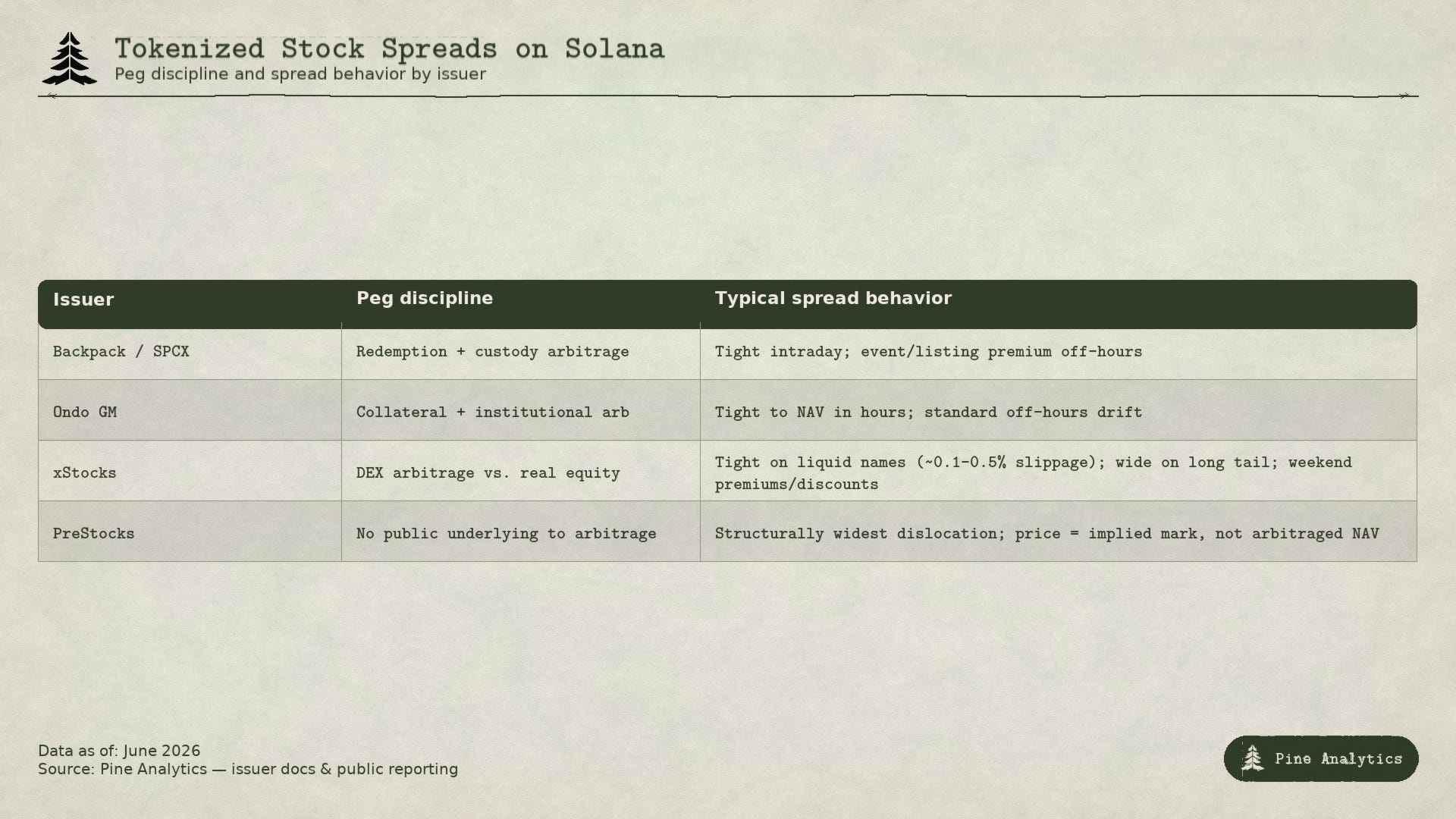

The decisive variable for on‑chain pricing is arbitrage: a tokenized stock carries two prices — the 24/7 on‑chain price and the underlying share value set by a market that closes nights and weekends — and when a live underlying market exists to arbitrage against (xStocks, Ondo, and Backpack during US hours), pegs hold tight and typical swap slippage tolerance on liquid names is just ~0.1–0.5%, whereas off‑hours, on weekends, or for PreStocks where there is no public underlying at all, premiums and discounts open up and prices can dislocate violently; liquidity is also heavily concentrated in a few marquee tickers (TSLAx, NVDAx, CRCLx, SPCX), so the 100‑plus long‑tail names quote wide and slip hard on any real size. The bottom line is that Solana has won the venue and the open question is which structure wins the holder — and regulation is already tilting the answer, with the January 2026 SEC staff statement’s practical effect being to pressure purely synthetic models and favor issuer‑sponsored and redeemable‑custodial ones, so for anyone choosing among these tokens it is the legal wrapper, not the ticker, that determines what you’re actually holding.

