$UP Has Nowhere to Go But Down

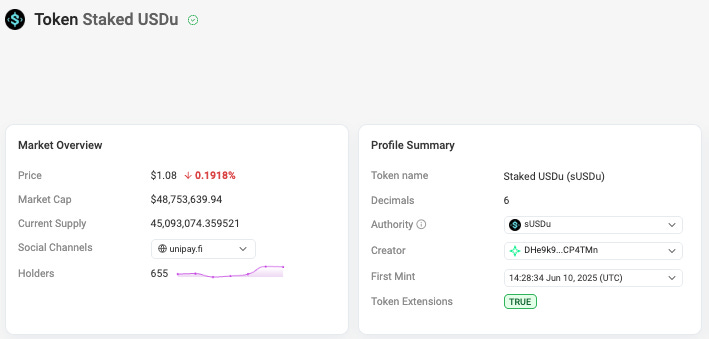

Unitas Labs is launching its $UP governance token via Binance Wallet TGE on March 13. The protocol runs a yield-bearing stablecoin stack on Solana — USDu as the base dollar token and sUSDu as the staking receipt that accrues yield. The yield engine is a delta-neutral JLP strategy: long JLP on-chain, short the underlying basket (SOL, ETH, BTC) on centralized exchanges via off-exchange settlement. Revenue flows 80% to sUSDu holders, 10% to an insurance fund, and 10% to treasury.

sUSDu currently advertises 12.92% APY. On the surface, that’s competitive. But the math underneath tells a different story — and the $UP token launching into this setup has problems that are hard to look past.

The Yield Isn’t What It Looks Like

There is roughly $80M in USDu supply. Of that, approximately $48M is staked into sUSDu — a 60/40 split that flatters the headline yield. The protocol earns yield on the entire collateral base, but only distributes to stakers. So the 12.92% APY that sUSDu holders see is the product of a much lower total return — approximately 7.75% on assets deployed — concentrated into a smaller pool of recipients.

The reason ~$32M in USDu is sitting unstaked is straightforward: the points campaign awards 20 points per USDu held versus only 5 points per staked USDu. Airdrop farmers are rationally choosing to hold USDu rather than stake it because the points-to-capital ratio is 4x better. That unstaked capital earns nothing for its holders while being exposed to all the same smart contract, custody, and strategy risk — but it serves as a subsidy that inflates sUSDu’s advertised APY.

This ratio will revert quickly after the TGE. Once points stop accruing, there’s no incentive to hold USDu without staking it. The unstaked USDu either gets staked — compressing the yield toward the actual 7.75% base return — or it leaves the protocol entirely as farmers redeem out. Either outcome is bad for the headline number: more stakers means lower APY, fewer deposits means lower absolute revenue. And 7.75% from a delta-neutral JLP carry is not a differentiated number.

The TVL Is Airdrop-Driven

Unitas was sitting around $22M in TVL through early January. When the airdrop campaign was announced mid-January, TVL surged past $100M. The conclusion is straightforward: 75%+ of the protocol’s current TVL exists because of airdrop farming and will leave shortly after the token launches and the points program concludes. This isn’t speculation — it’s the pattern every single points-driven protocol has followed. The question isn’t whether TVL drops. It’s how far.

A return to the ~$22M pre-airdrop baseline is the reasonable floor case. The protocol may retain some sticky capital above that, but the magnitude of the farming-driven inflow makes the current TVL an unreliable signal of organic demand.

No Moat in a Crowded Strategy

Delta-neutral JLP vaults are one of the most replicated strategies on Solana. Of the top 10 Drift vaults by TVL, eight run some variant of delta-neutral JLP. Gauntlet, Neutral Trade, Vectis, Kvants, and several others all execute the same fundamental trade: long JLP, short perps, harvest carry..

Unitas wraps this strategy in a stablecoin interface. That’s a product decision, not a moat. There’s nothing proprietary about the underlying execution. The collateral is JLP. The hedges are perp shorts on centralized exchanges. Anyone with a multisig and a Ceffu account can do this.

