Understanding $RAWR

The Project

Jurassic Finance is a Solana project proposing to acquire authenticated dinosaur fossils, place them inside Cayman SPVs, and sell fractional tokens against each one. The Labs entity, raising now under the ticker $RAWR, would operate the platform. The first fossil vehicle, a Triceratops head targeting roughly $1M, is scheduled for Q3 2026.

$RAWR holders own the operating company. They earn platform-level fees from every SPV that launches, receive 5% of each SPV’s token supply, and govern the treasury through futarchy. They do not own any fossil. They own a claim on the team’s ability to repeatedly originate and run fossil SPVs. SPV token holders ($TRCH1 being the first) own fractional economic rights to the underlying specimen via the Cayman entity. They benefit from the asset appreciating. They do not benefit from the platform succeeding beyond their specific fossil.

The risk profile of $RAWR depends almost entirely on execution. The risk profile of an SPV token depends on the specimen and the market for it.

What the Team Has Done

What exists: A website (jurassic.finance), a Twitter account with under 3,000 followers, an investor deck, a few thesis articles published by the team, a waitlist that the team reports at 3,300 signups, and a Cayman SPV structure that the team says has been scoped with legal counsel. The team has filed for Colosseum Frontier with a May 11 deadline. None of the contracts are deployed yet. No fossil has been acquired. No museum loan agreement has been signed. No SPV has been structured beyond the planning stage.

What the team has done elsewhere: Vukan runs a Solana creative studio called Blockformer that has produced marketing content for MetaDAO Ownership, Streamflow, Jupiter, and Solflare. Sora was previously COO at Blockformer and spent three years in marketing at LandX, a farmland tokenization project on Ethereum. The team’s combined background is content marketing and Solana-native community building. It is not asset acquisition, custody, legal structuring, or auction-house relationships.

What is claimed but unverified: Inbound from “100+ potential advisors, investors, and funds.” Active conversations with auction houses. A merchandise partnership the team has not named. An advisory bench that reportedly includes legal, Sotheby’s, tokenization, and paleontologist references.

This is not unusual for a pre-launch raise. Most projects raising on MetaDAO have a similar profile: a thesis, a deck, a small team, and a set of relationships. The relevant point is that none of the operational pieces that make the fossil tokenization model work have been built or tested yet.

Where the Qualitative Case Holds Up

The category is genuinely empty: Wine, watches, sneakers, cards, classic cars, fine art, and rare books all have at least one major tokenization platform. Fossils have zero. This is verifiable and it is structurally interesting. It either means the team has identified a real gap or it means the gap exists for reasons that make the business hard to build. Both are possible. The case for “real gap” is that fossils were not a serious institutional asset class until the last five years and the infrastructure simply has not caught up. The case for “hard to build” is that fossils are illiquid, opaque, hard to authenticate, and legally complicated in ways that wine and watches are not.