Background

A tokenized stock is a crypto asset whose ownership is recorded on a blockchain and whose value references an equity. The SEC staff statement of January 28, 2026 (Divisions of Corporation Finance, Trading and Markets, and Investment Management) established the governing taxonomy. It distinguishes:

Issuer‑sponsored tokens — can represent true equity ownership.

Custodial / entitlement tokens — a third party holds the real share and issues a token evidencing an indirect interest.

Synthetic / linked tokens — economic exposure only, no claim on a share.

The statement’s key warning: third‑party tokenized securities “may provide different rights” than the underlying, and holders may face risks specific to the tokenizer (e.g., its bankruptcy) that a direct shareholder would not. This is the lens for everything below.

The Four Offerings

Backpack Securities — SPCX

Issuer & mechanics. SPCX is issued by Backpack Securities, a regulated US broker‑dealer, and launched on Solana June 11–12, 2026 to coincide with SpaceX’s Nasdaq IPO — reportedly the first time a newly listed equity had a simultaneous on‑chain market. Each token is backed 1:1 by a real SpaceX share purchased and held in regulated custody. Liquidity is routed by Sunrise DeFi.

Legal structure & holder rights. Backpack’s structure is the strongest for holders because the token is redeemable back into the underlying equity. Eligible (onboarded, KYC’d) holders can redeem tokens for the real share and transfer it to any traditional brokerage via ACATS/DTCC settlement rails — the same infrastructure that moves stock between Schwab and Fidelity. On the brokerage side this is a UCC Article 8 security entitlement with real ownership rights (dividends, corporate actions, transfers). Caveat: the raw on‑chain token is still, in Backpack’s own description, a “tokenized claim / claim on an SPV.” Redemption into the real share is gated to eligible holders — a random secondary‑market buyer who never onboards is closer to the note holders below.

On‑chain market data — spread & value. SPCX surpassed $100M in 24‑hour volume by June 15, 2026, accounting for roughly 40% of all Solana tokenized‑equity trading in its first days. The underlying SpaceX equity priced at $135 (IPO), closed day one at $160.95 (+19%), and hit an intraday high of $225.64 on June 16. Because SpaceX was newly listed and volatile, the tokenized form carried a meaningful new‑listing / crypto‑access premium: tokenized variants (e.g., BitMart’s bSPCX ~145 USDT, third‑party SPCXON) deviated from the Nasdaq price, especially during after‑hours and crypto‑only sessions when no live equity market exists to arbitrage against.

Risks. Concentration (a single name so far), redemption gated to eligible holders, and the standard custody/operational risk of the broker‑dealer.

Ondo Global Markets

Issuer & mechanics. An Ondo tokenized stock is a structured note — a debt instrument issued by Ondo Global Markets (BVI) Limited, a bankruptcy‑remote SPV. Launched January 2026, Ondo now lists 264 tokenized equities and ETFs and reports >$1B in total value locked — the most extensive equity/ETF roster of the four. Tokenholder rights are governed by Swiss law.

Legal structure & holder rights. This is the best‑protected non‑redeemable model. Tokens are backed 1:1 plus a buffer by underlying securities held at regulated custodial broker‑dealers; Ankura Trust Company acts as Verification and Security Agent, holding a first‑priority perfected security interest in the collateral, with daily verification, monthly reconciliations, segregated accounts, an independent director, and annual audits. But the rights gap is explicit and quoted verbatim from Ondo’s legal docs: “you will not see your name on the share register” and “you do not have shareholder voting rights, shareholder information rights or other shareholder rights.” A Broadridge integration lets holders express voting preferences Ondo may apply — a governance‑experience feature, not ownership.

On‑chain market data — spread & value. Ondo led the tokenized‑stock market by value — roughly ~58–60% of the tokenized‑stock market on RWA.xyz in early–mid 2026 — with ~264 listed assets and >$1B TVL. Because Ondo’s model is collateral‑backed and institutionally arbitraged, on‑chain prices track underlying NAV closely during US market hours; deviations appear off‑hours like all the others.

Risks. Holder owns a note claim against an SPV, not a share — no shareholder rights; exposure to issuer/custodian operational failure (mitigated, not eliminated, by the security‑agent structure).

xStocks (Backed Finance)

Issuer & mechanics. xStocks are SPL tokens on Solana issued by Backed Assets (JE) Limited (Jersey), launched June 30, 2025. The lineup spans 130+ equities and ETFs — AAPLx, TSLAx, NVDAx, METAx, GOOGLx, COINx, CRCLx, MSTRx, plus SPYx and QQQx. Each is structured as a bearer debt instrument classified as a tracker certificate. xStocks is the most DeFi‑native option: Raydium is the primary AMM, Jupiter aggregates quotes, and Kamino accepts xStock collateral for borrowing.