When a strategy is this commoditized, margins get squeezed. Protocol-level fees at Unitas are currently zero for minting, staking, and redeeming — meaning the protocol captures revenue only from the spread between gross strategy returns and what it distributes. That 20% take (10% insurance + 10% treasury) has to cover team expenses, infrastructure, and eventually generate some return for token holders. In a competitive market where multiple providers are offering the same trade, the pressure to pass more yield through to depositors only increases.

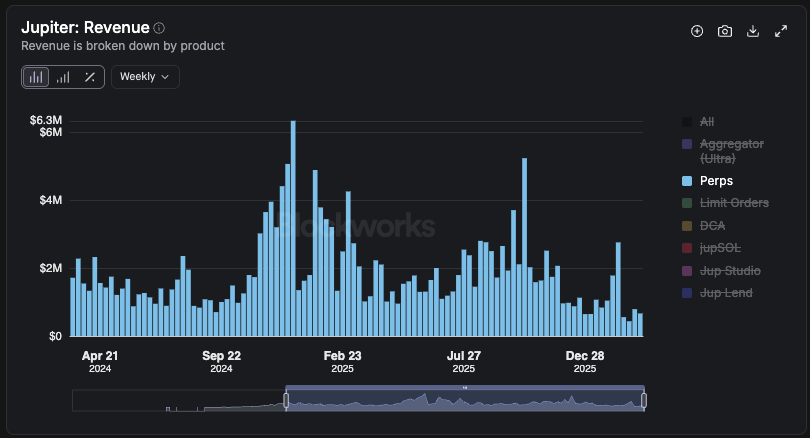

Jupiter Perps Are in Secular Decline

The entire delta-neutral JLP thesis depends on Jupiter Perps generating trading volume. JLP revenue comes from open/close fees, price impact, borrow fees, and trader losses — all functions of active trading.

Jupiter Perps volume has been in a sustained downtrend. The weekly reports tell the story:

Early December 2025: ~$440M daily average

Late December 2025: ~$189M daily average

Late January 2026: ~$270M daily average

Mid-February 2026: ~$173M daily average

Early March 2026: ~$277M daily average (bounce on SOL price move)

The trend is down and to the right, with periodic bounces that correlate to price volatility rather than organic growth in trading activity. Every delta-neutral JLP strategy scales with this number. As perps volume declines, the fee pool that JLP captures shrinks, and the carry that strategies like Unitas harvest compresses.

This isn’t a Unitas-specific problem. It affects every delta-neutral JLP vault on Solana. But it’s especially relevant when valuing a token whose entire revenue model depends on this single fee stream.

Attempting a Valuation

Let’s try to be generous. Assume the protocol stabilizes at its pre-airdrop TVL of ~$22M after the farming crowd exits. Assume a 7.75% gross return on deployed assets. That’s roughly $1.7M in annual gross revenue. The protocol retains 20% — $340K. From that, subtract team costs, infrastructure, audits, insurance fund contributions, and Ceffu/MPC custody overhead. The actual free cash flow available to token holders is substantially less than $340K.

Even at $340K in annual protocol revenue and a generous 10x revenue multiple (aggressive for a protocol with no moat, declining TAM, and commodity strategy), the implied FDV is $3.4M. With an estimated 1 billion token supply, that’s $0.0034 per $UP.

And $3.4M is the generous number. A 10x revenue multiple assumes meaningful growth potential and defensibility — neither of which exist here. The protocol runs a commodity strategy that eight other Drift vaults already replicate. The roadmap — cross-chain expansion, permissionless collateral adapters, a Unipay Card — doesn’t contain anything that would meaningfully increase margins or drive sticky TVL growth.

The Binance Wallet TGE is pricing $UP at $0.005 — a $5M FDV. That means even under our most favorable assumptions — full retention of pre-airdrop TVL, no margin compression from competitors, team costs magically at zero — the token is still launching at roughly 50% above what the cashflows could support. In reality, with team expenses, continued perps volume decline, and competitive pressure squeezing the take rate, the gap is almost certainly wider.

When the most optimistic version of the math still says overvalued, that’s a no-go zone.