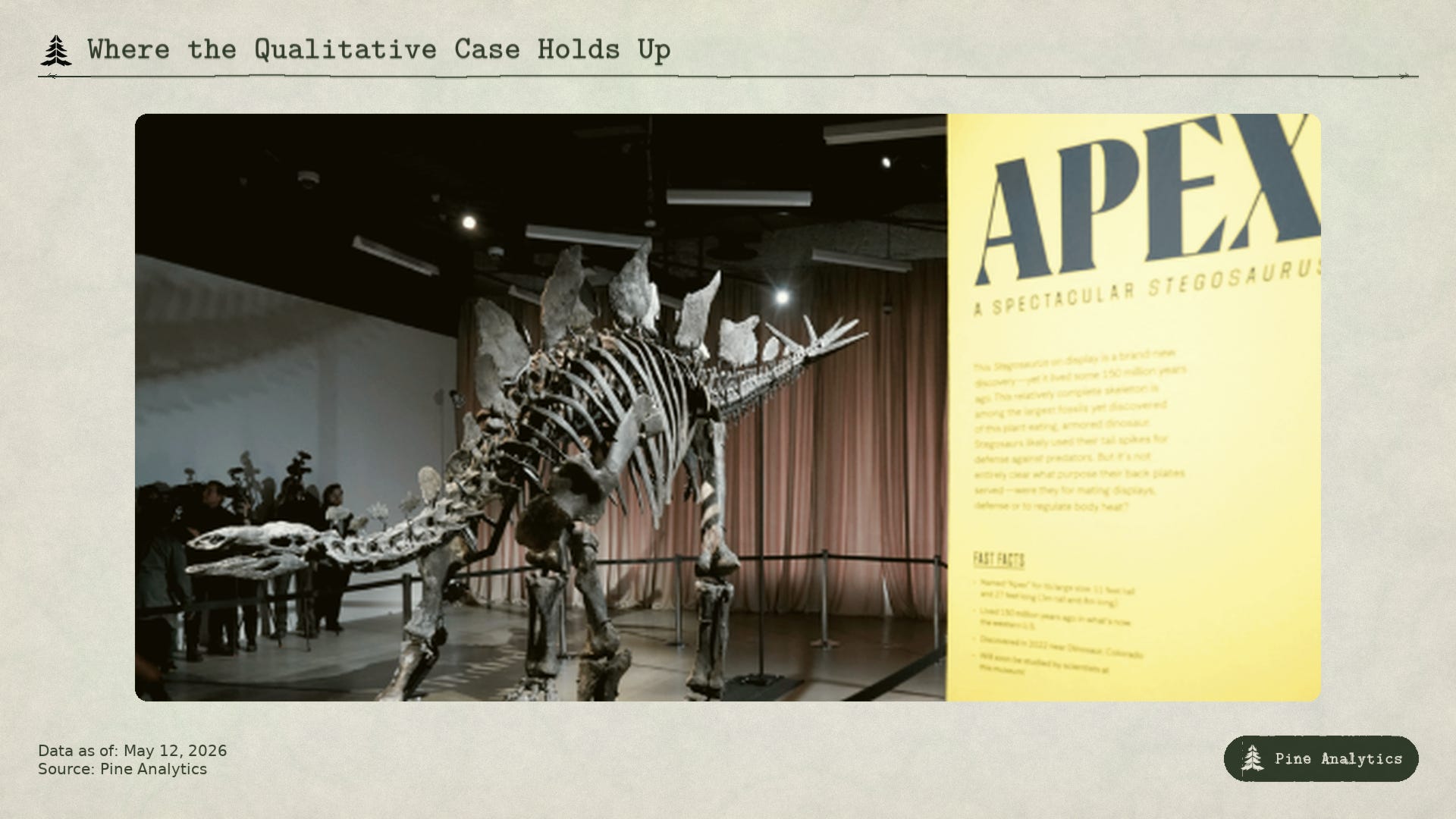

The auction market data is real: Ken Griffin paid $44.6M for the Apex Stegosaurus at Sotheby’s in July 2024, against a pre-sale estimate of $4M to $6M. Stan the T-Rex cleared $31.8M in 2020. These are documented sales. The bid for top-tier specimens has clearly stepped up. What is less clear is whether the demand at the very top of the market translates into demand for the $500K-to-$5M specimens that a tokenization platform would realistically be able to acquire.

The museum loan structure is sound in principle: Major museums do accept long-term loans of high-quality specimens and do typically assume conservation and insurance costs in exchange for display rights. This is how a lot of high-value paleontology specimens are housed today. Whether an accredited natural history museum will accept a loan of a specimen that is being publicly traded as a fractional security is an open question. The QR-code-to-fractional-ownership detail in the team’s pitch is the kind of thing that institutional curators tend to push back on. The structure works in concept. The execution depends on a museum being willing to participate.