Legal structure & holder rights. Economic exposure only — no shareholder voting, no direct dividend rights (dividends passed via a rebasing mechanism), no legal claim to the underlying shares or to residual assets in a company liquidation. Important correction to common marketing: xStocks is often described as “fully 1:1 collateralized in the underlying shares,” but xStocks’ product disclosures (surfaced in Kraken’s and Bybit’s risk pages) state collateral “may not always consist of the underlying shares” and “other eligible assets (including cash collateral) may be used as substitute collateral.” Holders bear Backed’s credit and solvency risk irrespective of the underlying’s performance.

On‑chain market data — spread & value. xStocks reached ~$293.5M AUM on Solana by mid‑May 2026, with >$3B cumulative on‑chain volume and >$517M DEX volume by early 2026. Liquidity concentrates in a few names (TSLAx, NVDAx, CRCLx); on those, recommended swap slippage tolerance is ~0.1–0.5% on Raydium/Jupiter. Spread mechanism: during US market hours, arbitrage between the on‑chain pool and the real equity keeps the peg tight; long‑tail tickers have thin books and wide spreads / high slippage for size; on weekends and after‑hours, with TradFi closed, prices float on pure crypto supply‑demand and premiums/discounts open up.

Risks. Issuer credit risk, substitute‑collateral risk, thin long‑tail liquidity, and no shareholder standing.

PreStocks

Issuer & mechanics. PreStocks tracks pre‑IPO private companies (e.g., OpenAI, Anthropic, SpaceX pre‑listing) via tokens backed by SPV exposure to private equity. Public volume figures are thin and unreconciled: the highest datable third-party daily volume is ~$29M (April 2026), while platform-cited figures (a $54.43M daily ATH, >$750M cumulative) remain unconfirmed by any third party. Operated under Regulation S — not available to US persons (and several other jurisdictions).

Legal structure & holder rights. The weakest holder posture. Tokens grant economic exposure only — no ownership, voting, dividend, or information rights. The claim depends entirely on the enforceability of upstream SPV interests in private companies with strict transfer restrictions. PreStocks itself disclaims being a broker‑dealer, adviser, exchange, transfer agent, custodian, or VASP.

On‑chain market data — spread & value. This is the most dislocated of the four because there is no public underlying market to arbitrage against — the “price” is a platform/implied mark, not an arbitraged NAV. The structural fragility became concrete in May 2026, when Anthropic and OpenAI publicly stated that the pre‑IPO SPV share transfers underlying these tokens were void/unauthorized (Anthropic: transfers to an SPV are “void under our transfer restrictions”), and the affected tokens fell 34–40% (Anthropic −34% over 7 days, OpenAI −39%; roughly −40% intraday). Compounding this, the platform showed an implied Anthropic valuation above $1.3T against only ~$23M in total assets, and no third‑party attestation reports promised at launch have been published. Spreads/discounts here reflect not just liquidity but genuine doubt about whether the backing is enforceable.

Risks. Disputed/possibly unenforceable backing, no attestations, no shareholder rights, illiquid private underlyings, US‑person exclusion.

On‑Chain Spreads & Share Value

Why spreads exist at all. A tokenized stock has two prices: the on‑chain trading price (set by DEX/CEX supply and demand 24/7) and the underlying share value (set by the equity market, which is closed nights and weekends). The gap between them is the story.

During US market hours — arbitrageurs (or authorized participants who can mint/redeem against the real share) keep the on‑chain price ≈ underlying. Pegs are tight; on the liquid names, typical swap slippage tolerance is ~0.1–0.5%.

Off‑hours and weekends — the equity market is closed, no fresh NAV anchors the token, and price floats on pure crypto demand. Premiums and discounts open up — most dramatically around events (a hot new listing like SPCX, or a pre‑IPO name reacting to news).

Liquidity is concentrated. Across all four issuers, volume clusters in a handful of marquee tickers (TSLAx, NVDAx, CRCLx, SPCX). The long tail of 100+ listed assets often has thin order books, meaning wide quoted spreads and steep slippage for any meaningful size.

Conclusion

The January 2026 SEC staff statement tightened scrutiny on synthetic equity while opening a supervised path for true entitlement models — a December 2025 DTC no‑action letter preserves UCC Article 8’s indirect‑holding framework. The trajectory favors issuer‑sponsored and redeemable‑custodial models, such as Backpack and Superstate’s native equities, and pressures purely synthetic ones like PreStocks. The PreStocks SPV‑transfer dispute is the clearest live example of the tokenizer‑specific risk the SEC warned about: the token traded fine until the referenced companies said the backing wasn’t valid.

That regulatory line maps directly onto how the four products actually differ. On a chart they all track a stock price, but legally and structurally they are four different instruments — Backpack is closest to owning and redeeming the real share, Ondo is the best‑protected note, xStocks is the most DeFi‑native tracker certificate, and PreStocks is the most speculative synthetic SPV exposure. On‑chain, the decisive variable for spreads is whether a live underlying market exists to arbitrage against, which is exactly why the liquid xStocks names hold a tight peg during market hours while PreStocks can dislocate violently. The venue question is settled; the structure question is not — and that, not the ticker, is what every holder is actually choosing between.