The MetaDAO mechanism is genuinely protective: The launch valuation gets capped regardless of demand, the treasury operates under futarchy with a published monthly allowance, and the team’s tokens are locked for an 18-month cliff with price-milestone-gated unlocks after that. The structural protections for $RAWR holders are real, well-documented, and have been tested across the platform’s prior launches.

Where the Qualitative Case Gets Weaker

The five revenue streams look like diversification but on closer reading they all collapse into the same underlying requirement: the platform needs to tokenize a lot of fossils and build a sizable active buyer pool for SPV tokens. The origination fee and the 5% SPV token allocation are effectively the same line, both paid at issuance and both scaling with the cadence and size of SPV launches. The lending market requires a deep pool of SPV tokens on-chain to lend against before it generates substantive revenue, which is downstream of that same issuance cadence.

The FOSSIL buyback program has a different but related problem. The standing bid only gets triggered when on-chain demand for the SPV tokens is weak, which means the program activates exactly when the platform is struggling, not when it is succeeding. Each token the Reserve absorbs is then sitting on the Labs balance sheet until the team can find an off-chain buyer to take the inventory at or above the absorbed cost. If those buyers exist in size, the buyback program is a reasonable liquidity facility. If they do not, the Reserve compounds illiquid inventory while the platform’s headline demand is already weak.

The merchandise line reads as immaterial relative to the rest.

The “no competition” framing is partly an artifact of category immaturity, not an obvious moat: If Jurassic Finance is the first to demonstrate that fossil tokenization works at scale, the team has shown a competitor that the category is fundable. The actual moat is the relationship with auction houses and museums, neither of which the team has demonstrated publicly. A second mover with stronger institutional relationships and worse marketing could plausibly displace the first mover here.

The team comp set is content marketing, not asset operations: This is the single biggest structural concern. Buying, custodying, transporting, insuring, authenticating, and eventually selling a $1M to $5M physical asset is not the same skill set as running a Solana token launch. The team has not done it before and is not partnered with anyone who is publicly known to have done it before. The advisory roster may close this gap but the public-facing roster does not yet.

The Solana retail base for $1M-plus fossil SPVs is speculative: The Labs raise is filled by people willing to buy a $516K-FDV ownership token of a fossil platform. That is a fundamentally different buyer profile from someone willing to commit $5K to $50K to own fractional rights in a single Triceratops head with no clear exit liquidity for years. The team is assuming the first buyer set converts to the second. This is plausible but unproven, and the size of the gap will determine whether the platform’s economics actually compound.

The Oversubscription

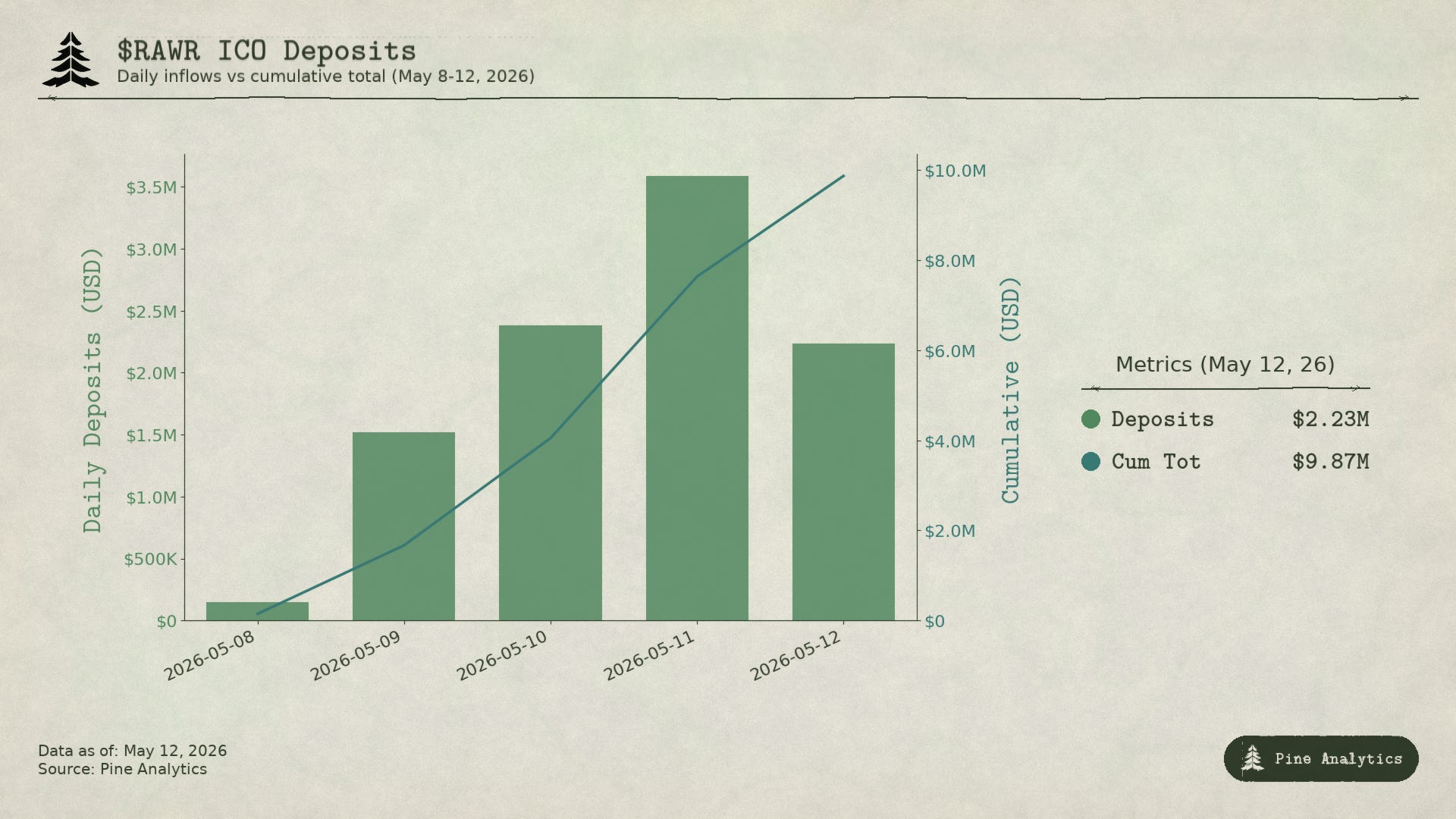

The Labs raise opened on May 8 with a stated $200K target and a seven-day window. With approximately two days remaining as of May 12, the contract has received $9.87M in USDC commitments from 719 unique wallets across 934 individual deposits. That is roughly 49x oversubscribed.

The mechanical explanation of the 49x figure matters as much as the sentiment signal. Once a MetaDAO raise clears its capped amount, every additional dollar of deposit dilutes everyone’s allocation pro-rata, and the dilution gets worse as more capital piles in late. A wallet that committed $10K early in the round may end up receiving allocation as if it had committed a few hundred. Anyone who actually wants size on the launch comes out under-allocated relative to their target, and the natural response is to deposit more into the raise, which is what produces the feedback loop visible in most heavily oversubscribed MetaDAO launches.

What the oversubscription does tell you cleanly is that informed capital views the launch as positive EV. People committing six-figure deposits to a $200K-target raise know exactly how the mechanism works and what it does to their allocation. They are not bidding because they expect to receive their full check at launch. They are bidding because they expect the post-launch market to clear meaningfully higher than the launch price, and the small allocation they do receive is worth the cost of capital and refund risk.

After the Launch: What to Watch

The first SPV launch is the entire test. $TRCH1 is scheduled for Q3 2026. The team’s entire value proposition compresses into whether they can clear a clean first acquisition and launch. Every revenue line in the model assumes this works. The case for for $RAWR rests on the assumption that it does. If $TRCH1 stumbles, $RAWR does not have a fallback thesis.

Specific things worth tracking once $RAWR is trading and $TRCH1 is in progress:

Specimen disclosure. The team has not publicly identified which Triceratops head they intend to acquire. Provenance documentation, bone count, authentication paperwork, and the third-party paleontological assessment are all things that should be public well before the SPV opens. Detailed and verifiable disclosure here would be a strong signal. Vague or late disclosure would be a meaningful flag.

Buyer breadth on $TRCH1. A $1M SPV filled by 500 distinct wallets is a different signal than the same dollar amount filled by 20 wallets, most of whom are also $RAWR whales. The team needs to demonstrate that the SPV layer attracts buyers who specifically want fossil exposure, not just buyers rotating into the next thing the Labs entity launches. The breadth of the $TRCH1 buyer base is probably the cleanest measurable indicator of whether the team is genuinely creating a new asset category.

Museum loan terms. The unit economics of the entire model assume custody costs are transferred to an accredited institution. The first signed loan agreement converts that assumption into a fact. The identity of the museum and the financial terms (who covers insurance, who covers conservation, who covers transit, what the display commitment looks like) will tell holders whether the operational thesis is workable or whether the team is going to need to absorb costs the model does not account for.

$TRCH1 secondary trading. The FOSSIL buyback program and the BONE lending market are designed to provide synthetic liquidity until real secondary volume develops. The question is how quickly real two-way price discovery emerges. Healthy organic volume within the first 90 days would validate the model. A market that requires the Labs Strategic Reserve to function as the sole bid would compress the treasury faster than the model assumes and would call the medium-term economics into question.

Cadence to SPV number two. The published target is 5 to 10 SPVs over 24 months. The second launch is when holders find out whether the platform is a repeatable originator or a one-off. SPV number two arriving quickly after $TRCH1 on improved terms would suggest the flywheel works. A nine-to-twelve-month gap would suggest the model is functional but slower than the bull case requires.

What You’re Underwriting

The framing in the launch materials has run ahead of the operating reality, and the qualitative case for the project rests almost entirely on things the team has not done yet. No fossil acquired, no museum signed, no SPV launched, no contracts deployed. The team’s background is content marketing and Solana community building, not alternative asset operations. The five revenue streams compress into a single bet on issuance cadence and on-chain buyer depth, with the FOSSIL program structurally active in exactly the conditions where it would hurt the balance sheet most.

What works is also real. The category is empty, the auction data supports the demand thesis at the top of the market, the museum loan model is sound in principle, and the MetaDAO mechanism caps the launch valuation while futarchy governs the treasury. The $516K FDV is consistent with a project that has identified a thesis and assembled a team to attempt it, rather than one that has demonstrated it can be executed.

The 49x oversubscription is doing the work people think it is doing, just for slightly different reasons than the narrative suggests. The structural feature of MetaDAO raises is that any wallet that wants real exposure has to over-deposit to defend against pro-rata dilution, which means the headline figure compounds on itself once a raise becomes visibly oversubscribed. What is signal in that number is that informed capital is willing to lock up six-figure deposits knowing most of it refunds, because they expect the post-launch market to clear meaningfully above the launch price. That is a reasonable read of the mechanism, not a guarantee of the business.

The right way to size $RAWR is as a small position priced for option value. The launch valuation is low enough that the team being right about the category and competent enough to clear the first SPV produces a real outcome. The launch valuation is low enough that being wrong about the team produces a livable outcome too. Where the position gets harder to defend is at any valuation that requires the issuance flywheel to have already turned. Above $3M to $5M FDV, the price is no longer pricing the option, it is pricing the outcome, and the outcome has not been demonstrated.

The first SPV will resolve most of the open questions. Until then, $RAWR is a wager on a thesis and on two people executing in a skill set they have not publicly demonstrated. The thesis has merit. The mechanism protects the entry. The team is the variable.